Why IMF Help for Poor Nations Will Benefit Rich Ones

Why IMF Help for Poor Nations Will Benefit Rich Ones

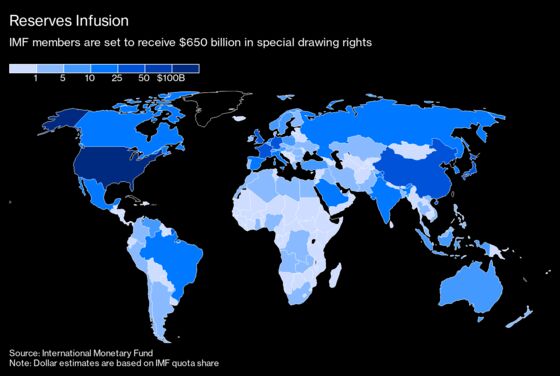

(Bloomberg) -- The International Monetary Fund’s member nations are nearing their biggest resource injection in its history, $650 billion, to boost global liquidity and help emerging and low-income nations deal with mounting debt and Covid-19. The choice of vehicle -- reserves known as special drawing rights, to be allocated on Aug. 23 -- has drawn some criticism. U.S. President Joe Biden reversed the stance of his predecessor, Donald Trump, that the IMF plan didn’t do enough to target the aid to poorer countries. The U.S. is the IMF’s largest shareholder and carries a de facto veto on such matters.

1. What are special drawing rights?

SDRs are an international reserve asset that can be converted into five currencies: the dollar, euro, yen, British pound and yuan. When SDRs are allocated by the IMF, recipient nations can hold them as part of their foreign currency reserves or exchange them for the hard currency of other IMF members. (The seller pays 0.05% interest on such sales if its SDR holdings dip below its IMF-allotted level.) The appeal of SDRs to poorer nations is that they come condition-free, unlike many of the fund’s loan programs.

2. How are they distributed?

The IMF requires they be distributed in proportion to each country’s share in the fund -- roughly equal to their economic output. That means that 58% of the new SDRs go to advanced economies, with 42% for emerging and developing economies and just 3.2% to the smaller subset of low-income nations. So of the $650 billion, according to U.S. Treasury Department calculations, about $21 billion will go to low-income countries and $212 billion to other emerging market and developing countries, without counting China.

3. What can they be used for?

Under the IMF’s rules, they must meet a global need for more long-term reserve assets and can’t fuel inflation. The last general allocation of SDRs came in response to the 2009 financial crisis. This time, some nations might put the money toward paying for vaccines and medical equipment. Argentina is said to be weighing using SDRs to make a payment due to the IMF in September toward the $45 billion it owes on a loan it received in 2018, the biggest one ever extended by the fund. The boost to reserves will also help improve the creditworthiness of high-yield bond issuers such as Pakistan and Ecuador, luring more investors to their debt markets. Many countries will simply hold onto the reserves, if 2009 is any guide.

4. Why would the IMF go this route to help poor nations?

It’s the fastest way to get resources to countries that need them, even if the lion’s share goes to richer countries. IMF loans, by contrast, take time to negotiate, and some nations in need might be reluctant to seek them for fear of creating a negative perception with investors. Also, lower-income countries are the ones most likely to convert their SDRs into other currencies to meet balance of payments and fiscal needs. Still, African finance ministers declared that the planned distribution of SDRs “would barely be adequate to meet the continent’s financing needs,” and they urged the IMF to consider ways to reallocate SDRs specifically to low-income and middle-income countries. IMF Managing Director Kristalina Georgieva has vowed “to identify viable options for voluntary channeling of SDRs from wealthier to poorer and more vulnerable member countries.”

5. What else is drawing criticism?

Like the 2009 allocation of SDRs, this one has critics who argue that such unconditional financing contributes to moral hazard, could fuel inflation and provides added international reserves the world doesn’t need. Some Republicans in Congress say the new SDRs will be used to pay off the developing world’s debts to China -- loans that might otherwise be restructured or even written off entirely -- and bankroll U.S. adversaries including Iran, Venezuela and Russia. (The U.S. Treasury Department says it will refuse to purchase SDRs from any country with which it currently has sanctions -- a list that includes Iran, Syria and Venezuela -- and will work with other countries to convince them to do the same.) The G-20 has called on the IMF to find ways to enhance transparency and accountability in the use of SDRs.

6. Is there a way to get more money to poor countries?

Wealthier nations can already channel part of their SDRs via the IMF’s Poverty Reduction and Growth Trust. IMF staff also are working to set up the so-called Resilience and Stability Trust by year-end, which would allow wealthier nations to redirect reserves to vulnerable low-middle-income countries. The Group of Seven nations endorsed a plan to reallocate $100 billion of new SDRs to poorer nations in June. But the G-20 in July kept support limited to the general allocation of SDRs, without specifying the amount that might be re-lent.

7. Who stands to benefit?

UBS AG economist Arend Kapteyn estimates the new SDRs will boost global foreign exchange reserves by 4.5%, with Venezuela, Pakistan, Ecuador, Kazakhstan, Turkey and Argentina seeing some of the biggest impacts among emerging markets. All of those countries would see an increase of 10% or more in their reserves. Smaller island nations like Antigua and Barbuda and St. Lucia, greatly reliant on tourism, also would see large boosts relative to existing reserves. Morgan Stanley estimated that Chad and Zambia -- two nations that have requested debt restructuring under a framework agreed to by the G-20 -- could also see significant reserves increases.

The Reference Shelf

- An IMF fact sheet on SDRs.

- The Center for Global Development held a webinar on the impact of SDR allocation for African economies and the challenges of effective reallocation.

- The Rockefeller Foundation suggests reallocating no less than $100 billion in wealthy countries’ SDRs for low- and middle-income countries.

- The Center for Global Development asks, “How Might an SDR Allocation Be Better Tailored to Support Low-Income Countries?”

- Isabelle Mateos y Lago, a managing director at BlackRock, wrote this paper on “Managing global liquidity through COVID-19 and beyond.”

- The SDR plan “would be a clumsy and ill-targeted way” to help countries in financial distress, a former director of the IMF Institute and former deputy director of the IMF’s European Department wrote in Barron’s.

©2021 Bloomberg L.P.