The Volcker Rule

Trump Might Allow Big Banks To Revive Proprietary Trading

(Bloomberg) -- When Paul Volcker, the former U.S. Federal Reserve chairman, in 2009 proposed banning many forms of short-term trading by federally insured banks to reduce risk to taxpayers and the world economy, he did it in one paragraph. Four years later, regulators issued a final rule, based on Volcker’s proposal, that limited banks’ ability to buy and sell stocks, bonds, currencies and risky derivative instruments for their own accounts. It ran close to 100 pages, with hundreds more in supporting material — and no one was quite sure how it would be enforced. By the time the rule finally took effect in 2015, it had become a lesson in how complicated simplifying Wall Street can be. Four years later a friendlier administration proposed changes that were somewhat more to the liking of the banks. But the act’s overall continuity underscored to what extent Wall Street had learned to live with a rule it once dreaded.

The Situation

Under orders from President Donald Trump to ease banking regulations that grew out of the 2008 financial crisis, the Fed and four other regulatory agencies finalized Volcker Rule revisions in August 2019. They wouldn’t simplify the rule so much as clarify where the lines between permitted and banned activities would be drawn. The changes were more marginal than major, raising questions about what impact they might have on trading. Trading by banks for their own profit — what’s known as proprietary or prop trading — would remain prohibited, and lenders would still face restrictions on investing in private equity and hedge funds. But the proposal would make it easier to trade for purposes of what’s known as market-making — the steady stream of securities that banks buy, sell and hold as middlemen. In one of the biggest changes, banks will no longer be assumed to be engaging in banned trades when they conduct short-term transactions. The so-called rebuttable presumption was part of what Wall Street hated most about the original rule.

The Background

After the Great Depression, Congress created federal deposit insurance to prevent runs at commercial banks. In return, the banks had to concentrate on making loans while leaving the fancy stuff to investment banks. That dividing line blurred in the 1990s and was erased entirely in 1999 when Congress repealed the Glass-Steagall Act, the law separating commercial from investment banking. Citigroup and other major banks promptly grew big trading operations. The financial crisis of 2008 had its seeds in bad mortgages, but what brought banks to the brink, Volcker noted when he proposed his idea, wasn’t bad loans but the exotic trades they had made around them. Then-President Barack Obama adopted a variation of the idea after taxpayer-paid bank bailouts, wrapping it in Volcker’s name in the hope that the towering stature of the man who tamed 1970s inflation would lend it greater weight. The idea became law in the Dodd-Frank reforms of 2010, but the rule-writing took another three years due to squabbles over how to separate prop trading from market-making and hedging. Instead of blanket bans, regulators sought to define each situation and carve out a string of exemptions, which is how the rule grew and grew.

{kind=link}

The Argument

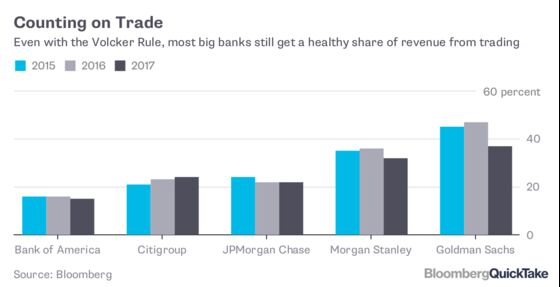

While trading revenue at U.S. banks declined sharply after the global financial crisis, it has since recovered, disproving the doomsayers who argued the Volcker Rule would cripple banks’ ability to trade. There were parts of it the banks disliked intensely: When the final version called on traders to certify the intent of each transaction, Jamie Dimon, the chief executive officer of JPMorgan Chase, complained that traders would need a psychologist and a lawyer by their side to make sure they were in compliance. Fed researchers found that the rule resulted in less-liquid markets for some bonds in times of stress. But by and large, banks adapted to it, though that didn’t stop them from lobbying for years to win procedural changes. Regulators picked by Trump arrived at their agencies with a strong interest in simplifying the rule. The revamp, known as Volcker 2.0, is part of a steady effort to soften regulations during his administration. While watchdogs haven’t ripped up the post-crisis rule book, critics argue that taken together, the changes will insert renewed risk into the financial system.

The Reference Shelf

- A QuickTake explainer on what Trump might mean for Wall Street reform.

- Davis Polk’s Volcker Rule website has the final rule text and statements from the various agencies.

- Deutsche Bank was the first lender to be charged with violating one aspect of the rule in 2017.

- A summary of the 2010 Dodd-Frank Act.

- Volcker’s 2012 comment letter on the original proposal.

- A Congressional Research Service report gives the legislative history of Volcker Rule proposals.

To contact the editor responsible for this QuickTake: John O'Neil at joneil18@bloomberg.net

©2019 Bloomberg L.P.