Ontario Fair Hydro Bonds Offer Fat Yield, Political Baggage

Even Investors Are Holding Their Nose Over Ontario's Hydro Bonds

(Bloomberg) -- Sometimes even a juicy yield offered by a government-backed issuer at a time of near-record low interest rates isn’t enough to entice some bond fund managers.

That’s the case of Fair Hydro Trust, a complicated piece of bond-market engineering designed to finance cuts to Ontario’s soaring hydro bills by adding as much as C$20 billion ($15 billion) in long-term debt. The program, unprecedented in Canada, has been lambasted by the province’s accounting watchdog and spurned by asset managers like Jeff Herold of J. Zechner Associates, who’s passed on buying the securities.

“The reduction in electricity charges is just a craven attempt to disguise the government’s bumbling mismanagement of the energy sector,” said Herold, who oversees C$2 billion as chief executive officer of the Toronto-based fund manager. “Fair Hydro Trust is bad policy and buying it would encourage governments to do similar deals in the future.”

The Fair Hydro Plan has become an unlikely flashpoint in a June 7 election in Canada’s most populous province with critics labeling it a blatant attempt by Premier Kathleen Wynne’s government to curry votes that will leave electricity users footing the bill. The government argues it’s a fair way of sharing the cost of funding green power with future generations who will benefit from cleaner air.

Adjustment Charge

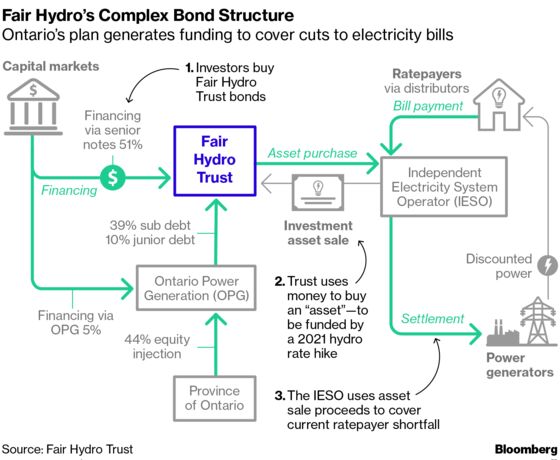

Cutting hydro bills was the easy part. Coming up with a framework that would cover the revenue shortfall for power-distribution companies without breaking the Liberal government’s promise to climb out of deficit was a bit more complex. Enter Fair Hydro.

Under the plan, a new Clean Energy Adjustment charge will be added to electricity bills in May 2021. Fair Hydro Trust, an entity managed by provincially owned Ontario Power Generation, will buy rights to these charges from Ontario’s Independent Electricity System Operator, financed by debt that uses the charges as collateral.

The trust has made two forays into the bond market so far, raising C$900 million in February and April offerings lead by CIBC World Markets, Goldman Sachs and RBC Capital Markets. In its inaugural transaction it sold C$500 million of 15-year bonds with a 3.357 percent coupon. They priced 92 basis points above federal bonds, or around 21 basis points over Ontario’s bonds. The deal attracted 36 buyers, according to people familiar with the matter, fewer than a typical investment-grade corporate bond that gets distributed among institutional investors in the same way.

Balanced Budget

Both of Fair Hydro’s bonds are doing well in the secondary market, trading above par and outperforming Ontario bonds. Ontario’s bonds have dropped 0.1 percent since the first Fair Hydro bond was sold in February, while the trust’s bonds generated a 1.7 percent return, according to data compiled by Bloomberg. The program is expected to peak at almost C$20 billion outstanding by 2029 and mature in 2047.

The plan allowed Finance Minister Charles Sousa to announce that the government had balanced its books as promised in fiscal 2017-18 while still cutting hydro bills by 25 percent. That was a significant reprieve for Ontario rate-payers who had seen residential bills rise about 70 percent between 2008 and 2016 compared with an average 34 percent across Canada, according to a Fraser Institute report.

