How an Attack on Saudi Oil Upended a Global Calculus

How an Attack on Saudi Oil Upended a Global Calculus

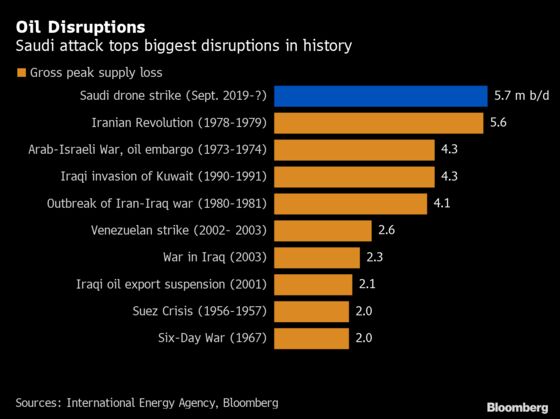

(Bloomberg) -- The Sept. 14 attack on two of Saudi Arabia’s biggest crude oil production plants sent shock waves through energy markets and triggered the biggest one-day jump in Brent crude prices on record. In volume terms, the estimated 5.7 million barrels a day of lost Saudi production was the single biggest sudden disruption on record. It underscored how the oil industry, perpetually on edge for political uncertainty and hints of weakness in the global economy, can be badly shaken by a single localized event.

1. Why were markets so shaken?

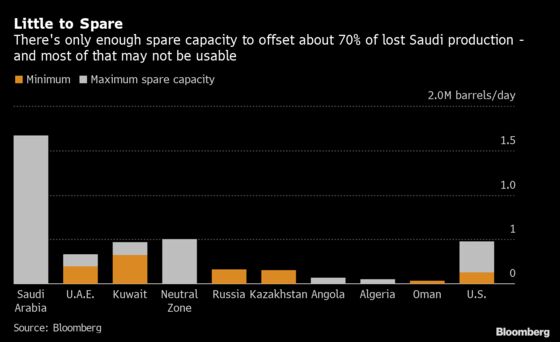

This was the blow to oil production that everybody feared because Saudi Arabia holds almost all of the world’s spare capacity -- seen as insurance against unexpected supply disruptions. With Iranian oil sales curtailed by U.S. sanctions and Venezuela’s industry in disarray from sanctions and a collapsed economy, the world’s supply buffer was already worrisomely inadequate. Plus, tensions were heightened due to attacks earlier in the year on several oil tankers in the vital waterway of the Strait of Hormuz and on Saudi Arabia’s East-West pipeline and Shaybah oil field.

2. What did the attack do to Saudi capacity?

The Abqaiq processing facility hit in the attack is the heart of the Saudi oil industry. It takes the output from almost all of Saudi Arabia’s onshore fields, including Ghawar, Shaybah and Khurais, removing sulfur and stabilizing the crude for onward delivery to the kingdom’s refineries and export terminals. It’s also the starting point for the East-West Pipeline that delivers Saudi crude to Red Sea export terminals, bypassing the contentious Strait of Hormuz. Most of Saudi Arabia’s capacity buffer needs to be processed at Abqaiq.

3. How fast can Saudi Arabia repair the damage?

The Khurais oil field resumed production at 30% of capacity after 24 hours, although it’s unclear how much it is now pumping. By Sept. 17, Abqaiq was processing about 2 million barrels a day, according to Saudi Energy Minister Prince Abdulaziz bin Salman. Saudi Arabia’s production capacity will reach 11 million barrels a day by the end of September and be restored to the pre-attack level of 12 million barrels by the end of November, the minister says. Some analysts have expressed doubts that the work will be completed so quickly: Consultancy Rystad Energy predicts Abqaiq’s capacity will only be fully restored “as we approach the end of the year.”

4. Can other supplies make up for the loss?

Oil price moves reflect concerns that, even if replacement supplies are forthcoming -- either from other producers, or from emergency stockpiles -- there will inevitably be delays and mismatches between the location of supplies and where they’re needed. The attack on Abqaiq made it impossible for Saudi Arabia to tap its own spare capacity, which lies largely in its onshore oil fields. That makes the present situation different from past disruptions. In the case of Iraq’s invasion of Kuwait, for instance, the lost output from those two countries was quickly replaced with increases from Saudi Arabia and Venezuela. Most oil producers are now pumping as much as they can from their fields, but only a handful of members in the Organization of Petroleum Exporting Countries have any significant head room. Kuwait and Abu Dhabi have already offered additional cargoes.

5. Can anything else be done to boost supplies?

Saudi Arabia can probably add about 250,000 barrels a day from its offshore fields, which do not depend on Abqaiq, according to Robin Mills, CEO of Dubai-based consultant Qamar Energy. The Neutral Zone, shared by Saudi Arabia and Kuwait, could pump as much as half a million barrels a day, but production there has been idle since 2015 as the result of a dispute between the two countries and would take as much as six months to restart, according to Mills. Saudi Arabia will use its own stockpiles of crude, both at home and those held near oil consumers in the Netherlands, Egypt and Japan. It told the Joint Organisations Data Initiative that it held 180 million barrels of oil in storage at the end of July, the most recent month for which data are available, but it is unclear how much of this will be available for sale and how much is needed as a minimum operating level.

6. What about emergency stockpiles?

Strategic reserves in oil consuming countries may have to be tapped. While those are adequate to cover any immediate shortfall from the attacks on Saudi Arabia, they would struggle to offset all of the loss of Saudi production for more than about three months. U.S. President Donald Trump has authorized the release of oil from the nation’s emergency oil reserves, while Japan and South Korea have also signaled their readiness to tap emergency reserves. The International Energy Agency issued a statement after the attack saying that it was monitoring the situation “closely” and pointing out that “for now, markets are well supplied with ample commercial stocks.”

7. What are the worries going forward?

Saudi Arabia, with its huge production, has for decades been the oil market’s great stabilizer. The attack could have a lasting impact on oil market sentiment, as it shows that Saudi oil infrastructure is much more vulnerable than has been assumed. Rising crude oil prices also inevitably feed through into the prices consumers pay at the pump for gasoline and diesel and to the cost of home heating oil and feedstocks for making plastics and the other products that depend on oil-based chemicals. But the oil shock alone won’t lead to a global recession, according to RBC Capital Markets’ Global Macro Strategist Peter Schaffrik.

The Reference Shelf

- Saudi wealth and weaponry still can’t guarantee oil’s protection.

- Making plastic and heating homes will cost more after Saudi attack.

- A weakened Iran shows it can still hold the world economy hostage, says Bloomberg Businessweek.

- QuickTake: How U.S. presidents use the Strategic Petroleum Reserve.

- Bloomberg Opinion: Julian Lee says the Saudi attack is what everyone feared.

To contact the reporter on this story: Julian Lee in London at jlee1627@bloomberg.net

To contact the editors responsible for this story: Alaric Nightingale at anightingal1@bloomberg.net, Andy Reinhardt

©2019 Bloomberg L.P.