A Trump Tweet Is a Good Excuse to Take Profits

A Trump Tweet Is a Good Excuse to Take Profits

(Bloomberg) -- Neither the Brexit drama nor patchy macro data has been enough to derail Europe’s equity market rally in 2019. Until a few tweets from President Donald Trump, which revived concerns on trade and gave investors an excuse to take some money off the table.

Sure, the rally looked increasingly stretched anyway, and some cautiousness was already in the air as Friday’s strong U.S. non-farm payroll print met a muted price action in Europe, and some market participants mumbling about labor force participation to explain the absence of euphoria. When people start looking for excuses to sell, it’s usually a good indicator of an exhausted rally.

On a positive note: the market’s overbought conditions, measured by the RSI on the charts, are gone. Sometimes, this is enough for money to return quickly. In this year’s rally, a lot of investors have been sitting on the sidelines, waiting for pull-backs to buy, and we saw some of that yesterday with both the Euro Stoxx 50 and the S&P 500 bouncing off lows.

Investors should buy the dip as Trump’s threat to raise tariffs on China imports is unlikely to trigger a decline of more than 5 percent, according to Tom Lee, co-founder of Fundstrat Global Advisors LLC.

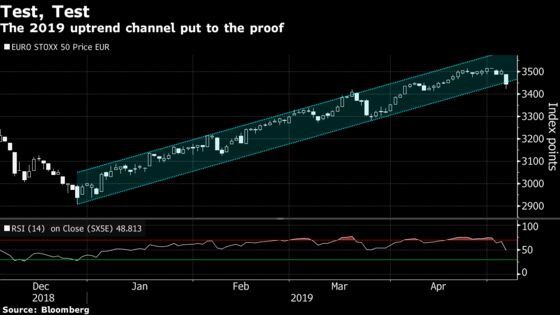

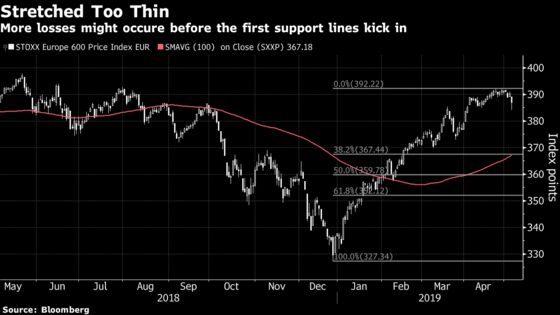

Technically speaking however, the retreat puts the market’s 2019 uptrend channels to the test. Given the fact that neither the Euro Stoxx 50 nor the Stoxx 600 have seen a meaningful correction so far this year, the support levels are rather low. The Stoxx 600’s 100-day moving average allows for another 5 percent drop, and typical Fibonacci retracement levels suggest similar levels as a first line of defense.

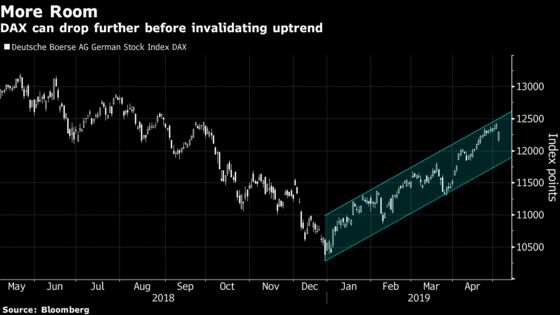

There are exceptions, mainly found with this year’s underperformers. Looking at the DAX, among the most exposed markets to trade jitters, the index seemed relatively resilient on Monday.

“The reaction to the setback is crucial and if the DAX continues to show stability, this would be extremely bullish,” says Donner & Reuschel analyst Orlando Rodrigues. The area around 12,230 could serve as support. The benchmark is also operating in a broader trend channel giving it more leeway to absorb losses before reversing the trend.