Auditor’s Censure

But the plan has drawn a rebuke from the Auditor General of Ontario who said in a report the government was “making up its own accounting rules” by creating “a needlessly complex” structure that would cost Ontarians as much as C$4 billion more in interest expense. The government, the auditor said, didn’t keep the office sufficiently informed about the plan as it was “acutely aware” the auditor would take issue with it.

“There was a willingness to incur an additional cost in order to get the accounting solution that they wanted,” Auditor General Bonnie Lysyk said in an interview in Bloomberg’s office in Toronto. “They intentionally kept us out of the discussion.”

Other bond market investors are also skeptical.

“It’s typical government mismanagement and focusing on popularity today and not the long-term fundamental health of the province,” said Mark Carpani, who helps manage C$1.2 billion as head of fixed income at Toronto-based Ridgewood Capital Asset Management and is also staying clear of the debt.

Fairer Way

“The creativity entails a lot of fixed costs,” added Randall Malcolm, managing director for total return fixed-income at Sun Life Investment Management in Toronto, which has C$37 billion in money market and fixed income assets and doesn’t hold Fair Hydro Trust bonds.

For its part, the government said the plan meets Canadian public sector accounting standards and has been approved by top accounting firms including EY and Deloitte, the Office of the Provincial Controller, and numerous third-party advisers. “It is a fairer way to pay for our electricity investments, and it keeps the cost of borrowing within the rate-base, not the tax-base, because that’s the logical thing to do, and that is how it has been done for decades,” Drew Davidson, a spokesman for the Ontario Liberal Party, said in an email.

Both the premier’s office and the Ministry of Energy declined to comment saying they’re in caretaker mode during the election period.

Liberals Lag

If the government had hoped to garner votes with its electricity-price cut, the plan has badly misfired. A poll tracker from the Canadian Broadcasting Corporation has about an 82 percent probability of the Progressive Conservatives, led by Doug Ford -- brother of late Toronto Mayor Rob Ford -- will win the election. The party is running neck-and-neck in the popular vote with Andrea Horwath’s New Democratic Party. Wynne’s Liberals are staring at an historic defeat.

While the structure is new to Canada, it’s relatively well-known in the U.S. where utilities have been issuing securities backed by cost-recovery charges since the 1990s. In 2013, New York State set up an agency that issued bonds backed by customer charges to help retire debt of the Long Island Power Authority after Hurricane Sandy left 90 percent of the utility’s customers, or 200,000 homes, without power.

But Fair Hydro bonds aren’t the same proposition, said Bill Girard, a portfolio manager who helps oversee about C$30 billion in fixed income at 1832 Asset Management LP.

“No infrastructure was paid for from the proceeds of these or future issues,” like other issuers which were used to fund actual power assets, Girard said.

Debt issued by New York’s Utility Debt Securitization Authority got AAA ratings, while Fair Hydro Trust received a rating of AAA at DBRS and lesser Aa2 rating at Moody’s Investors Service. Both DBRS and Moody’s listed a change in the program -- perhaps by a new government -- as the top challenge to the trust’s ratings. While Ontario has agreed to guarantee the trust’s debt-service payments upon legal changes, the pledge is not as robust as in U.S. programs, the rating company said.

Both Ford and Horwath have both said they want to cut hydro rates further and whoever wins will have to deal with a bond-market legacy designed to offer short-term relief for long-term cost.

“They basically kicked the can down the road,” according to Anthony Scilipoti, chief executive officer of Veritas Investment Research which said in its report that Ontario used a flawed and misleading approach to Fair Hydro Plan’s accounting. “The reality is our children have to cover this debt.”

--With assistance from Dave Merrill.

To contact the reporter on this story: Maciej Onoszko in Toronto at monoszko@bloomberg.net

To contact the editors responsible for this story: Christopher DeReza at cdereza1@bloomberg.net, ;David Scanlan at dscanlan@bloomberg.net, Jacqueline Thorpe

©2018 Bloomberg L.P.