Why Saudi Aramco’s IPO Is No Ordinary Share Sale

Why Saudi Aramco’s IPO Is No Ordinary Share Sale

(Bloomberg) -- Saudi Aramco’s much heralded and oft-delayed initial public offering was eventually completed -- albeit in a scaled-down version of the original plan by Saudi Crown Prince Mohammed bin Salman. There was no grand opening on the London or New York stock exchanges for the oil giant -- trading is restricted to the Saudi bourse and the shares weren’t even marketed to most money managers. Investors were able to purchase just 1.5% of the world’s most profitable company -- about half what was previously considered. Even so, Aramco’s IPO became the biggest in history.

1. Why was it scaled back?

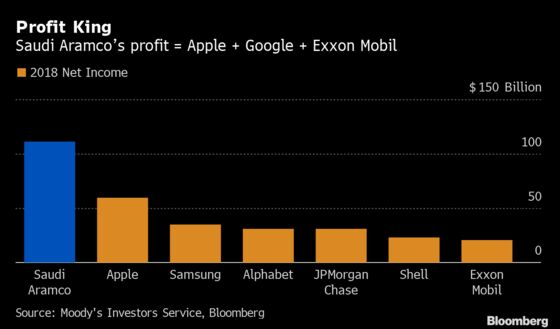

Because international investors balked at the valuation. The IPO is a key element of Prince Mohammed’s vision to wean the kingdom’s economy away from its dependence on oil. He caused something of a shock in 2016 when he announced the plan together with his valuation of $2 trillion. At the time, that would have made Aramco about four times the size of Apple Inc., the world’s biggest company by market capitalization. (Apple’s value has since soared to more than $1.3 trillion.) Although a reduced valuation of $1.7 trillion was finally settled upon, many global money managers still thought that was too high. One survey pointed to a “fair” range of $1.2 trillion to $1.5 trillion.

2. So who invested?

Saudi Arabia leaned on its allies and subjects -- and even its clerics -- to help out. Wealthy families in the kingdom, some of whom had members detained and accused of corruption by the government two years earlier, were encouraged to invest. In a sweetener, Saudi retail investors were eligible to receive one share for every 10 if they hold them for 180 days from the date of the listing in Riyadh. Hours before a local presentation in the month before the sale, the company surprised assembled bankers and investors by removing an international offering from the process, meaning Aramco didn’t market the deal directly in the U.S., Japan or Canada. A London presentation was also abandoned. The domestic focus sidelined the hoards of global banks advising on the share sales.

3. Was it a record?

Yes, and by some. After pricing at the high end of the valuation, the IPO raised $29.4 billion -- beating the record $25 billion raised by Alibaba Group Holding Ltd. in New York in 2014. The eventual total included an extra $3.8 billion raised from selling shares that were initially earmarked for trading in to help minimize price swings. Aramco shares began trading on Dec. 11, 2019.

4. Why no overseas sale?

Aside from global resistance to the Saudi valuation, there’s also the fact that an international share sale is fraught with difficulties. New York’s appeal is limited because of a U.S. law allowing victims of terrorism to sue foreign governments linked to attacks, which may lead to litigation against Aramco. Overseas listings also open the company to intense and unprecedented scrutiny. Aramco lifted the veil on its operations by releasing financial results for the first time. One advantage for the government is that a domestic listing may help the Tadawul exchange become a gateway for foreign investment into the kingdom. Aramco became a significant part of the MSCI Saudi Arabia index, meaning global fund managers tracking the index will be under pressure to buy the shares.

5. Why hold the IPO then?

The timing raised eyebrows. Saudi Arabian Oil Co, to give Aramco its formal name, pumps about 10% of the world’s oil, yet crude prices had fallen in the preceding year, and the outlook for global growth suggested at the time they may drop further. An aerial attack on Aramco’s largest processing plant in mid-September briefly wiped out half the company’s production capacity, highlighting its vulnerability as well as the region’s heightened geopolitical tensions. Saudi Arabia may have taken the view that it was better to press ahead in case oil prices continued to slide. The IPO also shone an uncomfortably bright light on slowing oil demand -- with even Aramco acknowledging for the first time that a peak might be on the horizon.

6. How attractive was the IPO?

Saudi authorities are reshaping the oil producers’ finances (most of its revenue goes to taxes and government royalties) as well as promising bumper dividends. For instance, the royalty it pays if Brent crude prices are less than $70 a barrel is falling to 15% from 20%. The “base dividend” in 2020 will be $75 billion -- much bigger than what other oil majors pay but a good deal smaller in terms of yield. Aramco is considering lifting that to $80 billion. The shares rose more than 9% in the first month of trading, for a couple of days valuing Aramco at more than $2 trillion.

The Reference Shelf

- After the world-beating IPO, the hard work begins.

- Aramco adds a sweetener, writes Bloomberg Opinion’s Liam Denning. He sums up the offering as “The World’s Biggest Dog Bites World’s Biggest Man.”

- A survey points to a valuation of $1.2 trillion to $1.5 trillion.

- Saudi Arabian stock market’s “invisible hand.”

- QuickTakes on Saudi Aramco, the crown prince and his plans to transform the economy.

- More QuickTakes on the attacks on Saudi oil facilities, Yemen’s civil war and the country’s treatment of women.

--With assistance from Paul Wallace.

To contact the reporter on this story: Matthew Martin in Dubai at mmartin128@bloomberg.net

To contact the editors responsible for this story: Will Kennedy at wkennedy3@bloomberg.net, Grant Clark

©2020 Bloomberg L.P.