How Leveraged Loans Are (and Aren't) Like Junk Bonds

How Leveraged Loans Are (and Aren't) Like Junk Bonds

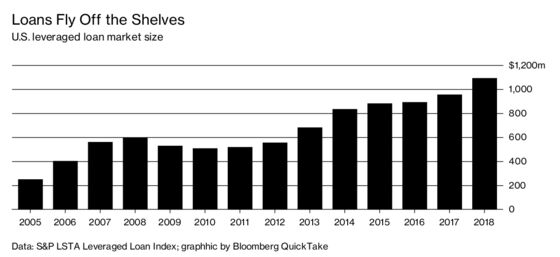

(Bloomberg) -- The leveraged loan market has doubled in size since 2012. Plenty of investors think they know why: Loans are just like safer versions of high-yield junk bonds and likely return more as interest rates rise. It’s true that leveraged loans and junk bonds share similarities. Both were pioneered by Michael Milken in the 1970s. Both finance corporations with less-than-stellar investment ratings. Both are traded over the counter, and the total market for each is about $1 trillion in the U.S. But peer more closely and you’ll find stark differences. A bond is a security with features that allow it to trade and settle more easily. A loan is a contract between a lender and a borrower; each one is different. Rookie investors may learn the details only after suffering nasty losses.

1. What makes a loan leveraged?

It’s made to a company deemed to be risky because it has a lot of debt compared to its income and cash flow. The risk is determined by ratings agencies -- a Moody’s Corp. credit rating of Ba1 or lower or Standard & Poor’s rating of BB+ or lower. In exchange for making these dicey loans, which are secured by physical assets, investors earn a defined amount of interest -- the so-called margin -- on top of the prevailing Libor benchmark rate. This increases as the loan gets riskier. If the company tumbles into bankruptcy and is restructured or liquidated, leveraged loans are usually supposed to be paid off before junk bonds. Traditionally, banks were the main lenders, but now most of these loans are sold to investors.

2. What’s a junk bond?

A high-yield bond made to the same risky companies. These bonds, nicknamed “junk,” became widely used in the 1980s thanks to Drexel Burnham Lambert and transformed the financial landscape. They fueled debt-financed buyouts of U.S. corporations such as the landmark $26 billion hostile takeover of RJR Nabisco in 1989 and fanned the growth of a private equity industry that grew into firms like Blackstone Group LP, Carlyle Group, and Kohlberg Kravis Roberts (now KKR & Co, Inc.).

3. Why are investors confusing the two?

Leveraged loans have started to look more like junk bonds, as their restrictions have eased and a trading market has developed. Leveraged loans were once normally protected by contract clauses called maintenance covenants that allowed lenders to monitor the borrowing company’s performance and take action, like forcing the sale of assets, if earnings deteriorated. During the financial crisis of the last decade, many companies with leveraged loans saw earnings plummet. Some were able to make the case to investors that this wasn’t their fault and they needed these covenants eliminated. Investors agreed. These loans with looser rules, known as covenant-lite, gradually spread and now represent 80 percent of new issuance. They’ve become so common that many investors shy away from making loans with strict covenants, figuring that if a borrower needs to agree to that many restrictions, the loan could be dicey. Since high-yield bonds don’t have maintenance covenants that give investors oversight over performance, investors and borrowers began to view covenant-lite loans similarly.

4. How do loans and junk bonds differ?

Junk bonds are securities traded under the authority of the U.S. Securities and Exchange Commission. They follow federal mandates, such as trades having to close within three business days. Leveraged loans are not regulated by the SEC, since they are transactions between borrowers and lenders. So getting cash from a loan trade can take weeks and as long as two months. Leveraged loans are usually less volatile than high-yield bonds because the majority of loans are bundled into collateralized loan obligations, or CLOs, which pay regular returns while spreading the risk of default among many investors. This provides steady support for loan prices. In turn, high-yield bonds are typically seen as having more liquidity, the ease of selling and buying an asset, though the bigger-sized loans are becoming just as easy to trade.

5. What’s happening now?

The leveraged loan market is growing while the junk bond market is shrinking. Borrowers, especially private equity shops, now prefer covenant-lite leveraged loans to finance deals since they’re not burdened with a lot of lender oversight, can be paid down at will, and are cheaper than junk bonds. The leveraged loan market has been able to keep up, mostly through CLOs sold to institutional investors. With fewer junk bonds being created, their buyers are being pressured to accept ever-riskier terms at slighter spreads.

6. What could go wrong?

After years of low interest rates, there has been a big increase in the issuance of bonds and loans by risky U.S. companies, at ever-more-favorable terms for the borrowers. As portfolios have ballooned and investment options dwindled, complacency about default risk has spread. Now that interest rates are rising, already shaky companies with big debt loads will find it harder to make payments; some will stop altogether. Because leveraged loans have evolved dramatically since the last recession, it’s unclear how much investors will recover on distressed loans or how much liquidity there will be if loan prices decline across the board. Leveraged loan investors looking to sell at signs of trouble might have to watch prices fall substantially before they could complete their transactions. The long delay in settling a trade could be especially problematic for mutual funds holding these loans, since they promise to pay their clients immediately. Liquidity problems are why the Bank of International Settlements and other watchdogs have sounded alarm bells over leveraged loans.

The Reference Shelf

- Bloomberg’s look at ways to avoid the next financial crisis asks whether CLOs are the new CDOs.

- Bloomberg’s history of the rise and fall of Michael Milken’s junk-bond empire.

- Danger signs are flashing over leveraged loans.

- A QuickTake explainer on leveraged loans.

To contact the reporter on this story: Lisa Lee in New York at llee299@bloomberg.net

To contact the editors responsible for this story: James Crombie at jcrombie8@bloomberg.net, Anne Cronin

©2018 Bloomberg L.P.