Tesla Going Private Would Demolish Doubters in Default Swaps

Tesla Going Private Would Demolish Doubters in Default Swaps

(Bloomberg Opinion) -- Elon Musk fired a bazooka in his war against Tesla Inc.’s equity market short-sellers when he announced he’s considering taking the company private. His plan would also most likely wipe out investors who bet the money-losing automaker would eventually default on its bonds.

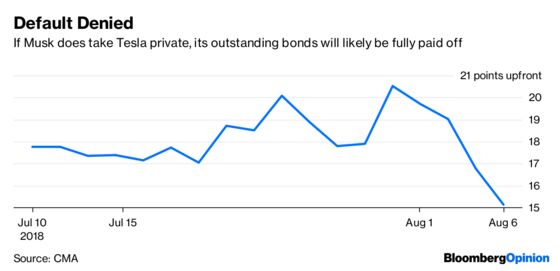

The cost to insure against Tesla failing to make good on its debt fell to an all-time low, with five-year credit-default swaps implying just a 35 percent chance of a missed payment in the next half-decade, down from 43 percent earlier this month. Even that seems far too high if you believe Musk will follow through on his privatization plans (and that’s a big if). That’s because such a move would most likely trigger the bonds’ change of control covenant, which would pay holders 101 cents on the dollar and take out the unsecured debt.

In other words, Tesla can’t default on debt that’s already paid off, just as investors can’t short shares of a company that goes private. Musk’s plan would crush the “large numbers of people who have the incentive to attack the company,” as he put it in a blog post.

It’s a stunning turn of events. JPMorgan Chase & Co. had reportedly led an effort to make a market in the derivatives, and Goldman Sachs Group Inc. supposedly quoted Tesla CDS prices, too. It could have been one of the few credits to have experienced a decent amount of CDS trading since the crisis.

Instead, the bonds rallied, with 5.3 percent coupon notes due in 2025 trading at 92.4 cents on the dollar. That does reflect some skepticism that the deal will truly come together. Bloomberg Intelligence credit analyst Joel Levington’s reaction was that “funding such a deal that could manage a large debt load as Tesla struggles to generate cash will be a challenge.”

Ivan Feinseth, chief investment officer at Tigress Financial, gave a rough estimate of how much debt would be needed to accomplish Musk’s vision.

“To finance around $58 billion even in rates in low teens — let’s say 12.5 percent — would be $7.1 billion in interest every year. Even though he projects to be cash flow positive by the end of this year, that would not be enough cash to pay the debt.”

The irony, of course, is that’s the exact scenario that CDS buyers were contemplating over the past weeks. Instead, they’re on the brink of a total loss.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2018 Bloomberg L.P.