Why the Future of Brazil’s Economy Rides on Pensions

Why the Future of Brazil’s Economy Rides on Pensions

(Bloomberg) -- Latin America’s largest economy, Brazil, will implement significant changes to its costly pension system. That was the focus of the first sustained legislative drive by President Jair Bolsonaro, his economic team and allies. Efforts to muster support for a major reform failed under previous administrations. Now, Brazil’s Senate has given the final approval to a reform that could boost the nation’s public finances and open the door to a virtuous cycle of expansion.

1. Why is pension reform so important?

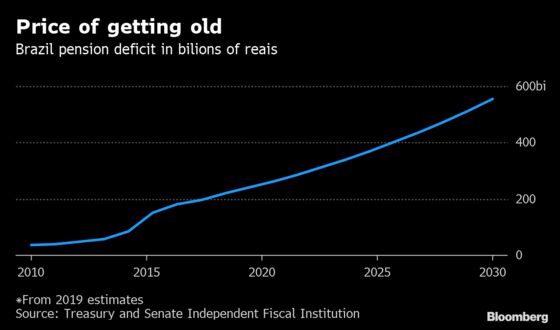

Brazil’s pension expenditures are already high compared with those of other countries, and a rapidly aging population makes the current system a ticking time bomb. Brazil spends the equivalent of 13% of gross domestic product on social security, well above the average of 8% for G-20 nations, according to a government report. On pensions specifically, Brazil spends the equivalent of 8.6% of GDP. The pension fund for private sector workers is expected to run a deficit of 218 billion reais ($54.3 billion) this year, up from 195.2 billion reais in 2018, while the fund for public servants will also be in the red. The number of citizens over the age of 65 will jump to 25.5% of the population in 2060 from just 9.5% now, according to the national statistics agency.

2. What is Bolsonaro’s plan?

His government, under Economy Minister Paulo Guedes, will establish minimum retirement ages of 65 for men and 62 for women. For workers in urban areas, the minimum contribution time will be 20 years for men and 15 years for women. (Currently, retirement is determined by a formula that considers both age and contribution time, allowing some people to claim benefits as early as in their 50s.) Those changes, along with a tax increase on banks, were initially supposed to generate 1 trillion reais in savings over 10 years, though modifications to the bill reduced that amount to about 800 billion reais.

3. What’s been the response?

Bolsonaro’s government made headway in winning lawmaker support by ceding on several points. State and municipal pensions were exempted from the reforms, for instance, and a plan to implement individual pension savings accounts was shelved. Such compromises helped speed up a cumbersome voting process that had hit snags earlier this year.

4. Where do things stand?

Brazil’s Senate approved the pension bill in two mandatory floor votes, which followed its passage in the lower house earlier in the year and marked the end of an eight-month-long legislative process. In the final vote, the measure was backed by 60 senators, well above the 49 required. The bill will officially go on the books once Davi Alcolumbre, as head of Congress, signs it into law in November. No further action will be required by Bolsonaro or his economic team.

5. What are investors hoping to see?

Investors reacted positively when the proposal was first made public in February and remained optimistic as many of its main points remained intact even after weeks of debate. A central belief in financial markets has always been that the closer the projected savings are to 1 trillion reais, the better. Many had expected a final number closer to 700 billion reais, lower than the roughly 800 billion reais that the bill would guarantee in its current form. Indeed, financial markets rallied during the final days before the reform’s final approval in the Senate. The benchmark Ibovepsa stock exchange surged to a record high while the real also gained and a key gauge of country risk tumbled.

6. What would have happened had reform efforts failed?

Failure to change the pension system would have most likely prompted a massive selloff. Analysts would have lowered their forecasts on local assets ranging from the stock market to the currency. Ratings agencies could have downgraded Brazil’s sovereign debt rating further into junk, thus raising the government’s borrowing costs as pensions swallowed up an ever-increasing percentage of the budget. The central bank would have likely been forced to raise the benchmark interest rate to fend off inflationary pressures from a weaker real and help prevent sharper declines in investor confidence. Put together, those factors would have hamstrung Brazil’s already slow recovery in investments and economic growth.

The Reference Shelf

--With assistance from Josue Leonel, Vinícius Andrade and Patricia Lara.

To contact the reporters on this story: Rachel Gamarski in Brasilia at rgamarski@bloomberg.net;Simone Iglesias in Brasília at spiglesias@bloomberg.net;Mario Sergio Lima in Brasilia Newsroom at mlima11@bloomberg.net

To contact the editors responsible for this story: Juan Pablo Spinetto at jspinetto@bloomberg.net, ;Walter Brandimarte at wbrandimarte@bloomberg.net, Matthew Malinowski, Laurence Arnold

©2019 Bloomberg L.P.