Why Direct Lending Is a Booming Part of Private Debt

Who Needs a Bank? Why Direct Lending Is Surging

(Bloomberg) -- What’s direct lending? Old-fashioned bank lending -- without the bank. As tougher regulations reshaped the post-financial crisis landscape, traditional banks have cut back on business lending. That’s created a raft of opportunities: For a growing group of asset managers who are making the loans, for borrowers and for investors looking for an answer to low-yield woes. Increasingly, that last group includes hedge funds and buyout firms who are dishing out billions of dollars at a time to lure borrowers away from the $1.3 trillion leveraged loan market. For regulators, the question is whether the market can sustain such growth without making a mess.

1. How does direct lending work?

It starts with asset managers -- initially, mostly hedge funds and private-equity funds, but now other types of investors as well, including insurance firms -- raising pools of money from investors interested in higher-yielding debt. The managers field pitches from debt advisers with investment opportunities, or other private-equity funds looking to finance acquisitions. The direct-lending fund does its own research before deploying its money. Direct lenders tend to hold onto the loans long-term, sometimes offering growth support to the company and entering into multiple funding rounds, although some do sell a small proportion of their debt.

2. Who borrows from them?

In the past, it’s typically been what are known as smaller “mid-market” businesses that banks are no longer interested in lending to. Their need for credit and lack of good alternatives means direct lenders have historically been able to extract higher interest rates -- though reaching those juicier yields has become more challenging amid increased competition for business. More recently, some big companies have turned to direct lenders for large loans. For instance, plane and train maker Bombardier Inc. recently said it scored a $1 billion loan from HPS Investment Partners, on the heels of one of the largest private deals ever: for the Ardonagh Group, a European insurance brokerage, which was able to negotiate a 1.875 billion-pound ($2.4 billion) debt package from a small group of private lenders led by Ares Management.

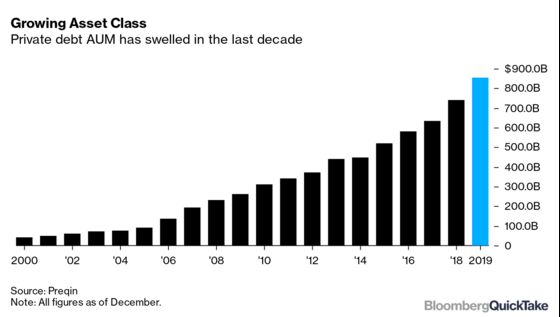

3. Why is direct lending in the news?

Direct lenders are consistently accumulating large sums of money and pursuing different types of deals. Direct lending is by far the most popular strategy in the approximately $850 billion private credit asset class, though special situations and distressed strategies are picking up steam amid the coronavirus pandemic. As of December, direct lending made up a $314 billion slice of private debt -- with $95 billion of that consisting of dry powder, according to Preqin. Of the $239 billion targeted for new private lending vehicles, nearly half of that is earmarked for direct lending.

4. Where are the deals happening?

The U.S. remains the most mature direct lending market, with the bulk of the deals occurring in its borders. The European market has also boomed, and is on pace to snag a larger part of the leveraged finance market as cash has streamed into funds for this purpose. And in Canada, burgeoning interest in alternative credit is spurring several new private debt funds, as some investors are seeing a better outlook north of the border as the U.S. faces oversaturation and thinning returns. Private credit funds have emerged in Canada as pension funds, endowments and life insurance companies hunt for yield. These non-traditional sources of debt are filling a gap as new regulations and capital requirements make it too onerous for the country’s big banks to lend to smaller and riskier companies.

5. How are the deals changing?

In the U.S. and Europe, intense competition for deals has led to weaker protections for lenders in many cases -- though some of that loosening has been clawed back in the wake of Covid-19. It’s similar to what’s happened in the larger market for broadly syndicated loans. Borrowers that have previously tapped the traditional leveraged loan market for their debt are increasingly pursuing direct loans instead as well. And the growing firepower of private debt funds mean they have been able to write bigger checks for single deals.

6. What’s driving the growth?

Investor demand, due to the search for yield. And a sort of virtuous cycle -- as more money comes into direct lending, fund managers are able to write bigger loans, which makes direct lending even more attractive. Asset-management firms are raising a lot of money from pension funds, institutional investors and family offices that need to deploy cash and find yield in a low-rate environment. There’s also demand for funding from small- and medium-sized enterprises (SMEs) that have struggled to get loans from the more cautious banks and are unable to issue bonds. At the riskier end of the high-yield spectrum, direct lenders can be attractive to companies facing business-specific or sector-wide challenges. Goldman Sachs estimates that expansion outside of North America could add as much as $370 billion to private debt overall in the medium term.

7. How risky are the loans?

Getting riskier. That started even before the pandemic: As the cycle reached its later stages, credit quality deteriorated across the board. While the direct-lending business grew up concentrating on solid, safe companies that were just too small for banks, a growing number of direct lenders are extending more speculative debt financing to more distressed companies and making bigger bets that could bite if things go sour. Now, credit grader Fitch Ratings projects that middle-market debt -- a category most direct lending falls under -- could hit a 7% to 8% default rate by the end of this year, with sectors like restaurants, casinos, movies theaters and others affected by virus-related shutdowns hit hardest.

8. What’s the case for direct lending?

The main thing is that direct lenders say yes to companies that banks don’t want to lend to. And as direct lenders are not as constrained by capital requirement guidelines, they are able to take on companies with higher leverage, which means attractive returns for investors if the deal runs smoothly. Private equity firms often go this route to secure faster financing for buyouts.

9. What are its downsides?

The extra leverage that can make direct loans look more attractive could put a damper on recoveries. Borrowers might not like the fact that a single lender can have more power in negotiations than a group might. An up-tick in creative earnings calculations, which may soon include adjustments for coronavirus, could also set up borrowers in the space for tighter credit conditions and more downgrades. New entrants that are spending more time tending to their own portfolios in the wake of the pandemic could face out-size losses and miss out on attractive deals. Though the industry as a whole may outperform the junk bond and leveraged loan markets, there will be a wide dispersion between winners and losers among the credit managers.

The Reference Shelf

- QuickTake explainers on leveraged loans, shadow banking and private credit.

- A Deloitte report on global direct-lending deployment.

- A Bloomberg feature the growing footprint of direct lending.

- An Ares whitepaper on the rise of the private markets.

©2020 Bloomberg L.P.