No More Bailouts? China's New Approach to Bank Stress

No More Bailouts? China's New Approach to Bank Stress

(Bloomberg) -- China’s legions of regional banks are feeling the strain. The country’s two-year crackdown on risky financing and the trade war with the U.S. have slowed economic growth, triggering debt defaults that are exposing them as the weakest link in the credit chain. Several lenders have fallen into deep trouble this year, with others -- perhaps many -- expected to follow. What’s different is that China seems to have thrown out the old playbook of injecting state funds into struggling lenders to keep them alive. If that proves to be the case, it would represent another shift for the country toward more market-oriented practices.

1. So banks are being allowed to fail?

Not quite. They’re being rescued but investors are having to bear some of the brunt. It started in May with the surprise government takeover of Baoshang Bank Co. -- China’s first bank seizure in more than 20 years. The Inner Mongolia-based lender, once seen as a model for funding regional economies, was one of the myriad smaller banks whose shadow-financing techniques obscured their exposure to risky borrowers. The authorities cited “serious credit risks.” Two months later came another approach: the purchase of stakes in struggling Bank of Jinzhou Co. by three state-owned heavyweight firms. Shandong province’s government will become the largest shareholder in troubled Hengfeng Bank Co., local media reported in August.

2. Why is this a big deal?

The new approaches signal a desire to reduce moral hazard -- the perception that there’s an implicit government guarantee behind banks. That’s manifested in other ways in recent years, such as the authorities warning that hugely popular and risky investment products do not have government backing if they fail. Also notable is that smaller banks contribute disproportionately to China’s output and employment, accepting deposits from individuals scattered across the various provinces and funneling loans to small businesses that form the lifeblood of the $13 trillion economy. As such, analysts see trouble ahead.

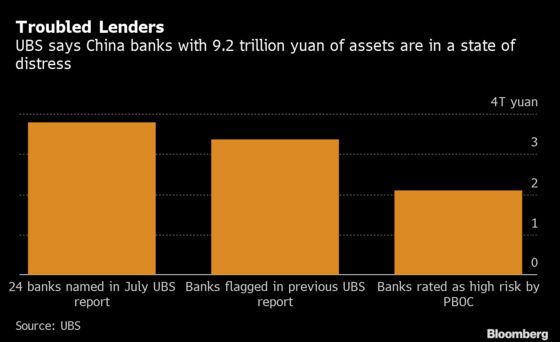

3. How much trouble?

China’s central bank, concluding its first review into industry risks, said in November that about one in 10 of the nation’s 4,000 banks received a “fail” rating. Four hundred and twenty firms, all rural financial institutions, were deemed “extremely risky” and just two received a top rating. Jason Bedford, a UBS Group AG analyst who had flagged the problems at Baoshang and Jinzhou, says China’s smaller banks face a potential capital shortfall of 2.4 trillion yuan ($340 billion). He estimates the size of assets “in distress” held by a broader universe of Chinese lenders at 9.2 trillion yuan -- about 4% of the commercial banking system and nearly 10% of gross domestic product.

4. What’s been the reaction?

Security prices quickly reflected the greater risk as policy makers upended the long-held assumption they would provide banks with a 100% backstop. In July, a key measure of the market’s wariness toward smaller Chinese banks (the yield gap between low- and top-rated non-convertible debentures) surged to as much as six times wider than before the Baoshang takeover. A Bloomberg Intelligence index of Hong Kong-listed Chinese bank stocks slumped more than 15% between early May and early August.

5. Who’s next?

Baoshang and Jinzhou are unlikely to be the last of China’s bank rescues and larger lenders will continue to be brought in to tackle problems at their smaller counterparts, say analysts including Katherine Lei at JPMorgan Chase & Co. Bankruptcies, though, are unlikely given market sensitivities, Lei said, even though a deposit insurance program was put in place in 2015. Research firm Trivium China sees the Baoshang case as a “pivotal” moment in accelerating banking consolidation.

6. How might this affect the economy?

Regulators want to prod smaller banks into improving management and serving the real economy, according to Citic Securities Co. China’s aggressive smaller, regional banks amassed a quarter of total banking assets by end-2018, with lending growth -- fueled by interbank borrowing and shadow financing -- twice as fast as at bigger rivals. The shadow financing crackdown could force them to cut leverage and return to their original business model: taking deposits and lending to small businesses. UBS’s Bedford says that while China’s financial industry is on a sounder footing than it was a few years ago thanks to the cleanup by regulators, he sees a difficult road ahead as authorities grapple with how to fix the country’s problem banks without spooking markets.

The Reference Shelf

- UBS analyzes the risks facing China’s smaller lenders.

- China’s $40 trillion banking system learns a lesson.

- QuickTakes on China’s shadow-banking maze and rising debt defaults.

To contact Bloomberg News staff for this story: Jun Luo in Shanghai at jluo6@bloomberg.net;Lucille Liu in Beijing at xliu621@bloomberg.net

To contact the editors responsible for this story: Sam Mamudi at smamudi@bloomberg.net, Jeanette Rodrigues, Grant Clark

©2019 Bloomberg L.P.

With assistance from Bloomberg