What ‘Keepwell’ Means With Bonds Like Evergrande’s: QuickTake

How a ‘Keepwell’ Clause Protects China Bonds (or Not)

(Bloomberg) -- A potential restructuring at one of China’s largest, state-run managers of distressed debt -- China Huarong Asset Management Co. -- and fears of a default by the world’s most indebted developer -- China Evergrande Group -- have drawn fresh attention to the labyrinthine structures that Chinese borrowers use to issue and guarantee offshore debt. The so-called keepwell provisions are supposed to protect a foreign bondholder in case the mainland company runs into financial trouble. The problem is the clause essentially amounts to a “gentlemen’s agreement,” and is only starting to be tested in court.

1. What is a keepwell?

It’s a type of credit protection mainly seen in China’s $850 billion market for dollar bonds (those sold outside mainland China, denominated in U.S. dollars). The keepwell provision often involves a Chinese company’s pledge to keep an offshore subsidiary that is issuing the bonds solvent -- but without any guarantee of payment to the bondholders. (Actual guarantees require regulatory approval but keepwells don’t.) The clauses often include an agreement where the parent will purchase equity interest or assets in the offshore subsidiary as a way of servicing payments on overseas notes, according to an analysis by Fitch Ratings. Terms can vary, with different definitions of default, trigger events or what actions the keepwell provider promises to take.

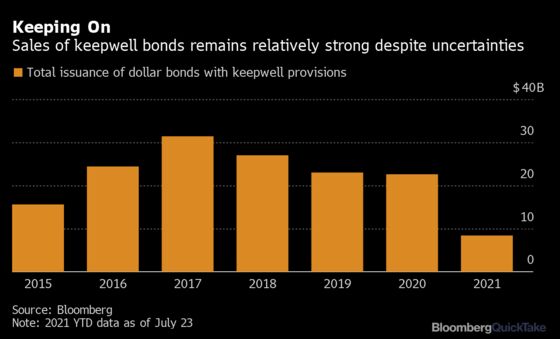

2. How much is out there?

About $110 billion of Chinese offshore bonds outstanding, or about 13% of the total, have the keepwell structure, Bloomberg-compiled data show. That includes some $25 billion from Chinese real estate firms, a risk-laden but popular sector. Nearly all of China Huarong’s $20 billion in dollar bonds have them, as do some of Evergrande’s. A record number of notes with such provisions were issued in 2017 and the pace has held fairly steady.

3. Why are they in the news now?

Pressure has been mounting on Evergrande since word of a possible cash crunch last year spooked investors. The developer has repeatedly said its relationships with creditors are normal and has made all of its payments to bondholders on time. But investors have been increasingly pricing in the risk of default amid a steady stream of reports about wary Chinese lenders and overdue payments to suppliers. Investors also are pondering worst-case scenarios for China Huarong, whose shares were suspended April 1 after it said its auditor needed more time to complete its financial results. That had investors worried about whether they would be repaid or forced to take a loss and spurred a historic selloff in the bonds. The firm is considered investment grade though some of its bonds have been trading at junk levels, in part due to uncertainty over how much protection the keepwell clauses offer.

4. What have the courts said?

In November 2020 a court in mainland China for the first time effectively recognized creditors’ claims on a Chinese defaulter’s offshore bonds that were backed by a keepwell provision. The potentially precedent-setting order, in the case of CEFC Shanghai International Group Ltd., came a few months after an administrator had rejected keepwell notes in the high-profile case of Peking University Founder Group Corp. That sprawling conglomerate, with medical and internet businesses, entered a court-led debt restructuring in February 2020. A lot of bonds sold by its overseas subsidiaries had keepwell provision, and the people who bought them are initiating legal action in Hong Kong and elsewhere. Another closely watched case is taking place at another defaulter, Tsinghua Unigroup Co. where the parent has said it’s not responsible for honoring repayment on offshore bonds with this provision.

5. How did we get here?

Chinese companies began using the keepwell structure in late 2012 in a bid to assuage concerns of skittish overseas investors about a bond issuer’s creditworthiness. They became increasingly popular as policy makers in Beijing adopted a more market-led approach to business and allowed corporate bond defaults to rise. In 2017 the State Administration of Foreign Exchange, a market regulator, issued new rules regarding guarantees that made it easier for domestic companies to bring home cash raised through offshore bonds. But according to China International Capital Corporation, an investment bank, some Chinese issuers have stuck with the keepwell structure because the rules for where the proceeds can be used are more flexible and there are still fewer regulatory approvals required.

The Reference Shelf

- Follow Bloomberg’s China Credit Tracker here.

- Bloomberg News goes inside China Huarang’s debt debacle.

- Bloomberg Opinion’s Shuli Ren assess Evergrande’s endgame and asks who will pick up the tab for Huarong’s troubles.

- More on Fitch’s report and an earlier warning from Moody’s.

- Another QuickTake on how China is opening its financial sector, sort of, and why China is shaking up its credit-rating industry.

©2021 Bloomberg L.P.

With assistance from Bloomberg