Fintech

Fintech

(Bloomberg) -- Not so long ago, homebuyers, entrepreneurs and investors went hat-in-hand to the bank to apply for a mortgage, small-business credit line or brokerage account. Financial technology, or fintech, is rapidly changing all that by making it easier to save, borrow and invest online or with a mobile device, without ever dealing with a traditional bank. For old-fashioned banks and money managers, fintech is causing dramatic upheaval, possibly the most since mainframe computers first whirred to life on Wall Street in the 1960s. It’s caught the attention of regulators, consumer advocates and industry veterans — some cheering, others booing, but all wondering: Will a digitized financial-services industry mean lower costs, more innovation and greater access for all? Or will the dominant players ultimately stay on top, with their hefty fees, commissions and compensation, as well as their gatekeeper roles, largely intact?

The Situation

Fintech has unsettled just about every corner of global finance. Traditional bankers at first scoffed when the arrivistes promised to reinvent their business. Then services such as Venmo, the person-to-person money-transfer app owned by PayPal Holdings Inc., started displacing established bank products, so big banks are now joining the revolution. Dozens have teamed up to offer Zelle, a Venmo-like app. Goldman Sachs Group Inc. rolled out Marcus, a mobile-banking app that now claims 1.5 million customers. Industry-friendly regulators in the U.S., U.K. and Singapore have set up or proposed so-called sandbox programs to help fintech firms develop new offerings with lighter oversight. European Union banks as of 2018 had to give qualified fintech firms access to account data, such as credit-card transactions, if bank clients requested it. Investors are piling in: Adyen NV, a Dutch startup that processes Uber, Netflix and Spotify payments, joined 28 other companies in the pantheon of fintech unicorns — those with valuations of $1 billion or more — when it raised $1.1 billion in a June 2018 stock offering. All this is less welcome news for those in old-line financial jobs. Vikram Pandit, a former Citigroup Inc. chief executive officer, has said that technology could replace about 30 percent of banking jobs by 2023.

The Background

Financial services largely fended off Silicon Valley until 2008, when the global financial crisis caused big banks and money managers to lose consumers’ trust. At the same time, fintech entrepreneurs found a welcome reception among millennials. Free software and cloud computing also made it easier than ever to launch a tech company. Soon enough, fintech newcomers were everywhere, though mostly in California, New York, Berlin, Shanghai and London. Once fintech pioneers showed that financial transactions could be as simple as shopping on Amazon, the banks swung into action. Some operate fintech accelerators — programs that provide startups with office space and seed money — to unearth promising innovations they might want to adopt. Fintech has caught a wave in China, where Ant Financial Services Group, a digital bank spun off from tech giant Alibaba Group Holding Ltd., claims 500 million customers. In mid-2018, it raised $14 billion in a single funding round.

The Argument

Fintech companies are getting a lot of attention, but they’re not about to replace Wall Street’s stalwarts. PayPal, a fintech granddaddy, only joined the ranks of global financial powerhouses in early 2018, 20 years after its founding, when it cracked $100 billion in stock-market value. Some startups have struggled after early missteps. One example is LendingClub Corp., a peer-to-peer lender whose founder was ousted after an internal review uncovered conflicts of interest and abuses involving loan sales. In China, where peer-to-peer lending has skyrocketed, a lack of regulation created an opening for scams, leading to a government crackdown. By mid-2018, thousands of the lending websites had been forced shut or had failed. Some U.S. states and consumer advocates are wary of letting fintech companies apply for federal banking charters, arguing that the states that currently oversee them are better at balancing innovation with consumer protection. Such critics also disparage regulatory sandboxes. As one state regulator put it, “Toddlers play in sandboxes. Adults play by the rules.”

The Reference Shelf

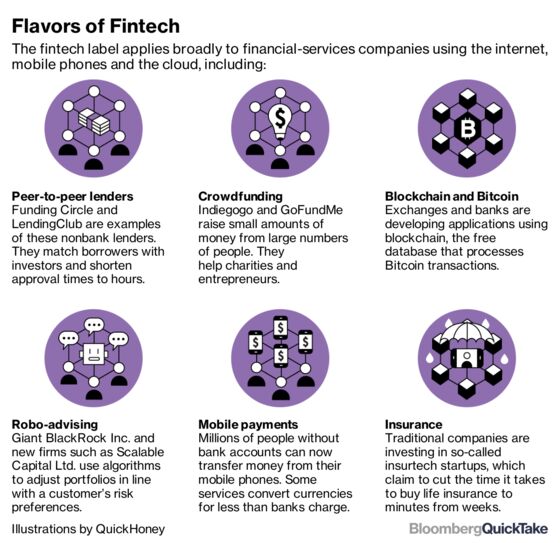

- Bloomberg explores fintech more deeply with QuickTakes on peer-to-peer lending, robo-advisers, crowdfunding, artificial intelligence, mobile payments and bitcoin.

- Consulting firm Accenture published this report on fintech’s global evolution and outlook.

- This McKinsey report says “fintech companies are undoubtedly having a moment.”

- The U.S. Treasury’s Comptroller of the Currency, a bank regulator, is proposing to issue a new bank charter for fintech companies.

- Jamie Dimon, the chairman and CEO of JPMorgan Chase & Co., previewed the bank’s move into fintech in his 2017 shareholder letter.

To contact the editor responsible for this QuickTake: Paula Dwyer at pdwyer11@bloomberg.net

©2018 Bloomberg L.P.