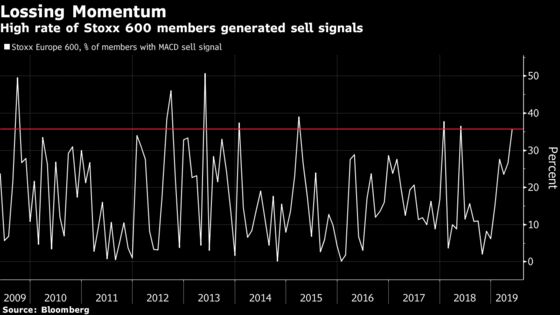

Overall, with earnings season in full swing and the European elections on the horizon, potentially adding more political uncertainty, the margin for error is slim. The ugly combination of weak data, exhausted momentum and political uncertainty could put the four-month long stock market rally to the test.

In the meantime, European shares are set to fall again, with Euro Stoxx 50 futures trading down 0.5 percent ahead of the open and the FTSE 100 futures down 0.5 percent.

- Watch U.K. stocks for reaction to Trump’s tweets after the market was closed Monday for a holiday. Watch miners in particular, as most of them are U.K.-listed, after European stocks tumbled. Wall Street analysts questioned whether the tariffs are a tactic. The pattern of prior tweets and market moves suggest buying the dip.

- Watch for impact of European economic forecasts and German factory orders, as economic activity in the euro area at least showed some signs of stabilizing.

COMMENT:

- “The threat of a ratcheting of U.S. tariffs on China this coming Friday and a much more entrenched trade dispute has not been discounted by equity markets,” Jefferies strategists including Sean Darby write in a note. “The trading action over the past 24 hours suggests that investors believe President Trump’s threat is a negotiating ploy to prevent further Chinese procrastination. A good outcome seems fully baked into the U.S. companies with high revenue exposure to China.”

COMPANY NEWS AND M&A:

- AB InBev Confirms Plan for Hong Kong IPO Asia Pacific Unit (1)

- BMW Sets EU1.4b Antitrust Provision, 1Q EBIT Falls 78% Y/y (1)

- Henkel 1Q Adj. Ebit Falls 5.6%; Forecast Confirmed

- EssilorLuxottica First Quarter Revenue Meets Estimates

- Adecco First Quarter Revenue Meets Estimates

- Infineon 2Q Adj. EPS Beats Estimates; FY Guidance Maintained (1)

- UniCredit Considers Sale of 10%-15% Stake in Finecobank: Sole

- Cellnex to Pay About EU2.7 Billion in Cash for 3 Tower Deals

- Alstom FY Adj. Ebit EU570m, Est. EU578.7m

- Siemens Gamesa Second Quarter Sales Meet Estimates

- Airline Built on Airbus Jets Prepares Another ‘Large’ Order

- Solvay First Quarter Adjusted Ebitda 1.2% Above Estimates

- Arkema 1Q Rev., Ebitda Meet Estimates; Keeps Forecast

- DSM Raises FY Adj. Ebitda Guidance After 1Q Adj. Ebitda Beat (1)

- Orkla First Quarter Adjusted Ebit Beats Highest Estimate

- Iliad First Quarter Revenue EU1.29 Bln

- Pandora First Quarter Revenue 1.2% Below Estimates

- HelloFresh First Quarter Revenue 4.8% Above Estimates

- PostNL 1Q Underlying Cash Operating Income Matches Estimates (2)

- Vonovia Sees FY FFO About 5% Higher From Prior Year

- Evonik Raises FY Adj. Ebitda, Sales Outlook

- Oerlikon 1Q Sales CHF624m, Misses Co.-Comp. Estimate of CHF630m

- Roche’s Firefish Trial Achieves Key Motor Milestones

NOTES FROM THE SELL SIDE:

- Banco Sabadell is raised in a Morgan Stanley note to overweight from equal-weight on improved visibility, with price target boosted to EU1.35 from EU1.10. Re-rating of shares seen driven by more credible capital road-map, with funding markets and TSB unit leading to better earnings visibility.

