Unlike Peak Oil, Peaker Gas Has a Future

Unlike Peak Oil, Peaker Gas Has a Future

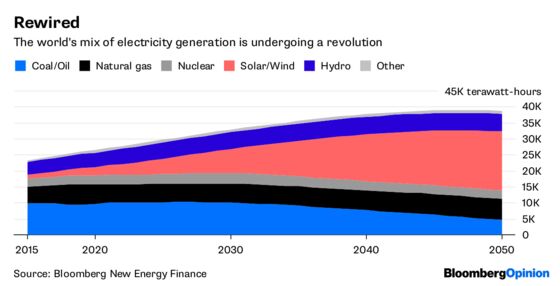

(Bloomberg Opinion) -- Bloomberg New Energy Finance has just released its annual tome of forecasts. The short story is that wind and solar power are getting cheaper and we will all be using more of them — a lot more, and relatively soon:

Not the most encouraging forecast for coal, obviously. Natural gas, though, is a bit more nuanced.

While gas-fired electricity drops from 25 percent of the market to 17 percent, its absolute output isn’t cut in half as coal’s is. On the other hand, it doesn’t grow much either. That undermines the thesis of gas being a “transition” fuel, generating lower carbon emissions than coal and bridging power’s dirty past and cleaner future.

Still, even under BNEF’s projection of a far greener energy sector, gas is expected to have a meaningful role, particularly as flexible capacity. The intermittency of solar and wind power requires more sophisticated management of demand for power, as well as storage and back-up options. Storage generally means batteries, and BNEF certainly foresees growth there, with capacity forecast to rise by a factor of more than 160 times by 2050.

But the limitations of lithium-ion batteries — particularly in terms of meeting peak demand for long periods or providing storage over long periods of time — means BNEF foresees gas-fired plants continuing to provide back-up. What changes, however, is the type of plant required.

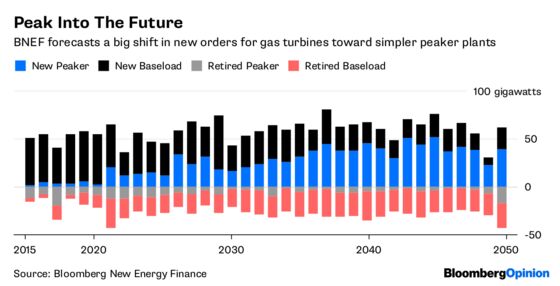

Rather than the more efficient (and expensive) combined-cycle gas turbines that dominate the market now, simpler (and cheaper) “peaker” plants — which turn on only to meet high demand — will be more suited to competing with renewables and storage for those relatively infrequent periods where they can provide the last kilowatt-hour required. Hence, the mix of new gas plants being built shifts significantly:

One striking aspect of that projection is the sheer size of the market, with orders for new turbines averaging almost 60 gigawatts a year. That contrasts sharply with the gloomier noises coming from manufacturers such as Siemens AG and General Electric Co. (see my colleague Brooke Sutherland’s column on their troubled power businesses here). GE is planning for a market of less than 30 gigawatts of new heavy-duty gas turbine orders in 2019 and 2020. BNEF’s projections imply that may be too pessimistic.

Concurring with this, a new report from Hugh Wynne and Eric Selmon of Sector & Sovereign Research LLC, also published this week, projects turbine orders to rise from 31 gigawatts in 2020 to 49 in 2025 and 70 in 2030. Even under its more-bearish scenario — where batteries are deployed much more quickly — annual orders rise back toward 50 gigawatts by the end of the 2020s, in part simply to replace retiring plants (on that note, it’s worth pointing out BNEF’s projections imply net additions to capacity averaging just 31 gigawatts a year out to 2050).

If that offers a hopeful note for turbine-makers, it comes with caveats.

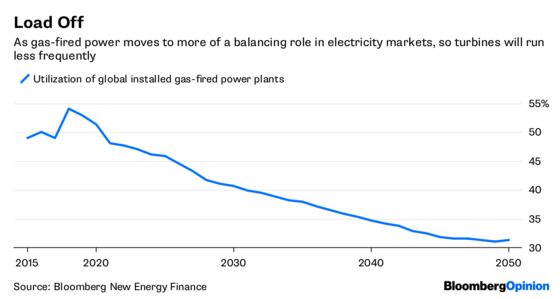

The shift toward peakers rather than baseload gas plants means even if orders are higher than expected, that will be partly because they are cheaper. There’s no other way to compete in a market becoming more defined by renewable sources, where deflation is structural. Plus, as peakers, they will be used less often:

Cheaper plants requiring less maintenance mean the revenue opportunity for turbine makers probably won’t be as big as those higher order numbers imply.

The other issue to consider is this: Who will finance and build those gas plants? In the past, merchant generators played a big role in the gas-plant boom in the U.S. But that model has come under increasing pressure as power demand has flattened and things like renewable energy and demand management have muscled in — all of which will intensify from here.

Future gas-peaker plants may instead have to be built by utilities (funded by ratepayers) or require some other incentive mechanism similar to the capacity auctions currently run in some U.S. regional power markets. In this country, at least, the energy transition and the political maneuvering to undercut it make getting to a sensible and, from a developer’s perspective, reliable planning environment doesn’t look like a sure thing.

Above all, the biggest wildcard is that transition itself. If storage technologies, in particular, advance much more rapidly, then natural gas’ role begins to look more doubtful. Even the concept of peaks in power demand is shifting as a result of renewable energy’s penetration and the likely impact of more electric vehicles getting on the road (and into sockets). The overriding message from BNEF’s report is that the world is changing profoundly; gas will have to fight for its place in it.

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

©2018 Bloomberg L.P.