How ECB Hopes ‘Tiering’ Eases Pain of Negative Rates

How ECB Hopes ‘Tiering’ Eases Pain of Negative Rates

(Bloomberg) -- In September, the European Central Bank has doubled down on its negative interest rates, a policy meant to stimulate the economy by charging banks billions of euros for money they’re not lending out. At the same time, it added a new measure, called tiering, to ease the impact on banks that have been complaining about paying those billions. Tiering might help more of the ECB’s monetary stimulus reach the real economy. Or it could blunt the effort while helping some banks more than others. For the world’s only central bank managing a multicountry currency area, nothing is simple, especially very complicated things.

1. What is tiering?

It’s a system that applies negative rates differently to different chunks of the money banks have parked with their central bank. The ECB’s system went into effect Oct. 30. That means that reserves as much as six times the minimum amount a bank there is required to hold will be exempt -- the interest rate on that money will be 0%. Any reserves beyond that mark will be subject to the ECB’s new deposit rate of minus 0.5%, a further drop from 0.4%.

2. Why is the ECB doing this now?

Signs of economic weakness both globally and across Europe have led the ECB to institute new stimulus measures, including the lowering of the negative rate. But that’s raised worries about whether the policy might undermine itself. Negative rates were already costing European banks about 7.5 billion euros ($8.25 billion) annually, an amount they called a drain on their profits that could eventually hurt their ability to lend. The ECB’s chief economist, Philip Lane, described tiering as a way to strike the right balance.

3. How much will tiering help banks?

Third quarter earnings results showed that Europe’s banks continued to feel the pain from negative rates -- some were even considering ways of passing the penalties on to clients. The ECB estimates tiering will allow the region’s lenders to save around 4 billion euros a year. Those savings aren’t likely to fall evenly, however.

4. Who’s going to benefit most?

The region’s bigger lenders -- particularly those from Germany, France and the Netherlands -- account for some 40% of all the euro area bank reserves that exceed minimum requirements. That means they’ll see the biggest savings. Deutsche Bank -- Germany’s biggest lender -- estimates it’ll save more than 100 million euros in annual interest payments. That’s not likely to make banks with lower reserves, including many in Italy and other southern European nations, happy. But it could give the richer northern banks a stronger reason to make cross-border loans to their weaker counterparts within the euro region, something the ECB has been trying to encourage since the debt crisis, with only limited success.

5. What else might tiering do?

Some analysts worried that adding tiering could undo some of stimulus sought from negative rates -- that it could push the rates in actual interbank lending above the level the ECB is targeting. That’s in part simply because the negative rate will apply more narrowly once some reserves are exempted. Another worry is that banks who currently have fewer reserves than the maximum amount exempted will have an incentive to borrow to get the full benefit of tiering -- an additional demand for borrowing that could drive rates up. However, there’s no evidence of that so far, and the ECB has pledged to monitor markets closely and make changes as needed. And at least on the first day of tiering, there was no sign that interbank rates were being driven up.

6. What would the ECB do if rates go up?

It says it would shrink the level of reserves eligible for exemption from negative rates if the short-term rate is “unduly influenced.” It would do that by lowering the current dividing line between tiers -- the multiplier of six times mandated reserves. The ECB has also restarted its bond purchasing program, known as quantitative easing, in November. The bank plans to buy 20 billion euros of bonds a month for the foreseeable future, money it deposits with euro area banks, thereby driving up their reserves and holding rates down.

7. How does tiering mesh with other ECB measures?

It’s not the ECB’s only program meant to give banks relief. The central bank recently renewed its Targeted Longer-Term Refinancing Operations program, or TLTRO, which gives banks cheap loans. Banks that meet targets for lending to the private sector can even borrow at a sub-zero rate. Money from the new round of TLTROs could encourage banks in countries such as Italy to borrow through the program to increase their reserves to take full advantage of the tiering exemption quota.

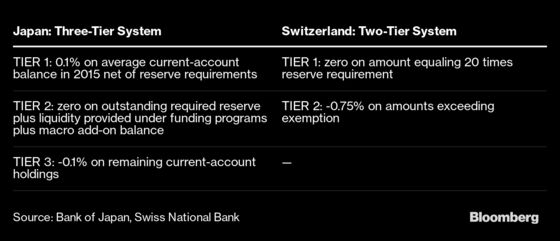

8. Has tiering been done anywhere else?

Yes. Both Switzerland and Japan introduced tiering systems when they began their own negative rates policy, and the ECB’s tiering borrows heavily from the Swiss model. Here’s what the model looks like in those two countries:

The system is also used in Denmark and Sweden. But it’s never been tested before in a multicountry currency zone, where the conditions of banks can vary widely in different parts of the region.

The Reference Shelf

- The ECB’s release on the two-tier system.

- ECB Vice President Luis de Guindos delivered a speech on the benefits and design of the two-tier system.

- A Bloomberg story on tiering giving banks relief.

- A Bloomberg feature on the range of options the ECB has on making their sub-zero rates policy more palatable.

To contact the reporters on this story: Yuko Takeo in Tokyo at ytakeo2@bloomberg.net;Piotr Skolimowski in Frankfurt at pskolimowski@bloomberg.net

To contact the editors responsible for this story: Paul Gordon at pgordon6@bloomberg.net, David Goodman, Zoe Schneeweiss

©2019 Bloomberg L.P.