Why Argentina’s Hot Delivery Item Is Cold U.S. Cash

Why Argentina’s Hot Delivery Item Is Cold U.S. Cash

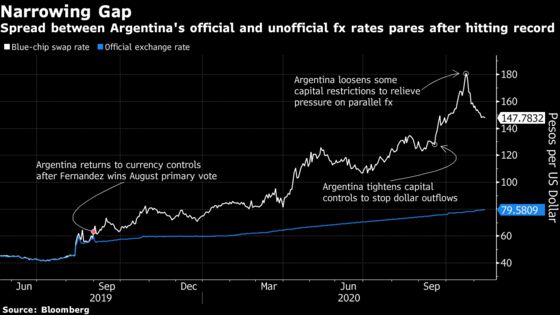

(Bloomberg) -- It’s not as if Argentina hasn’t been in economic trouble before -- its story, after all, is almost synonymous with sovereign default, including its ninth mere months ago. But rarely has it faced so many overlapping crises at once, with a pandemic-driven economic contraction coming on top of an already deep recession, inflation well into double digits, a currency crunch so bad that motorcycle couriers swarm the streets delivering black-market dollars and few prospects for help from the bond markets or international lenders. As its foreign-exchange reserves dwindle, the gap between the official and black-market exchange rate recently hit its widest in 31 years.

1. What’s happening?

Capital controls have caused a surge in demand for U.S. dollars among Argentines trying to protect their pesos against devaluation. But savers are restricted to buying just $200 a month though official channels. Anything beyond that must be done through a series of financial trades or on the thriving black market, where greenbacks -- sometimes delivered door to door via motorbike -- fetch more than 150 pesos per dollar, or almost double the official exchange rate.

2. Why is that happening?

This part of the story goes back to August of 2019, when the leftist Alberto Fernandez unexpectedly swept the Presidential primaries, sparking a rapid selloff in Argentine assets as investors anticipated another default. The president at the time, Mauricio Macri, imposed some capital controls in response. Since becoming president, Fernandez has successively tightened those controls, limiting savers and businesses from accessing dollars to protect the country’s waning international reserves, now at a four-year low.

3. Didn’t Argentina just go through a debt crisis?

It definitely had one, but whether the crisis was resolved is more questionable. Argentina defaulted for the ninth time in its history in May while negotiating with its foreign creditors to restructure $65 billion in overseas debt. Fernandez’s government said a three-year recession -- worsened by the pandemic -- had made its foreign debt payments unsustainable. In September, the government and creditors restructured the bonds, delaying significant payments for three years without sticking bondholders with a large principal haircut. But the prices of the new securities issued as part of the deal have since tumbled, as investors have turned skeptical about the economy returning to growth.

4. Why is that?

Since the restructuring, Argentina has implemented a series of patchwork policy measures to try and boost foreign reserves in the central bank, but investors say the new measures don’t go far enough to bring dollars back to the country. Investors are also reminded of the 2011-2015 presidency of Cristina Fernandez de Kirchner, now vice president, who implemented similarly draconian capital controls which led to a proliferation of parallel peso rates. Back then, the government cracked down on illegal exchange houses and monitored brokerage operations closely in a bid to curb their use and keep the peso overvalued.

5. What has the pandemic done?

Argentina endured one of Latin America’s strictest lockdowns, which showed initial success but did little to prevent cases from eventually rising, and it’s one of the top five countries with the most deaths per capita. The lockdown shuttered businesses for months, and gross domestic product is expected to contract around 12% this year, the largest drop on record. The government has tried to prop up the economy with social spending, but without access to foreign capital, it resorted to money printing to fund a soaring deficit, now at 8.5% of GDP according to data from the International Monetary Fund-- the largest since it began keeping track in 1993. While inflation was already high before the pandemic, consumer prices are expected to rise around 40% this year.

6. What are Argentina’s options?

Unfortunately, there are few good ones. The standard way to prop up a currency is by hiking interest rates to attract foreign capital, but higher rates would likely only deepen an already entrenched recession. Countries sometimes bite the bullet and devalue their currency, but by driving up the price of imports that risks even higher inflation, already expected to end the year around 40%. Further tightening the capital controls would likely cause Fernandez’s already wobbling approval numbers to slide, as locals are already exasperated by the restrictions in place. The government has begun adopting a more orthodox approach, slowing its money printing and promising not to finance itself with advances from the central bank, which has eased some pressure on the currency crisis in recent weeks.

7. Haven’t rich countries pledged to help those hurt by the pandemic?

Argentina is renegotiating its $44 billion program with the IMF. But the country has a rocky history with the Fund, and the government has been reluctant to take out more debt with the international lender. Economy Minister Martin Guzman told reporters Nov. 9 Argentina would pursue an IMF program that would give the country at least a four-and-a-half year grace period to start paying back its debt. That program is likely to come with strings attached that would require structural economic changes.

The Reference Shelf

- A 2017 QuickTake on Argentina’s financial travails.

- How cash deliveries via motorbike work.

- The IMF’s page on Argentina.

©2020 Bloomberg L.P.