Why Machine Learning Hasn't Made Investors Smarter

Why Machine Learning Hasn't Made Investors Smarter: QuickTake

(Bloomberg) -- Hedge funds have been in the doldrums and face mounting pressure to justify their fees. Will artificial intelligence come to the rescue? A growing number of hedge funds are putting money behind the idea that a branch of AI called machine learning could provide a way to get back on top. The problems? It’s hard, expensive and prone to failure.

1. What’s machine learning?

A software program that searches for regularly occurring patterns in more data than even the most sleep-deprived junior analyst could examine, and then tests its hypotheses against even more data. What can satellite shots of mall parking lots tell you when combined with in-store sales data? Does a default premium of A to B and a yield curve slope of C to D have an E percent chance of boosting a stock price by F percent or above? If a company’s chief executive or a central bank official uses specific words, does that have an impact on asset prices? Put me in, coach, the algorithm says, I’ll figure it out.

2. Is everybody trying this?

Lots of funds, big and small, are testing the waters. Fifty-eight percent of managers in one survey said machine learning will have a medium-to-large impact on the industry. Hedge fund giant Bridgewater Associates and Man Group Plc as well as Highbridge Capital Management and Simplex Asset Management in Japan are among firms developing machine learning or investing in it. Renaissance Technologies and Two Sigma have used the techniques for a long time. In a potential source of capital for AI funds and signs that the strategy is slowly becoming mainstream, JPMorgan Chase & Co.’s asset management arm is planning to invest in emerging and established machine-learning statistical-arbitrage hedge funds.

3. Is it hard to do?

Finding patterns isn’t that hard; finding ones that work reliably in the real world is. Financial data is very noisy, markets are not stationary and powerful tools require deep understanding and talent that’s hard to get. One quantitative analyst, or quant, estimates the failure rate in live tests at about 90%. Man AHL, a quant unit of Man Group, needed three years of work to gain enough confidence in a machine-learning strategy to devote client money to it. It later extended its use to four of its main money pools.

4. What’s the problem?

There are several. If you let the programs roam too freely through the world of data, they can find meaningless patterns, such as U.S. GDP and the S&P 500 Index tending to gain or fall in lockstep with the homicide rate in England. But when quants complicate their models, adding too many parameters to get the results they seek -- a problem called over-fitting -- they can also flop.

5. Are there other complications?

Several! One concerns how to convince investors to invest in “black boxes” -- programmers know the data a machine learning program analyzed, but how it arrived at its conclusions is a mystery. Another: If people don’t know how the computer is making decisions, who’s responsible when things go wrong? The first known legal case of humans going to court over investment losses triggered by autonomous machines has been filed in London court, pitting Samathur Li Kin-kan, whose father is a major investor in Shaftesbury Plc, which owns much of London’s Chinatown, Covent Garden and Carnaby Street, against Raffaele Costa, who has spent much of his career selling investment funds for the likes of Man Group Plc and GLG Partners Inc. A trial is scheduled to begin next April.

6. Why do they fail?

Many algorithms wash out during so-called backtests, when their predictions based on historical data can’t be replicated using a new data set. Or if firms fail to fully understand what effect their algorithm is capturing, they may not know when to switch it off. And some run afoul of market realities. Tucker Balch of Lucena Research came up with an algorithm whose backtesting suggested impressive risk-adjusted returns. But the formula was focusing on thinly traded equities, and the act of buying in the real market caused prices to rise. “Ignore your market impact at your own peril,” Balch said. And then there’s the unexpected. Few algorithmic trading strategies developed so far would cope well with a Brexit vote or terror attack.

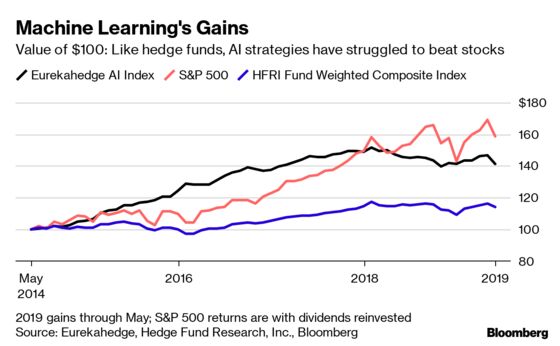

7. How are the machines doing?

So far, not so well. Machine-learning has yet to deliver Earth-shaking returns. The Man AHL Dimension fund, which includes a machine-learning strategy, has returned an annualized 1.1% in three years through March, compared with an almost 5% gain for the average hedge fund. The Eurekahedge AI Hedge Fund Index, which tracks money pools that use AI as part of their core strategies, has returned 7.1% annually in five years through May, according to the latest data available. That compares with an annualized gain of 9.65% for the S&P 500 with dividends reinvested.

The Reference Shelf

- A timeline on the development of AI for investment.

- A story on whether machine learning is more hype than revolution, and one on the first lawsuit of AI-driven losses.

- QuickTake explainers on artificial intelligence and computerized high-speed trading.

- A story on how hedge funds are embracing machine learning.

- Apple hired an artificial intelligence expert to compete against Google, Microsoft and Amazon in machine learning.

- Bloomberg View columnist Noah Smith sees machine learning disrupting white-collar work, in a good way.

©2019 Bloomberg L.P.