What’s NUE in India and Why Does Amazon Want a Piece?

Amazon, Facebook and Google are lining up for the chance to build a new platform to handle electronic money flows in India.

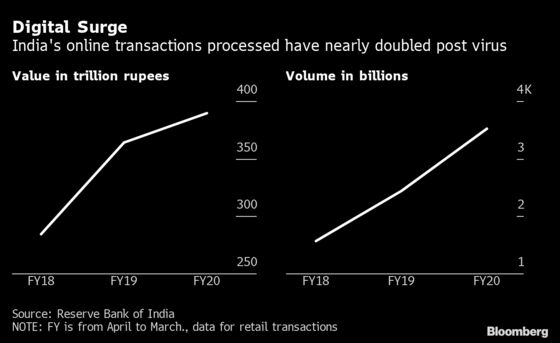

(Bloomberg) -- Cash may be king in India, but with smartphone usage heading toward 1 billion, online payments are catching up. Digital transactions doubled in the last two years, faster than any major country outside China, and are forecast to reach $2 trillion in 2023. Such exponential growth hasn’t been trouble-free, however, leading to concern about the wisdom of relying on a single payments system. That has global tech giants including Amazon, Facebook and Google lining up for the chance to build a new platform to handle electronic money flows -- and reap an expected bounty in fees.

1. What’s the system now?

Digital transactions are processed by the National Payments Corporation of India, a non-profit, umbrella organization backed by more than 50 retail banks. In operation since 2016, its Unified Payments Interface allows users to link their mobile phone numbers to their bank accounts. That’s made transferring and receiving money via apps as easy as sending a text message, at minimal cost. With several payment apps to choose from and a quick and simple interface, its popularity has soared: The platform processed transactions amounting to 31.7 trillion rupees ($450 billion) from April 2020 to January 2021. It handled about half of India’s nearly 41 billion retail online transactions, which are expected to double this year.

2. What’s the problem?

As the traffic builds, it’s getting riskier to depend on one system. During the pandemic, with people spending more time at home and relying on the internet for shopping and entertainment, there’s been a rising incidence of internet fraud, cyber-crimes and transactions that got reversed or declined, including at top banks and NPCI. In February, some transactions by mutual fund investors were disrupted during an upgrade of the system. To address the “risk concentration” of only one platform and offer consumers more options, the Reserve Bank of India in 2020 invited private companies to bid for a license to set up a new platform.

3. What’s the lure?

Referred to (for now) as the New Umbrella Entity or NUE, the platform will be for-profit and allowed to charge fees for transactions, unlike the existing system. The new entity or entities will be able to earn interest from the float that customers maintain in their online shopping accounts. A promoter will hold at least 25% and up to 40% in the operator and must be an Indian resident. Foreign companies can own a maximum 25%, so are teaming up with local players. The deadline for applications is March 31, and the selection process is expected to take several months. It’s possible two licenses might be awarded for two new networks; the RBI hasn’t been specific.

4. Who has applied?

So far six groups:

- A consortium consisting of Amazon, Visa Inc., Indian private lenders ICICI Bank Ltd and Axis Bank, and two financial-services startups, Pine Labs and BillDesk.

- Another group is led by Asia’s richest man, Mukesh Ambani, and his Reliance Industries, partnering with Facebook and Alphabet Inc.’s Google, which invested more than $10 billion in Reliance’s digital services unit, Jio Platforms, in 2020.

- India’s digital payments leader Paytm has joined with ride-hailing startup Ola and at least five companies.

- The Tata Group -- India’s biggest conglomerate -- combined with Mastercard Inc., telecom operator Bharti Airtel Ltd and two Indian banks, HDFC and Kotak.

- Financial Software and Systems is applying with Indian Bank, Central Bank of India, National Bank for Agriculture and Rural Development and India Post Payments Bank Ltd.

- U.S.-based payments firm FIS joined with Union Bank of India and Punjab National Bank.

5. What’s in it for customers?

The systems will operate in parallel, increasing options for users. Those running the platforms will have to compete, possibly offering incentives to online vendors in a bid to gain market share. Eventually that will help boost transaction volumes for both platforms as e-commerce expands and reaches deeper into India’s unbanked hinterland. In the World Bank’s most recent report on financial inclusion in 2017, some 190 million Indians did not have a bank account and more than half did not make or receive digital payments. A key benefit: Customers faced with a failed transaction currently have few options. In the new regime, they’ll be able to try the other platform.

The Reference Shelf

- More QuickTakes on India’s “bad bank,” why farmers are worried, and the tensions with China.

- Bloomberg Opinion’s Andy Mukherjee on India’s digital currency and the battle for supremacy in its retail landscape.

- Businessweek looks at India’s smartphone frenzy.

©2021 Bloomberg L.P.