Facebook’s Shrinking Margins Top List of Woes Weighing on Stock

Facebook’s shrinking margins are giving investors the most pause.

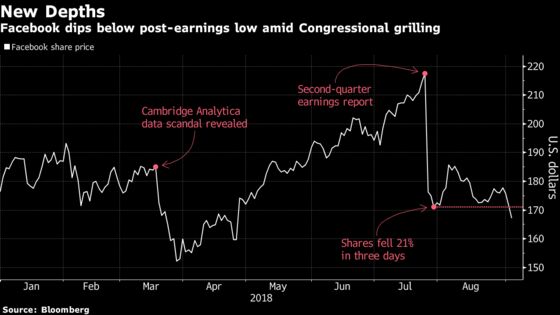

(Bloomberg) -- Facebook Inc. has contended with data privacy scandals, U.S. lawmaker scrutiny and slowing user growth in 2018. Yet the social network’s shrinking margins are giving investors the most pause.

As the internet giant’s shares continue to languish in the aftermath of its $121 billion one-day rout in July, Facebook will need to show that it can jump-start earnings growth to restore faith with investors who have been reluctant to buy, analysts and shareholders say.

“Facebook hasn’t built confidence in anybody,” Ross Gerber, chief executive officer of Gerber Kawasaki Wealth & Investment Management, said by phone. “They’ve done a very poor job at dealing with problems.”

Shares of the Menlo Park, California-based company have continued to slide after the historic selloff, which was triggered by forecasts for narrower operating margins and slowing revenue growth. Criticism of its content policies from U.S. President Donald Trump and the prospect of government regulation haven’t helped, nor have indications that some users are reducing time spent on Facebook. On Wednesday, U.S. lawmakers on the Senate Intelligence Committee discussed the regulation of social-media companies during testimony from Facebook Chief Operating Officer Sheryl Sandberg. The stock fell 3.9 percent as of 1:04 p.m. in New York on Thursday, extending its losing streak to a fourth-consecutive day.

While shares of Faang-group counterparts Apple Inc. and Amazon.com Inc. have been setting records, Facebook is the only member that has lost ground in 2018. Netflix Inc. is up 78 percent, while Google parent Alphabet Inc. has gained 14 percent.

For Wedbush Securities analyst Michael Pachter, the pressure on Facebook’s share price might be eased if the company cut spending.

Facebook’s expenditures on initiatives like product development, infrastructure and security -- including plans to hire thousands of people to work on investigating issues with fake news and election interference -- will increase 50 percent to 60 percent this year and will outpace revenue growth in 2019, Chief Financial Officer David Wehner said on the July 25 earnings call. Capital expenditures, which includes spending on physical assets like data centers and equipment, are forecast to jump to $15 billion in 2018, up from $6.7 billion last year. Wehner said operating margins will "trend towards" the mid-30 percent range over the next several years. That compares with 44 percent in the second quarter.

"Facebook is essentially saying, whatever you think our revenues are going to do, our operating expenses are going to grow faster," said Pachter, who has had an outperform rating on the stock since the initial public offering in 2012. "If margins do in fact compress, they should rethink what they’re spending money on because investors don’t like it. If in fact margins expand, the stock is going to zoom right back up to $200 and keep going."

The spending is necessary, in part, because the company’s main moneymaker -- the ads in the Facebook news feed -- can’t grow much further. The company’s news feed has been able to steadily fuel growth, either with more users or more ads. Now, the company connects a majority of the world’s internet population, so the future drivers of growth will have to come from more experimental revenue sources, like messaging and virtual reality.

Declining margins were at the core of a rare downgrade on Tuesday by MoffettNathanson analyst Michael Nathanson, who had maintained a bullish rating on the stock since 2015.

"Revenue growth deceleration coupled with the company’s long-term margin guidance does not provide a meaningful near-term path for outperformance," the analyst wrote in a research note. Slowing growth combined with continued regulatory scrutiny is a "toxic brew," Nathanson wrote.

For Facebook to regain its mojo, the company will have to beat its forecasts and assuage concerns about regulatory and antitrust risks, Nathanson said.

Facebook has a history of giving conservative forecasts and exceeding expectations, said Jason Benowitz, senior portfolio manager at Roosevelt Investment Group Inc. In addition to spending less than projected, Facebook needs to demonstrate that it can generate more revenue from its WhatsApp and Instagram businesses.

"We think that the bear case won’t fully play out the way management presented it," said Benowitz, whose firm owns Facebook shares. "It’s hard to grow your expenses 50 percent."

Gerber remains skeptical. While his firm still owns Facebook shares, he’s reduced his exposure to the stock and plowed the proceeds into Alphabet.

Facebook has been a "hugely profitable investment for us," Gerber said. "But I think that government regulation is coming and their business is never going to be the same."

Still, the majority of Wall Street remains bullish. The stock has 40 buy ratings, 6 holds and 2 sells, according to data compiled by Bloomberg. The average price target is $206, representing an implied gain of more than 20 percent from current levels.

To contact the reporters on this story: Jeran Wittenstein in San Francisco at jwittenstei1@bloomberg.net;Sarah Frier in San Francisco at sfrier1@bloomberg.net

To contact the editors responsible for this story: Jillian Ward at jward56@bloomberg.net, ;Catherine Larkin at clarkin4@bloomberg.net, Brad Olesen

©2018 Bloomberg L.P.