Why It Matters That the FRA-OIS Spread Is Widening

Why It Matters That the FRA-OIS Spread Is Widening

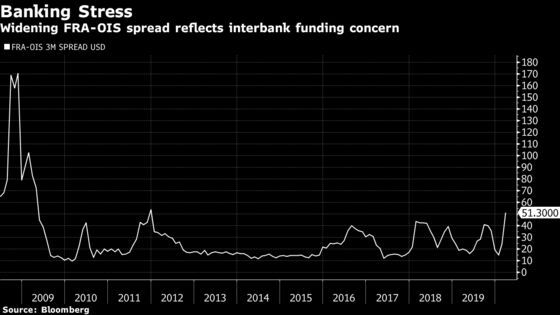

(Bloomberg) -- With the 2008 global financial crisis still in the rear-view mirror, the coronavirus and a plunge in oil prices have put jittery markets on the alert for signs of another credit crunch. That helps to explain why one important indicator of stress in the U.S. banking system -- the FRA-OIS spread -- is drawing attention. The spread has spiked to its widest level in more than eight years, even if it’s way off the highs of 2008 and 2009.

1. What’s the concern?

Right now it boils down to deteriorating market sentiment about credit and recession risks rather than a genuine fear of a pullback in funding markets. The widening of the FRA-OIS spread -- seen by many as a proxy for risks in the banking sector -- reflects concern that companies will struggle as the new coronavirus exacts its toll on the economy. That makes interbank lending more risky, since banks stand to suffer losses if companies fail. The perceived added risk means banks will demand higher interest payments to lend to one another -- hence the increase in the spread. The forward rate is also a gauge of market expectations for additional Federal Reserve interest rate actions.

2. How bad is it?

The spread has approached the levels in 2011 of close to 60, but is nowhere near the financial crisis peak of around 170 in November 2008. Strategists at Natwest Markets are concerned that there are “skeletons in closets” they may not be aware of that come out in times like this, particularly in small-to medium-sized business that may not have two months of cash to ride out declining sales.

3. What is FRA?

A forward rate agreement is a deal to swap future fixed interest payments for variable ones, or vice versa. The key rate for U.S. markets is the three-month London interbank offered rate, or Libor, in U.S. dollars. The benchmark is derived by major banks submitting rates based on transactions that are compiled to establish benchmark for five different currencies across seven different loan periods. Those benchmarks underpin interest rates on trillions of dollars of financial instruments and products from student and car loans to mortgages and credit cards.

4. What is OIS?

The Overnight Index Swap rate is calculated from contracts in which investors swap fixed- and floating-rate cash flows. Some of the most commonly used swap rates relate to the Federal Reserve’s main interest-rate target, and those are regarded as proxies for where markets see U.S. central bank policy headed at various points in the future.

5. What does the FRA-OIS spread show?

It’s regarded as the markets’ measure of how expensive or cheap it will be for banks to borrow in the future, as shown by Libor, relative to a risk-free rate, the kind that’s paid by highly rated sovereign borrowers such as the U.S. government. The FRA-OIS spread provides another snapshot of how the market is viewing credit conditions because of the fact that traders are betting on where Libor-OIS -- its underlying spread -- will be.

The Reference Shelf

- QuickTakes on the repo market blowup and central bank options to boost economies.

- Another QuickTake on the end of Libor.

- Widening Libor-IOS spread is credit-driven, not liquidity: Bloomberg Intelligence.

To contact the reporter on this story: Alexandra Harris in New York at aharris48@bloomberg.net

To contact the editors responsible for this story: Nick Baker at nbaker7@bloomberg.net, Grant Clark

©2020 Bloomberg L.P.