- Peel Hunt says the market is overly bearish on Acacia Mining and sees as much as 50% upside for the stock, upgrading shares to buy from add. Broker cuts price target to 215p a share from 230p based on a weak 1Q, and says shares could re-value toward at least 186p even without a resolution with government of Tanzania.

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 392.7 (July 2018 high); 403.7 (January 2018 high)

- Support at 385.7 (76.4% Fibo); 382.1 (50-DMA)

- RSI: 50.3

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,516 (76.4% Fibo); 3,596 (May high)

- Support at 3,403 (61.8% Fibo); 3,391 (50-DMA)

- RSI: 53.5

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- Acacia Mining upgraded to buy at Peel Hunt

- Air France-KLM upgraded to neutral at MainFirst; PT 8.50 Euros

- Hochtief upgraded to buy at Kepler Cheuvreux; PT 142 Euros

- Koenig & Bauer Upgraded to Buy at Bankhaus Metzler; PT 50 Euros

- Mapfre upgraded to overweight at JPMorgan; PT 3.30 Euros

- Novo Nordisk upgraded to neutral at Oddo BHF; PT 333 Kroner

- Persimmon upgraded to buy at Citi

- Piovan upgraded to buy at Kepler Cheuvreux; PT 7.80 Euros

- SBM Offshore upgraded to overweight at Barclays; PT 25 Euros

- Sabadell upgraded to overweight at Morgan Stanley

- SocGen upgraded to neutral at Mediobanca SpA; PT 31.20 Euros

- Tele2 upgraded to buy at HSBC; PT 142 Kronor

- Tubacex upgraded to buy at Ahorro Corporacion; PT 3.80 Euros

DOWNGRADES:

- Centrica downgraded to reduce at HSBC; PT 90 Pence

- Deutsche Post downgraded to hold at Berenberg; PT 34 Euros

- Essentra Downgraded to Hold at Stifel; PT 4.20 Pounds

- GARO AB downgraded to hold at Carnegie; PT 255 Kronor

- Gecina downgraded to equal-weight at Barclays; PT 145 Euros

- Hammerson downgraded to reduce at AlphaValue

- Nordea downgraded to reduce at AlphaValue

- Roche downgraded to reduce at Oddo BHF; PT 263 Francs

- Scout24 downgraded to hold at Kepler Cheuvreux; PT 49 Euros

- SocGen downgraded to hold at DZ Bank; Price Target 30 Euros

- UCB downgraded to reduce at Oddo BHF; PT 68 Euros

- Umicore downgraded to hold at Berenberg

INITIATIONS:

- None reported.

MARKETS:

- MSCI Asia Pacific down 1.2%, Nikkei 225 down 1.6%

- S&P 500 down 0.4%, Dow down 0.3%, Nasdaq down 0.5%

- Euro up 0.13% at $1.1213

- Dollar Index down 0.09% at 97.42

- Yen up 0.12% at 110.63

- Brent down 0.1% at $71.2/bbl, WTI up 0.2% to $62.4/bbl

- LME 3m Copper up 0.5% at $6265/MT

- Gold spot up 0.1% at $1282.1/oz

- US 10Yr yield up 1bp at 2.48%

MAIN MACRO DATA (all times CET):

- 8:45am: (FR) March Trade Balance, est. -4.5b, prior -4b

- 8:45am: (FR) March Current Account Balance, prior -800m

- 9:30am: (UK) April Halifax House Prices MoM, est. 0.1%, prior -1.6%

- 9:30am: (UK) April Halifax House Price 3Mths/Year, est. 4.5%, prior 2.6%

- 9:30am: (GE) April Markit Germany Construction PMI, prior 55.6

- 10am: (UK) April New Car Registrations YoY, prior -3.4%

- 11am: (EC) EU Commission Economic Forecasts

- 11am: (IT) Istat Releases the Monthly Economic Note

--With assistance from Michael Msika.

To contact the reporter on this story: Jan-Patrick Barnert in Frankfurt at jbarnert3@bloomberg.net

To contact the editor responsible for this story: Blaise Robinson at brobinson58@bloomberg.net

©2019 Bloomberg L.P.