Active v. Passive? Why It’s Not That Simple Anymore

Active v. Passive? Why It’s Not That Simple Anymore

(Bloomberg) -- For the past five decades a radical idea has been eating away at the soul of the global asset management industry: What if you can’t beat the market? At least, not consistently. Then all the time, energy and — most important — money spent trying to do so is wasted. You’d be better off buying a so-called passive fund that holds all the stocks in an index like the S&P 500. This idea became an $11 trillion tidal wave of cash, bringing with it concerns about whether passive portfolios are distorting financial markets. Now the debate is shifting again. Rather than a black-and-white choice, active is getting more passive and passive is getting more active. What’s unclear is whether this will improve investment tools or re-create the inefficiencies of the past.

1. What triggered the shift?

In and around the 1960s, a confluence of factors (in particular the advent of computers) allowed a small group of academics to show exactly how most money managers were performing versus the U.S. stock market. The conclusion was famously articulated by Burton Malkiel in his 1973 book, “A Random Walk Down Wall Street,” in which he argued that “a blindfolded monkey throwing darts at the stock listings” would do as well as the pros. Trailblazers at firms including Wells Fargo & Co. and Vanguard Group Inc. developed index funds with the idea that by accepting “average” returns engineered by buying a broad swath of the market — but spending far less on fees — most investors would do better.

2. How did it take hold?

Year after year the evidence against stockpicking accumulated as the technology to automate buying and selling to match an index got better. Fewer than 15% of active U.S. large-capitalization funds beat the market over the past decade, according to 2020 data from S&P Global. Meanwhile fees for passive funds can be as low as 0.1% of assets or less, compared with more than 1% for the average active mutual fund. The dam finally broke over the last decade thanks to a combination of easier-to-trade products like exchange-traded funds (ETFs) and the mistrust of money managers sown by the 2008 financial crisis.

3. What’s the fallout?

By late 2019, passive strategies had officially swallowed up more than half of publicly traded assets in U.S. equity funds. The share of passive strategies in areas like non-U.S. stocks or bonds has yet to surpass that of active money, but the same trend is unfolding. Used by both institutional and retail investors, index funds are a big reason why more than half of all Americans are invested in the stock market today, a bigger share than other rich countries. Companies such as BlackRock Inc., the world’s biggest asset manager, have also become the largest shareholders in many U.S. corporations, leading to much handwringing about the potential dangers of the approach. Concerns range from stock price volatility to the inefficient allocation of capital toward companies that have the big weightings in an index. Another worry is that index approaches could delay a shift to so-called ethical investing if investment managers neglect their traditional role as powerful company watchdogs.

4. What’s happened to active investing?

Active managers have mounted a spirited defense of their craft. They’ve argued that the period since 2008 has been an abnormal one, with many stocks moving in lockstep rather than trading on their individual earnings prospects. Bad-mouthing indexing as “a blob,” they posit that passive distortions will create more opportunities for those who can spot bargains and avoid overpriced securities.

5. How are active managers adapting?

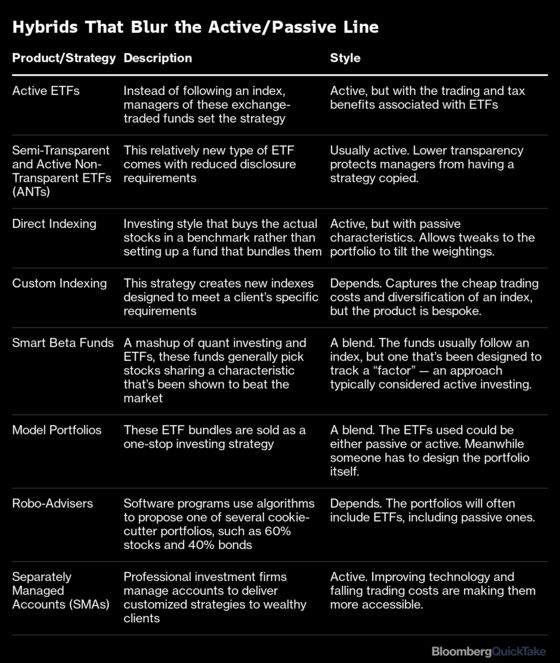

They’re creating hybrid styles, blurring the lines with passive. New rock stars such as Cathie Wood at Ark Investment Management are popularizing the use of active strategies inside ETFs. These capture the tax and trading benefits of an ETF but give managers more discretion. Fees are slightly higher, and so far performance has varied widely. After Wood’s market-beating success in 2020, such funds have launched at more than double the rate of passive vehicles in 2021.

6. How passive is passive investing?

The field has evolved from buying the whole market to buying ever-smaller or more complicated slices of it and using a mixture of strategies to the point where many investors have what amounts to actively managed portfolios via a selection of index funds. As more cash has shifted to indexing and ETFs there’s been an explosion in the number of gauges and funds, with about 3 million indexes now in existence globally and about 10,000 ETFs. Meanwhile, big money managers are racing to develop so-called custom indexing — another hybrid approach that’s arguably more active than the name suggests.

The Reference Shelf:

- Meet the man who started the $11 trillion index revolution.

- Even Harry and Meghan are joining the build-your-own index craze.

- Related QuickTakes on ethical investing and active ETFs.

- A special report on active management from Bloomberg Markets.

©2021 Bloomberg L.P.