What's a 'Term Premium,' and Where Did Mine Go?

What's a 'Term Premium,' and Where Did Mine Go?

(Bloomberg) -- In olden days, like before the 2008 financial crisis, it was a given that Treasury investors would demand greater compensation for lending for longer periods. Those so-called term premia -- higher interest rates for long-term borrowers-- reflected the greater risk of, say, inflation rising over 10 or 20 years. But term premia shrank and then disappeared, lurking below zero much of the time between late 2014 and early 2021. That’s all changed now, as yields surge in a shift that many think will mark a sea change in relations between lenders and borrowers, including the U.S. government.

1. What exactly is a term premium, anyway?

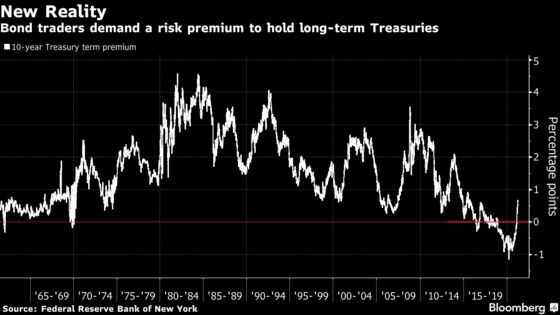

It’s the difference between what you get for locking up your money for an extended period and what you would get if you simply kept rolling over short-term instruments for the same amount of time. Many investors and analysts use the term premium on a Treasury note to help decide if it’s worth buying. By one Federal Reserve model, the term premium that 10-year Treasury bonds offer has averaged about 1.56 percentage points since 1961. It hit an all-time low of -1.15 percentage points in March of 2020. It hovers now at about 0.61 percentage points.

2. Why reward holders of longer-term bonds?

The longer you lend money to someone (or, in this case, a government) for, the more time there is for things to go wrong. Former Fed boss Ben S. Bernanke says that in his analysis the term premium reflects the buffer that investors need to account for two key risks. One is changes in demand for or the supply of bonds, which can affect prices. The other is inflation, which would reduce the real value of future bond payments. When investors feel more uncertain on either point, they demand a bigger premium in the form of higher rates.

3. How is that different from a yield curve?

Yield curves are a way of measuring the difference between what someone gets for investing their money for entirely different periods, say for two years versus 10 years. That gap includes the term premium along with other variables, including a premium for liquidity that reflects how hard or easy it is to trade the securities.

4. What’s been going on with term premia?

Long-term Treasury yields, that had been stuck below 1% since March 2020, have become unmoored from that mark this year, as visions of a strong post-pandemic economy has investors recalculating the risk of inflation. More than half of the force for that rise has come from a jump in term premium, with the rest due to a projection of the Fed moving its policy rate higher at some point. The New York Fed’s ACM model for 10-year term premium broke above zero in February, the first time that’s happened since 2018. That put an end to it being actually a discount, meaning the term premium was negative, for much of the time for years before that. Other factors have also come into play.

5. What else is driving term premia up?

There’s also a supply-demand dynamic. For one thing, the huge surge in borrowing by the Treasury to fund trillions in pandemic-relief spending will continue. For another, the Fed is siphoning off less of that new supply because it’s buying fewer bonds than it did in 2020, when it scooped up about $2.4 trillion of Treasuries as part of its pandemic crisis response. The Fed is currently buying $80 billion worth of Treasuries a month as part of its asset purchase program, a pace that would total $960 billion for all of 2021. So even though the Treasury’s expected 2021 net debt issuance will be less than last year’s record of more than $4 trillion, private investors will have to buy more given the Fed’s smaller presence in the market this year, according to forecasts by JPMorgan Chase & Co.

6. Why might it rise more?

Most Wall Street strategists see room for the term premium to move higher. Praveen Korapaty, chief rates strategist at Goldman Sachs Group Inc., says it’s reasonable to foresee it rising back to where it averaged during the 2010 to 2014 period, before it dove hard below zero. By the Fed ACM model, the average during that window was about 1.5 percentage points. Additional increases in term premia seem probable because investors will likely demand even more compensation for the risk of inflation, given that the Fed has adopted a new policy schema in 2020. Instead of regarding its 2% inflation target as a hard ceiling, the Fed’s new approach will be to allow price pressures to run hot for a while during a recovery, to average 2% inflation over time. Roberto Perli, a partner at Cornerstone Macro LLC and a former Fed economist, also sees strong odds of the term premium rising further. Yet Perli warns that if things go surprisingly sour with the economic recovery -- if new variants of the virus, for instance, cause a resurgence that prompts new business lockdowns -- it may dip again.

The Reference Shelf

- An explainer on inflation averaging from the Fed.

- Former Fed Chairman Ben S. Bernanke’s blog on the term premium.

- The Federal Reserve Bank of New York’s term premium model.

- A New York Fed blog post on the potential impact of monetary tightening on term premia.

- A Bank of International Settlements report on term premium.

- A Bloomberg story on term premium model changes in the post-QE era.

- The Fed’s report on how its asset purchases affected long-term rates.

©2021 Bloomberg L.P.