What's a Current Account Deficit and Who's Worried?

What's a Current Account Deficit and Who's Worried?

(Bloomberg) -- Like households and businesses, countries need to balance the books when they spend more money than they take in. And like households or businesses, that’s not such a worry for countries when others are willing to fund any shortfall with loans or investments. However, trouble can brew if the funding dries up. In the case of national economies, the shortfall is called the current-account deficit -- and running such a deficit over a sustained period can come back to bite, particularly in emerging markets.

1. What is the current account?

It tallies the value of a country’s exports of goods and services against its imports of goods and services. That’s also known as the trade balance. The current account, however, is broader than the trade balance, since it also takes into account certain revenue and payments such as interest on debt or dividends on equities. If the value of a country’s imports exceeds that of its exports, a country has a current-account deficit. If the value of its exports exceeds that of its imports, the country runs a current-account surplus.

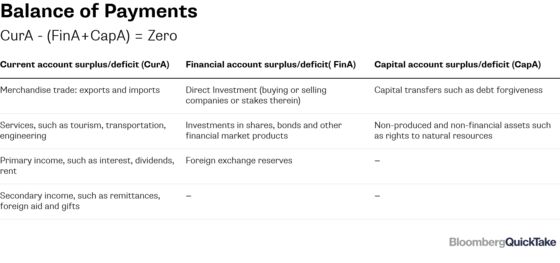

2. Where does it fit into a country’s finances?

It’s one element of the balance of payments, the broadest measure of a nation’s transactions with the rest of the world. The other elements are the capital account and the financial account, which include the net flow of private and public investments and items such as foreign exchange reserves. By definition, the balance of payments, or BOP, has to balance, so for a nation with a current-account deficit, the BOP shows how the shortfall is financed (think the U.S. and its bumper sales of Treasuries). For a country with a surplus, the BOP shows where the excess is distributed (think China and its vast foreign exchange reserves).

3. What’s the problem?

For countries to continue attracting funds to cover long-term deficits, the greater risk to investors eventually needs to be reflected -- in higher yields on bonds, a weaker currency or cheaper stocks. Also, the more a country relies on others to fund its deficit, whether through investing in its markets or offering loans, the more susceptible it is to their whims. Economies where foreigners hold a higher proportion of domestic assets -- including in many emerging markets -- are particularly vulnerable to gyrations in sentiment, such as during the financial crisis or last year’s market meltdown. To make matters worse, any financial selloff exacerbates the deficit, putting pressure on the local currency as investors sell, sell, sell -- threatening an all-out crisis.

4. Any examples?

In Indonesia, overseas investors own almost 40 percent of government bonds. When foreign holders headed for the exits in 2018, bond yields surged (making it more expensive for Indonesia to sell new bonds) and the currency slumped to its lowest level against the dollar since the 1998 Asian financial crisis (making imports more expensive, so worsening the deficit). In the Philippines, President Rodrigo Duterte’s “Build, Build, Build” program turned a current-account surplus into a deficit, since the country needed to import expensive capital goods such as power generators and specialized machines. As the shortfall widened, the currency weakened to a 13-year low.

5. What happens when the funding gets tighter?

Economic growth can be among the first casualties. In India, the government slapped higher tariffs on imports including jet fuel, jewelry and communications gear. In Indonesia, the central bank raised borrowing costs six times in a bid to slow capital outflows, even though inflation was subdued. Another textbook case is Turkey, where President Recep Tayyip Erdogan’s opposition to higher interest rates last year discouraged the central bank from tightening policy fast enough to stem capital outflows and rein in inflation. As a result, the currency plunged to a record low.

6. Why have emerging markets been spooking investors?

Part of the appeal of emerging markets is their relatively higher yields compared with developed markets. When that differential falls because of the U.S. Federal Reserve raising borrowing costs, as it started to do in earnest in late 2016, emerging markets become less attractive. Higher U.S. rates have sucked capital away and strengthened the U.S. dollar, making it more expensive for deficit countries to buy foreign goods and service overseas loans. The Fed’s more dovish tone in early 2019 has helped ease concerns about emerging markets -- for now.

7. Is a current account deficit always a bad thing?

Much depends on the content of the deficit. For instance, it might be funding imports that are used for sound investments, such as roads and rail that will help to improve the economy’s growth potential. The Philippines is betting that its investment program will boost the economy longer term, even though markets reacted by selling the peso. The other notable exception is the U.S., whose currency is used for everything from pricing commodities and settlements of international trades to overseas borrowing and foreign-exchange reserves. The dollar’s prevalence means investors have been happy to look past the U.S. deficit not just on its current account but also its budget.

The Reference Shelf

To contact the reporter on this story: Masaki Kondo in Singapore at mkondo3@bloomberg.net

To contact the editors responsible for this story: Tan Hwee Ann at hatan@bloomberg.net, Grant Clark

©2019 Bloomberg L.P.