How Climate Divestment Won Converts With Deep Pockets

How Climate Divestment Won Converts With Deep Pockets

(Bloomberg) -- Can you strike a blow against climate change by getting rid of your oil company stocks -- and can you do it without losing money? The idea is not just for activists anymore. Norway took a partial step in selling off oil and gas stocks in its massive $1 trillion wealth fund. And a growing number of investors who control trillions more are using the threat of divestment as a cudgel to force energy companies to adopt greener ways. Together these approaches are producing a notable disruption in the energy field.

1. What’s the climate divestment movement about?

It was started in 2012 by the activist group 350.org, whose name is a reference to what some scientists consider the maximum safe level of atmospheric carbon in parts per million. Its goal is to “keep carbon in the ground,” in part by weakening the oil, gas and coal industries. Adopting a tactic from the fight in the 1970s and 80s to force South Africa to give up apartheid, it urges universities and other investors to divest themselves of stocks from the 100 largest coal companies and the 100 largest oil and gas firms.

2. How has that gone?

The initial movement has had some success. The group says that so far more than 1,100 institutions, from pension funds to family foundations, mostly in North America and Europe, have made some level of commitment to divesting. But the biggest steps have come from investors acting independently. The Norwegian fund decided to dump $6 billion of oil and gas exploration companies’ stocks as a hedge against a long-term decline in crude prices, although it also argued that existing producers are investing heavily in the transition to renewable power. And BNP Paribas Asset Management said it would dump almost 1 billion euros ($1.1 billion) of coal stocks from its actively managed funds.

3. Is this all about coal?

Coal, the dirtiest fossil fuel, has been the primary focus but that’s starting to change. One of Exxon Mobil Corp.’s largest shareholders, Legal & General Investment Management, sold $300 million of the oil giant’s stock when it wasn’t satisfied with the company’s emissions reductions strategy.

4. Have those moves had an impact?

In some ways. The biggest success has been how very large shareholders have been using the idea for their own purposes. A coalition of mega-investors called the Climate Action 100+, which collectively oversees more than $35 trillion, has been engaging with companies they feel are most at risk as the world transitions away from fossil fuels. The group has extracted pledges from some of the biggest companies, including BP Plc, Royal Dutch Shell Plc and coal giant Glencore Plc, to better align their businesses with the goals of the Paris climate accord. Royal Dutch Shell also agreed to publish a report on its lobbying of governments.

5. Is this a split in the movement?

Not really. Though the largest and most powerful money managers tend to use the threat of divestment to push companies to succeed, rather than disappear. For example, after freezing out Rio Tinto Group for more than a decade for owning a highly polluting copper mine, the Norwegian sovereign wealth fund re-invested when Rio sold it. It’s now one of Rio’s top 10 shareholders. One of Climate Action 100+’s largest members, Legal & General Investment Management, with about $1 trillion under management, divested its holdings in some large companies in June, saying they failed to engage over global warming.

| Who’s taking action on climate change? |

|---|

|

6. Is there an economic argument for divesting?

That depends on who you ask. Oil companies themselves see demand for their products peaking, but not until sometime between 2025 and 2050, and then slowly declining. Economics drove the thinking at Norway’s sovereign wealth fund, the world’s biggest, about whether it should dump about $37 billion of fossil-fuel stocks. It ultimately kept most of them, noting that oil and gas companies have become some of the biggest investors in renewables. The Norwegian finance ministry said that diversification may pay off for the fund in the long-term.

7. What are the financial arguments not to divest?

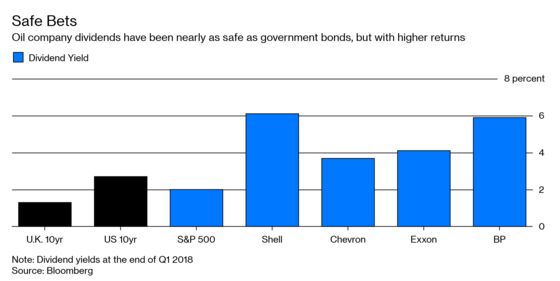

For most investors, having money in an oil company is almost unavoidable. Behemoths such as Exxon Mobil Corp. and Shell are included on every major equity index -- core investments, like it or not, for the mutual funds that almost everyone’s pensions or 401Ks are invested in. Then there are the dividends. Oil companies distribute money to shareholders with a fervor matched by few others. If you bought a share of Shell during World War II, you would have received a flat or increasing dividend payment every quarter without exception. Those dividend payments have endured through price collapses, the Arab oil embargo, wars, nationalization of assets, government sanctions, worries that supplies would run out and more. Few assets besides government bonds offer that kind of stability. And the yield of a Shell share is more than 6%, while a 10-year U.K. gilt will earn you less than 1%.

8. So does divesting mean taking a financial hit?

It’s a question of the time frame. The absolute return of oil companies hasn’t outperformed the broader index since 2014 because of an oversupply of crude that caused prices to slump. Exiting now could mean passing up those fat dividends and possibly rising share prices, but also curbing exposure to the impact of climate legislation and competition from alternative forms of energy.

9. If everyone divested tomorrow, what would happen?

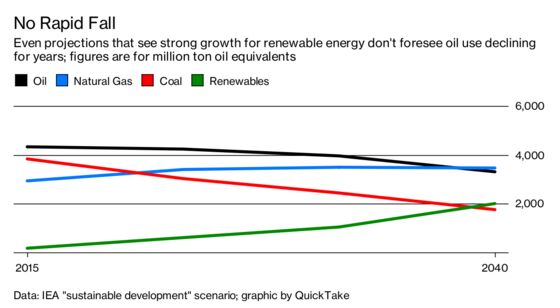

First of all, the sheer size of oil holdings means it would be hard for everyone to sell at once -- the Norwegian selloff will be done over years. Even if could happen, it probably wouldn’t cut demand for fossil fuels sharply right away. Renewable energy sources like wind and solar are growing rapidly but from a tiny base. In one scenario modeled by Shell, meeting goals set in the Paris climate accord without fossil fuels would require new energy sources to increase fifty-fold and the reforesting of an area the size of Brazil, among other measures.

10. What do energy companies think of the movement?

They don’t like it. BP Chief Executive Officer Bob Dudley said in October a rising cost of capital for the industry could harm human development, pointing out that cheap energy is essential to economic growth. Executives have also argued that even with a large proliferation of renewables, fossil fuels will remain essential for a wide range of products such as plastics, pharmaceuticals and road surfacing.

The Reference Shelf

- An explanation from 350.org about the push for divestment.

- Frequently asked questions answered by the Climate Action 100+ group.

- Carbon Tracker, the group that coined the term “stranded assets,” explains the risk of fossil fuel companies pursuing continued growth

- The view from Norges Bank about oil and gas stocks.

- A BNEF study on the competition to oil and gas from renewables.

- A U.S. congressional report on the financial performance of oil companies amid volatility.

- Shell’s Sky Scenario, which gives insight into how it thinks it can stay aligned with Paris Accord.

--With assistance from Mikael Holter.

To contact the reporter on this story: Kelly Gilblom in London at kgilblom@bloomberg.net

To contact the editors responsible for this story: James Herron at jherron9@bloomberg.net, John O'Neil

©2019 Bloomberg L.P.