The End of Libor Is a $12 Trillion Headache for Loan Bankers

The End of Libor Is a $12 Trillion Headache for Loan Bankers

(Bloomberg) -- The whole financial world is working to move away from Libor and other interbank lending benchmarks, which for decades have been used to set borrowing costs on bonds and loans, as well as products ranging from derivatives to credit cards. Since 2018, more than $150 billion worth of bonds have been sold using rates set by a new generation of benchmarks. The syndicated loan market is lagging far behind, with at least $12 trillion of deals needing to be replaced or rewritten so they follow a Libor alternative. There are no easy fixes in sight despite potential deadlines as early as this year.

1. What’s Libor and why is it disappearing?

Libor, or the London interbank offered rate, is a daily average of what banks say they would have to pay to borrow from one another. It forms the basis for floating-rate or variable loans and bonds. But ever since European and U.S. banks were found to have manipulated rates to benefit their own portfolios, the benchmark has been seen as tainted. Along with its interbank offered rate (Ibor) kinfolk -- such as Euribor for the euro and Tibor for the yen -- Libor is headed for history’s scrapheap, set to be abolished by the end of 2021. A Bank of England working group has proposed halting new lending using Libor in the third quarter of this year.

2. What’s taking its place?

Central banks around the world have been working to develop a replacement set of benchmarks based on what are called risk-free rates (RFRs). The goal is to find a rate that reflects the general state of the credit market, and is based on actual transactions -- unlike Libor, which became open to manipulation as it went from being a synthesis of actual loans to a compilation of banks’ guesses about what such borrowing would cost. New entries include the U.S.’s Secured Overnight Financing Rate (SOFR), the U.K.’s Sterling Overnight Index Average (Sonia), and the Euro Short-Term Rate (ESTR).

3. Why is the change a problem?

Ibor comes in many flavors in terms of duration, like monthly or quarterly, and crucially for the loan market it includes forward-looking rates, that is, rates that incorporate market expectations for the cost of borrowing over a particular duration. By contrast, the new benchmarks mostly track backward-looking overnight lending: SOFR, for instance, is based on the U.S. repo market, where cash is briefly exchanged for high-quality securities. Rewriting loans so they track an overnight benchmark instead of a three-month rate would be hugely complicated not least because the changeover would probably require pricing renegotiations.

4. Why not just create new three-month rates?

This is a lot easier said than done. Calculating a three-month rate out of a string of overnight transactions is very complicated, and the loan market has yet to develop a commonly accepted methodology or answer basic questions such as whether to include weekends. The lack of official compounded rates also means loan agents would need to calculate rates manually, resulting in less transparency for borrowers. Furthermore, any rate compiled by compounding or averaging daily figures for the new benchmarks would be backward-looking, breaking with loan traditions. One possible way to compile a forward-looking rate would be to turn to the swaps or futures markets, where traders speculate on risk-free rates a little down the road. Still, it could take a long time to develop a new rate this way, and regulators have told banks not to wait around for it to happen.

5. Why is this a bigger problem for syndicated loans?

The bond market has started on the Libor transition helped by the fact that every deal is always in just one currency and the borrowed funds are always fully disbursed at the start of the lending period. Loans are more complicated because borrowers can dip in and out of deals -- regularly changing the amount being used. The syndicated loans market also sees at least 300 multi-currency deals every year. This hasn’t been much of a problem with Libor and its different-currency cousins because they all use the same general methodology. The new single-currency benchmarks may be less similar because they are being separately developed by central banks. This will add even more complication, potentially resulting in pricing errors.

6. Why does this matter?

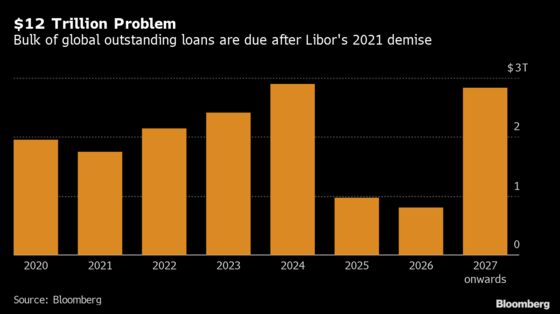

Companies worldwide, especially listed and top-rated conglomerates, take out $4 trillion-plus of loans each year for cashflow, capital expenditure, investments and acquisitions. Many loans are routinely rolled over from one year to the next, and companies’ financial health could be put severely at risk if the loan market seized up as a result of Libor’s demise. There is also $12 trillion of long-term loans that will need to be converted to a new benchmark because they mature after 2021. More than half of them are based on Libor and the rest are tied to other Ibor rates, so the market faces the Herculean task of amending or renewing all this outstanding debt. Without standardization, companies from the same sector and ratings bracket could end up paying different pricing, which would disrupt the transparency and efficiency of the market.

7. What’s being done about this?

Global loans bodies like Europe’s Loan Market Association (LMA) are proposing changes to loan documentation to make it easier to transition existing loans to RFRs. The LMA has also been publishing so-called exposure draft versions of guidance on new structures and terms for referencing new benchmark rates directly. The LMA and the Loan Syndications & Trading Association (LSTA) in the U.S. are working with lenders to develop methodologies and calculations. The International Swaps & Derivatives Association (ISDA) announced that Bloomberg LLP, the parent company of Bloomberg News, will provide Ibor fallback calculations -- alternatives to use when Ibor isn’t available -- and publish compounded RFRs. Major banks, specifically those that have arranged non-Ibor based bond sales, have set up operational systems to tackle existing portfolios and potential spread adjustments and calculations. Loan system vendors such as FIS (ACBS) and Finastra are developing systems using compounded rates.

8. Have any loans been made in the new system?

The syndicated loan market only saw its first deal using SOFR in December 2019. Royal Dutch Shell Plc signed a $10 billion revolving credit facility, which will initially follow Libor before switching to SOFR once the market is ready. Documentation is based on the LMA’s exposure draft for SOFR. The loan spread may need to be adjusted after the switch as there will be a gap between Libor and SOFR rates. Elsewhere, the limited number of Sonia loans have all been bilateral deals rather than more complicated multi-bank syndications.

The Reference Shelf

- A QuickTake exploring issues in adopting Saron for Swiss Franc.

- A QuickTake overview on SOFR, and an explainer on how the U.S. came up with SOFR to replace Libor.

- A Bloomberg News article on the European loan market’s need for a Libor replacement.

- Bank of England working group’s consultation paper on credit adjustment methodologies.

- An update on loan-market transition to risk-free rates by law firm Clifford Chance.

- Europe’s Loan Market Association paper on how to transition from Libor.

- U.K. Financial Conduct Authority speech on preparing for end of Libor.

To contact the reporters on this story: Jacqueline Poh in London at jpoh39@bloomberg.net;Ruth McGavin in London at rmcgavin1@bloomberg.net

To contact the editors responsible for this story: Hannah Benjamin at hbenjamin1@bloomberg.net, John O'Neil, Neil Denslow

©2020 Bloomberg L.P.