Current-Account Deficits

Current-Account Deficits

(Bloomberg) -- If a family spends more than it earns, it can make up the difference by borrowing, at least for a while. The same goes for a country that sends more money outside its borders to pay for imports than it brings in from the sale of exports. That’s called running a current-account deficit, and the money borrowed usually comes from foreign investors. Running such a deficit for a long time can leave a country exposed to sudden shifts and swings in global capital flows. That vulnerability helps explain why interest-rate decisions in Washington wreaked havoc last year on economies in such places as Indonesia and Turkey, or why booms in deficit-running countries can turn so quickly into busts, as happened in much of Asia 20 years ago.

The Situation

From Argentina to Turkey, a slew of developing countries have run into trouble in recent times by relying on fickle outsiders to plug their deficits. Foreign investors can get cold feet for a variety of reasons, some specific (like a deteriorating economy or a change in government), others more general (such as a global stock market selloff). In 2018, a rout in emerging markets was triggered by the prospect of interest-rate hikes by the U.S. Federal Reserve. Investors quickly switched to higher-yielding U.S. assets, raising worries that persistent current-account gaps would prove untenable for many developing countries. That caused currencies to plunge in places such as Indonesia, which increased interest rates six times in 2018 in an effort to support its rupiah, and India, which raised tariffs on communications gear, jewelry and jet fuel in an attempt to damp imports. In Turkey, the deficit exploded as imports fed a debt-fueled building boom, helping to send the Turkish lira to new lows. Current-account deficits played a key role in the 1997 Asian financial crisis, when currency speculators correctly bet that Thailand’s gap of more than 8% of gross domestic product was unsustainable, before turning their attention to other countries in the region.

The Background

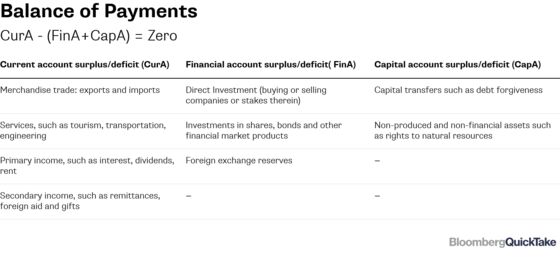

A current account tallies the value of a country’s exports of goods and services against its imports (also known as the trade balance), then throws in a few other measures such as the interest it pays on debt. If the result is less than zero the country has a current-account deficit; if it’s positive it’s known as a surplus. The current account is one element of a nation’s balance of payments, the broadest measure of its transactions with the rest of the world. Since the tally must essentially balance out, any shortfall represents the share that’s financed, generally through either private or government debt sold overseas (think the U.S. and its bumper sales of Treasury notes). For a country with a surplus, the excess is distributed (think China and its vast foreign exchange reserves). A current-account deficit is not to be confused with a budget deficit, which measures the excess of government spending over tax revenue collected — though government borrowing from foreigners helps balance both out.

The Argument

Not all current-account deficits are bad. A country may go into the red in order to fund imports that fuel valuable investment, such as building roads and railways that improve the economy’s growth potential. The Philippines, for example, is betting that its “Build, Build, Build” program that’s turned its current account from a surplus into a deficit will develop the country longer term. The U.S., meantime, has run a current-account deficit for several decades thanks to the ubiquity of — and demand for — the dollar, which is used for everything from pricing commodities to global holdings of foreign-exchange reserves. One problem with persistent deficits is that foreign investors can end up owning a big share of assets, making a country’s stock and bond markets vulnerable to the whims of outsiders. Foreigners own almost 40% of Indonesia’s local currency government bonds, so when overseas holders headed for the exit in 2018, bond yields surged and the currency slumped to its lowest level against the dollar since the Asian financial crisis. Running a surplus is not necessarily a sign of a healthy economy; Spain moved into a surplus in 2012 as demand collapsed and the economy sank into recession.

The Reference Shelf

- A guide to how current account issues are playing out in emerging markets.

- The International Monetary Fund’s manual on balance of payments.

- A QuickTake piece explaining why the crises in Argentina and Turkey hurt Indonesia.

- Quicktake: China’s evolving toolkit to manage monetary policy.

To contact the editor responsible for this QuickTake: Grant Clark at gclark@bloomberg.net

©2019 Bloomberg L.P.