Counting the Toll of U.K.’s Costliest Banking Scandal

Counting the Toll of U.K.’s Costliest Banking Scandal

(Bloomberg) -- It was the costliest scandal in the history of British banking: the mis-selling of payment protection insurance, or PPI, to tens of millions of borrowers who didn’t want it, didn’t understand what they were buying or whose policies didn’t cover what they thought. Starting in 2006, financial regulators began issuing fines over problems with PPI, and a wave of refund requests crashed over U.K. lenders. The period for filing claims has now ended and banks are ready to turn the page. But shareholders are still paying the price.

1. What was payment protection insurance?

PPI was a financial product that covered some or all of a borrower’s loan repayments in the event he or she suffered an accident, sickness, involuntary unemployment or loss of life. It was sold alongside a range of other financial products, such as car loans, credit cards, store credit and mortgages. The premiums were usually billed in monthly installments tacked on to loan payments and were often relatively expensive, ranging from 13% to as much as 56% of the total credit, according to the Citizens Advice Bureau. The policies were sometimes a very poor deal: In one notorious example, insurance sold with a mortgage cost 20,838 pounds (about $26,000) over the term of the loan, but the maximum a customer could claim was just 31,000 pounds.

2. What did the banks do wrong?

Aside from the questionable value of the insurance, PPI was often sold using aggressive tactics. Some customers were pressured into buying it, while others were promised cheaper loans if they took it. In some cases, banks sold PPI without providing a full explanation of what it would (and wouldn’t) cover or making clear that clients had to pay additional fees. In the worst cases, banks misled customers by telling them PPI was mandatory -- or even charged them for it without permission. Cases of alleged abuse date back to the early 1990s, but it was in the mid-2000s that the practice peaked and caught the attention of regulators.

3. What was the compensation?

Successful claimants got back some or all of what they had spent on premiums, minus any reimbursements they’d already received from insurers, with the amount depending on how egregiously they’d been abused when the policies were sold. The massive flow of claims against banks and insurance companies was overseen by Britain’s Financial Conduct Authority. Most were filed against the sellers, who rejected half or more of them, and about a third of those were referred to the Financial Ombudsman, which overturned 80% of the rejections.

4. What’s been the fallout?

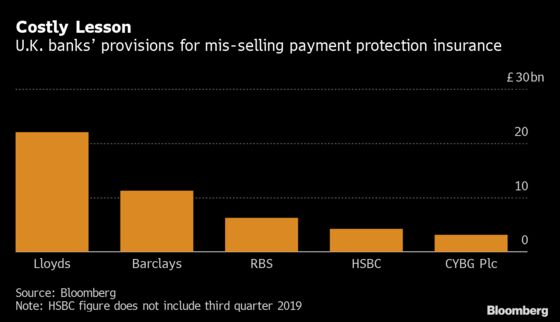

Banks and insurance companies were fined hundreds of millions of pounds by regulators, primarily for how they handled compensation claims. But the far bigger price came with the payouts they had to make for customer refunds, which reached a total of 36 billion pounds between 2011 and August 2019. As the crisis unfolded and compensation claims piled in -- fueled by advertising and telemarketing campaigns urging Britons to file -- banks repeatedly took unexpected hits to their quarterly earnings, even as executives reassured shareholders that the end of the pain was in sight. All told, banks have booked 53.3 billion pounds in provisions, including an estimated 12.5 billion pounds to administer claims. That dwarfs the cost of the scandals surrounding manipulation of the Libor benchmark interest rate and the rigging of foreign-exchange rates.

5. How did the banks get caught?

Concern about PPI swirled around the personal-finance press as far back as the 1990s and then began appearing in the mainstream media. U.K. financial services regulators visited hundreds of firms in 2005 and sent letters to chief executives to stop the products being sold with unsecured personal loans. Banks organized themselves for a legal fight, but in 2011, a court ruled they might have to pay compensation to customers. That’s when Lloyds Banking Group Plc Chief Executive Officer Antonio Horta-Osorio broke with his peers and signaled an openness to consumer settlements. He set aside billions in provisions against an anticipated wave of claims, saying “these problems have to be closed. We are drawing a line under PPI.”

6. Wasn’t there blowback over the claims process?

After Lloyds opened the floodgates, an ecosystem of claims management companies sprung up to help consumers seek restitution. They took a cut of the payback, sometimes in excess of 25%. By 2013, more than 1,000 such firms were in operation, bombarding Britons with hundreds of millions of text messages and robo-calls urging them to file claims. Some claims management companies were warned, fined or shut down by the government for shoddy practices. The U.K. government also pushed people to claim: For two years, the FCA ran a television ad campaign, paid for in part by the banks, that featured a likeness of the disembodied head of Hollywood actor and former California governor Arnold Schwarzenegger, urging people to “do it nooooow” and see whether they qualified for redress.

7. Is this the end of it?

There is still the possibility that banks will pay out more claims in individual PPI cases that go to court, but an Aug. 29 deadline ended the formal claims process overseen by the FCA. Shareholders are still feeling the pain: Lloyds is curbing a previously announced share buyback to set aside as much as 1.8 billion more pounds to cover last-minute PPI claims, while Barclays Plc is ponying up an additional 1.6 billion pounds for the late rush, threatening the lender’s promise to return more money to shareholders. It may take until early 2020 for the last refunds to be processed and for a final tally of the cost.

8. Could this happen again?

Selling PPI simultaneously with a loan or credit product was banned by Britain’s Competition Commission in 2011. The insurance still exists, but most banks no longer offer it. Regulators are turning their attention instead to fintech, payday loans and mis-selling of investment and retirement products. Claims management companies, fishing for their next business opportunity after the PPI bonanza winds down, are set to jump on new avenues to pursue claims against financial-services companies.

The Reference Shelf

- The PPI page for the U.K. Financial Conduct Authority.

- The FCA enlists Arnold Schwarzenegger to push consumers to file claims.

- Bloomberg: U.K. banks pay $66 billion as costliest ever scandal winds down.

- Landmark 2011 report from the Citizens Advice Bureau on PPI.

--With assistance from Viren Vaghela.

To contact the reporters on this story: Stefania Spezzati in London at sspezzati@bloomberg.net;Harry Wilson in London at hwilson57@bloomberg.net

To contact the editors responsible for this story: Ambereen Choudhury at achoudhury@bloomberg.net, Andy Reinhardt, Keith Campbell

©2019 Bloomberg L.P.