Why 10-Year Treasury Yields Get All the Attention

Why 10-Year Treasury Yields Get All the Attention

(Bloomberg) -- Financial news is always awash in numbers, but there’s one figure that seems to be getting more attention than anything else: the yield on 10-year U.S. Treasury notes. Not only are investors laser-focused on it, but gyrations in other asset classes have been driven by its movements this year. Increases that reach market milestones could have big implications for everything from U.S. stock prices to the value of emerging-market securities. Some observers are speculating that the yield’s sharp rise in 2021 may mark a sea change in the era of historically low rates and inflation.

1. What are Treasuries and why do they matter?

To understand the focus around 10-year Treasuries, it helps to take a step back. Treasury securities are debt obligations of the U.S. government and the primary way it taps investors for funds to finance spending that exceeds the revenue it takes in. (It’s been running a budget deficit since 2001, and the pandemic is driving borrowing up steeply.) Investors care about the prices at which Treasury notes and bonds change hands, but it’s their yields -- broadly speaking, the total annualized rate of return for buy-and-hold investors -- that are more telling. That’s because they show the interest rate the government has to pay to borrow for different lengths of time. They also provide a benchmark for other borrowers, like companies and homeowners with mortgages.

2. What kind of lengths do Treasuries come in?

Just as individuals can borrow money for different periods of time, the U.S. government has IOUs of various maturities. Some of the securities it sells are bills that come due in as little as a few days, while its longest-dated bond matures in 30 years. In between these are a whole range of maturities, including the 10-year note, which it issues on a regular basis.

3. Why is the 10-year yield so important?

Investors are keenly attuned to rates across the so-called yield curve, but its various segments -- and the gaps between them -- can indicate quite different things. Short-term rates, for example, are heavily influenced by the choices of the U.S. Federal Reserve, which has said it plans to keep its policy rate locked near zero for several years. Long-term yields, on the other hand, have more freedom to move, making them barometers of investors’ outlook for economic growth and inflation. With very long bonds, like 30-year issues, uncertainties are greater, so many focus their attention around the 10-year security instead. The result is that the 10-year note is one of the world’s most important benchmarks for the cost of risk-free borrowing and its rate is used to price trillions worth of other securities.

4. How does the 10-year yield affect other assets?

All returns are relative: Investors weigh choices not in the abstract, but in comparison to the risks and rewards offered by other assets. The 10-year Treasury yield is a handy yardstick against which investors can compare possible returns or losses on riskier assets, such as stocks or corporate loans. A rise in the 10-year yield can therefore be bad for stocks, because investors may have less to gain from taking on more risk. It can also undermine stock prices by delivering a hit to discounted values of company cash flows. That’s especially true for growth stocks -- heavily represented by tech firms -- given that much of their income streams are expected well in the future.

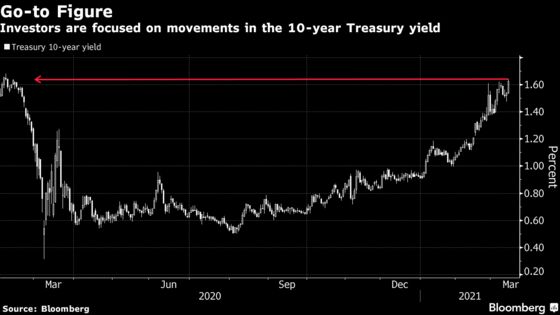

5. Is there one key yield level that matters most?

Yes and no. The 10-year yield hovered around 1.61% in mid-March, up from less than 1% at the start of 2021 and as little at 0.31% during the market turmoil of March 2020. Around 2% -- give or take -- is becoming a hot forecast for the end of the year. Strategists at BMO Capital Markets are eyeing 1.75% as the next key mark, a level last seen in January 2020, weeks before the pandemic sent markets into a frenzy. As the yield keeps inching higher, some are warning it will set off triggers for a round of so-called convexity hedging, a practice related to holdings of mortgage debt that can amplify swings in yield levels. The increase in yields over the past year -- with the 10-year up over a percentage point -- has already put it above the dividend yield on the S&P 500.

6. Has the 10-year always been so important?

In decades past, all eyes used to be on entirely different indicators, like central bank money supply numbers, to divine the path of Fed policy, although the central bank regime that underpinned that kind of analysis has long since shifted. More recently, traders were very focused on money markets and other shorter-term rates to gauge other investors’ expectations for the path of the Fed’s main target. This has not disappeared. Even with the Fed indicating now that it will likely keep its policy rates near zero through the end of 2023, markets are not so convinced and observers remain glued to indicators derived from money market trading, such as Eurodollar futures and overnight index swaps. But with investors around the world trying to assess growth and inflation risks, the focus on the 10-year has become that much more acute.

7. What does the Fed think about the increase in yields?

Even as yields have surged and traders bring forward the timing of the first rate hike, the Fed has signaled that it plans to keep monetary policy accommodative for years to fight the pandemic’s long-term damage. While Fed Chairman Jerome Powell recently acknowledged that the run-up in bond yields was “notable” and caught his attention, he indicated that he would be concerned if there were “disorderly conditions in markets or persistent tightening in financial conditions” that threatened the achievement of the central bank’s goals.

8. When happens if the markets and the Fed disagree?

Sometimes the Fed has been right, but on other occasions the market has been more accurate. Back in 2014, for example, central bank officials signaled that the pace of growth and inflation would warrant aggressive monetary policy tightening over the coming years. Fixed-income traders said that was way off, a forecast that proved more accurate, with the central bank going on to lift rates just once in 2015 and once in 2016 -- much closer to what the market had predicted.

©2021 Bloomberg L.P.