How Fed Could Goose Economy via Yield-Curve Control

How Fed Could Goose Economy via Yield-Curve Control

(Bloomberg) -- Central banks set short-term rates and markets set the rest, right? That’s just the way thing work -- except in dire need, like when facing a pandemic’s massive economic disruption. The U.S. Federal Reserve is just the latest central bank to give serious consideration to a policy called yield-curve control that seeks to hold down longer-term interest rates by capping what the government pays on its debt.

1. What is yield-curve control?

The yield curve (YCC) is the relationship between rates on bonds of varying durations. Investors generally demand a higher yield for holding longer-term debt, meaning that the curve is normally upward sloping. And normally, central banks manage monetary policy through short-term rates only: The Fed, for instances, creates incentives to keep overnight borrowing within a range it specifies -- what’s known as the Fed Funds rate. In a policy of yield-curve control, the central bank also sets a target yield for one or more specific maturities of government debt.

2. How does it do that, and what does that do?

A central bank pursuing yield-curve control will announce its target rates and maturities -- and that it will buy those securities in whatever amounts are necessary to peg the rate there. As well as capping longer-term borrowing costs for the government, this will bring down rates for businesses and consumers. The policy also helps convey the message that benchmark short-term rates will be staying low, according to some Fed officials.

3. Is anybody already doing this?

Yes. The Bank of Japan has been pursuing yield-curve control since 2016 as part of its fight against deflation, after years of negative benchmark rates and massive bond purchases failed to achieve inflation targets. Japan chose to pin 10-year rates at zero -- which ensures a degree of upward slope in the yield curve, since its overnight policy rate is negative. Australia adopted a different version of the idea in March, in response to the coronavirus. The Reserve Bank of Australia is targeting three-year bond yields at 0.25% as part of its quantitative-easing program. India’s central bank, while it hasn’t publicly said so, is reckoned by many analysts to have been using a form of yield-curve control since February.

4. What about the Fed?

Federal Reserve Bank of New York President John Williams says policy makers are “thinking very hard” about targeting specific yields on Treasury securities, because it’s another way -- on top of keeping the benchmark interest rate near zero -- to ensure that borrowing costs stay at rock-bottom levels. Such a maneuver could “potentially complement” other policy actions,” Williams said in an interview on Bloomberg Television. For now, only a few Fed board members, including Lael Brainard, support yield caps. But “it’s not a stretch to think that more supporters would come on board once the idea is fully thrashed out,” said Roberto Perli, a partner at Cornerstone Macro LLC and a former Federal Reserve economist, wrote in a note.

5. What might a Fed version look like?

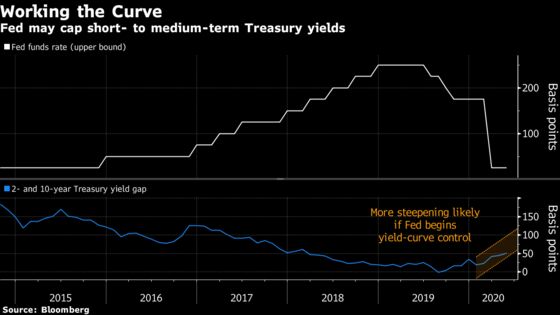

Wall Street investors predict that the Fed would most likely follow the Australian example, selecting Treasury debt with maturities of somewhere between two and five years as its target. That view aligns with the support expressed by at least a few Fed officials for caps on “short- to medium-term maturities,” according to minutes from their April meeting. It would be a departure from the only other time the Fed used the strategy, during World War II, when it capped yields on 30-year bonds as well as Treasury bills.

6. What would it mean for debt markets?

The likely effect would be to expand the gap between 5- and 30-year Treasury yields, that is, to “suppress real rates and lift inflation expectations,” according to Mark Cabana, head of U.S. rates strategy at Bank of America Corp. He predicts that the Fed may adopt yield-curve control as early as September, opting to cap yields on 2- or 3-year Treasuries at around 0.25% (currently the top of the target range for the central bank’s overnight policy rate).

7. What are the dangers?

If the Fed helps the federal government battle the coronavirus by holding interest rates down, it could find its ability to raise rates after the crisis constrained by the huge budgetary impact of even a small increase in borrowing costs. Still, that could be true regardless of whether the Fed adopts yield-curve control -- and in any case that question won’t arise until there’s a pickup in inflation, which most economists don’t see as an imminent threat.

The Reference Shelf

- Fed Governor Lael Brainard discusses yield-curve control in a Feb. 21 speech in Chicago and Nov. 26 speech in New York.

- Fed Chairman Jerome Powell discussing YCC in Denver in October.

- Bloomberg News stories on YCC and the Fed-Treasury alliance to fight Covid-19.

- NY Fed’s Kenneth Garbade reports on 1940s yield-curve management.

©2020 Bloomberg L.P.