How the Fed’s Swap Lines Aim at Dollar Funding Stress

How Currency Derivatives Show Dollar Funding Stress

(Bloomberg) -- A global run on the U.S. dollar triggered by the coronavirus pandemic is once again prompting the Federal Reserve to step in as the lender of last resort for investors and companies scrambling for dollars. The Fed enhanced the existing dollar-liquidity swaps it offers foreign central banks and established new ones as part of sweeping emergency measures unleashed to ease a shortage of greenbacks. The idea is to help companies seeking to either raise cash or repay loans and alleviate pressure on currency markets.

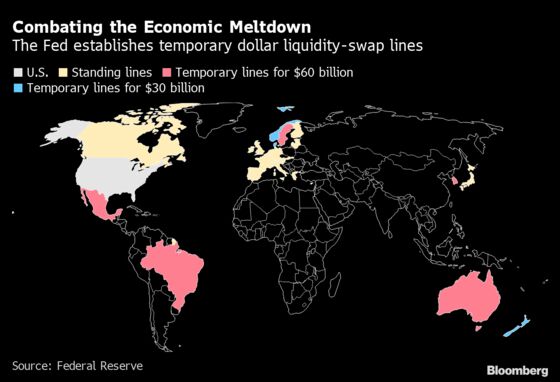

1. What’s a central bank dollar swap line?

First used extensively during the 2007-2008 financial crisis, they’re temporary lending facilities that allow central banks around the world to borrow dollars from the Fed in exchange for an equivalent amount of their local currencies. On March 15, the Fed and five major central banks, including those in the euro zone and Japan, said they’d activate the program to ease a squeeze as demand for the dollar surged. They subsequently increased the frequency of seven-day maturity operations to daily from weekly. The Fed also lowered the rate and added a longer maturity. Then it expanded the swap line to nine other central banks, including Australia and Brazil, bringing the total to 14. And then at the end of March it allowed foreign central banks to swap any Treasuries securities they hold for cash.

2. What’s the Fed hoping they’ll do?

The goal is to ease the panic for dollars and allow foreign-exchange markets to keep operating normally. Surging volatility in stock and bond markets has spurred a rush to secure the U.S. currency for borrowers and as a haven against further turmoil. Central banks, sovereign wealth funds and U.S- based asset managers who would otherwise invest their greenbacks have pulled their lending, creating a dollar vacuum. The Fed says the lines are necessary at times because bank funding markets are global and can break down “disrupting the provision of credit to households and businesses in the United States and other countries.”

3. Will it work?

That’s the big question. While the measures can ease pressures for banks, the effect is felt in the broader economy only if these lenders extend more dollar loans to companies and other financial institutions. Banks also may shun a central bank swap line because of a stigma attached to tapping it. Making dollars available to foreign nations -- even if it didn’t cost the Fed -- became a point of contention for some lawmakers in the U.S. Congress during the 2008 crisis. The central bank had to repeatedly defend the action, saying U.S. taxpayers were not on the hook because these were swaps -- not loans -- and there was no risk of default. Back to 2020, the early signs were promising as banks in mainland Europe and the U.K. took billions of dollars on offer from their central banks.

4. Where are the signs of dollar shortage?

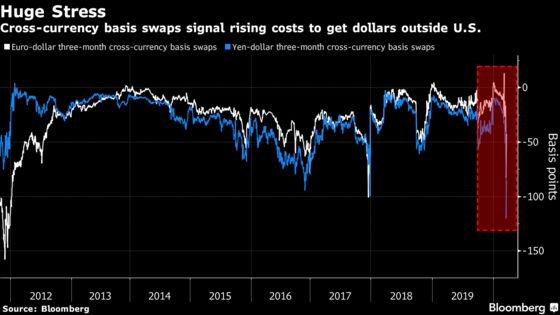

The dollar shortage became acute as the greenback soared on March 18, throwing other currencies from the British pound to the Brazilian real into free fall. As stocks plunged and investors fled to U.S. Treasury bonds amid the global coronavirus pandemic, the currency derivative market showed signs of stress. There was a notable move in cross-currency basis swaps, revealing a preference among investors to hold dollars rather than euros or yen.

5. Why are some Fed swap lines more popular?

Japanese banks have taken more than $150 billion from these funding operations in an attempt to satiate demand and also to hoard dollars ahead of the end of the fiscal year. The foreign claims of Japanese banks have increased substantially since the global financial crisis, while they have declined for their European counterparts, according to the Bank for International Settlements.

6. Is there a fee on some swap lines?

The European Central Bank can charge a fee for accepting collateral in return for lending dollars, which may make the transaction more expensive. Some banks may in turn find it cheaper to access dollars in the open market, even when liquidity conditions are tight, reducing the demand for these operations.

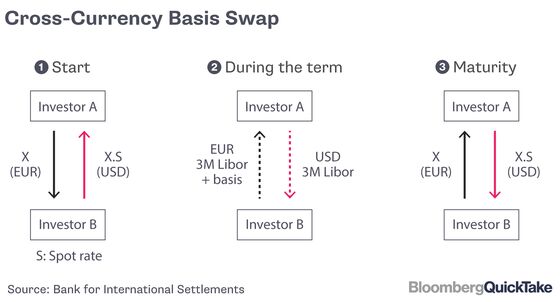

7. What are cross-currency basis swaps?

They’re contracts where two sides agree to exchange interest payments in two different currencies. During the life of the contract, floating interest-rate payments are exchanged, typically on a quarterly basis. On March 17, the premium paid to swap funding exposure from euros into the dollar surged to the widest since 2011. The premium narrowed in the days that followed, though it remained elevated. That suggests investors were still struggling to get their hands on dollars despite injections of cash into financial markets by the Fed.

8. What do they tell us about borrowing stress?

Dollar funding stress is particularly pronounced for yen- and euro-based investors, based on cross-currency basis swaps. While higher demand to swap funding exposure from the yen into the dollar was evident from the start of February -- coinciding with the rally in Treasuries -- the euro-denominated market was more resilient until mid-March. The moves have also come at a time when financial companies become increasingly cautious about lending to each other and demand higher premiums on interest over risk-free rates, known as the FRA/OIS spread.

9. Who uses cross-currency basis swaps?

Banks are the biggest users, while hedge funds and proprietary trading firms rank second. The favored currencies are the dollar, euro and yen. Most contracts involve the dollar. They typically range from 1 to 30 years, reflecting the length of the transactions they fund, such as loans. What makes them unique in the world of swaps is that the parties agree to exchange notional principals, or the face amount used to calculate the payments.

10. Why do investors need them?

Let’s say a European company needs a dollar loan. While the firm may be well-established on the continent, banks in the U.S. may demand a stiffer rate to lend to a relatively little-known entity on the other side of the Atlantic. Enter the cross-currency basis swap. The European firm borrows in euros and swaps the payment into dollars with another entity that needs funds in Europe’s common currency.

11. What happens if the widening in basis swaps continues?

That’s the million-dollar question. If investors continue to seek the safety of Treasuries and stocks keep tumbling, the preference to swap out funding exposure into the dollar may persist. The pressure may be more pronounced in the yen market because it’s historically been a good proxy for institutional funding stress.

The Reference Shelf

- How the U.S. dollar’s surge on March 18 led to staggering moves in foreign exchange markets, leading to calls for intervention.

- The Fed’s website explains the history and use of dollar-liquidity swaps.

- A Bank for International Settlements paper explains the cross-currency basis.

- A Quicktake explainer on the FRA/OIS spread.

- Reserve Bank of Australia Deputy Governor Guy Debelle explains how he came to “love the basis.”

©2020 Bloomberg L.P.