A Guide to China's $10 Trillion Shadow-Banking Maze: QuickTake

A Guide to China's $10 Trillion Shadow-Banking Maze: QuickTake

(Bloomberg) -- Shadow banking in China has ballooned into a $10 trillion ecosystem which connects thousands of financial institutions with companies, local governments and hundreds of millions of households. The practice is now at the center of a Chinese government-led regulatory crackdown aimed at defusing financial risks that threaten the wider economy. Unlike in the U.S., traditional commercial banks drive shadow banking, or unregulated lending, in China. That’s because the banks have been able to keep shadow-banking assets off their balance sheets, thereby sidestepping regulatory constraints on lending. So what exactly makes up China’s giant shadow-banking network, the fastest-growing among major economies? Here’s a glossary:

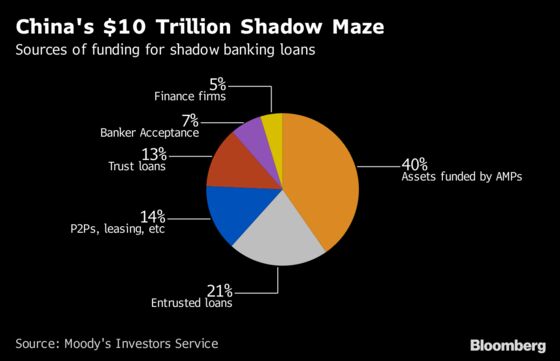

Asset Management Products

The largest funding source for shadow loans, these bear little resemblance to the investments offered by fund managers in London or New York. AMPs are effectively high-yielding deposit accounts offered by banks, brokerages and other financial firms to raise funding from companies, households and even each other. Because of the widespread perception that they’re guaranteed by the issuers, and that the government stands behind China’s financial institutions, AMP issuance has exploded, reaching 100 trillion yuan ($16 trillion) in 2017. Not all of that flows into shadow banking, but as issuers try to match the over-sized yields promised to depositors, a good-sized chunk has gone into funding loans to weaker borrowers and speculative areas such as real estate and stocks.

Wealth Management Products

This is the name given to asset management products issued by banks, about 30 percent of all AMPs. As part of the regulatory clampdown, financial institutions have until the end of 2020 to comply with tougher rules aimed both at breaking the idea that AMPs carry implicit guarantees and at suppressing riskier types of lending.

Entrusted Loans

The No. 2 shadow-banking source, entrusted loans provide a way for cash-rich companies to lend to other firms by using banks as middlemen. However, rather than acting solely as agents, some banks have used the process to make the loans themselves. And because of light regulation, many such loans have gone to risky borrowers like local government financing vehicles or property developers. Regulators have acted, though, for instance stopping banks putting up their own money and enforcing their role purely as intermediaries.

Trust Loans

These are loans provided by China’s 68 trust companies, which invest money on behalf of wealthy individuals but into which banks also channel funds. Again, light regulation meant that loans were directed to higher-risk borrowers who couldn’t get money from banks, and at such a rate that until recently these were the fastest-growing shadow-banking segment. The trust companies had 26.3 trillion yuan of assets under management by the end of 2017, one third of which was used for lending. Regulators in December banned trusts from using bank funds to invest in stocks, property and local government financing vehicles. At least eight trust products have delayed payouts to investors this year and, with more than 3.3 trillion yuan maturing in the second half, the problems are expected to deepen.

Internet Financing

Peer-to-peer lending and other internet financing have surged outside the gaze of regulators -- accounting for about 9 percent of shadow financing -- but authorities are coming down hard. They’ve enforced a cap on interest rates and closed down illegal operators. The number of platforms has shrunk from almost 4,000 to 1,800, according to Shanghai-based researcher Yingcan Group, which says only 800 are likely to survive long term.

Interbank Funding

Though not a direct source of money for shadow loans, interbank funding is another engine for the industry because it allows smaller banks that lack the branch networks of larger rivals to inflate their balance sheets and sidestep regulatory limits on lending. Interbank funding has also provided a source of leverage for Chinese funds and brokers to invest in bonds, adding to the hidden and risky inter-dependencies in China’s financial system. To address this, China last year imposed a limit on interbank liabilities of no more than a third of a bank’s total liabilities.

Structured Deposits

Faced with restrictions on AMP issuance, banks and other financial firms have turned to products that include yield-enhancing features such as options contracts. For instance, a structured deposit may offer a yield of 5 percent that would be reduced to 1 percent in the event of something -- usually unlikely, if not impossible -- happening, such as the yuan hitting 5 per U.S. dollar within a certain time frame. The practice allows issuers to offer turbo-charged yields that they are often later forced to subsidize. That way they can bypass regulations forbidding banks from guaranteeing returns to investors. Regulators are planning to ban the sales of some structured deposits.

The Reference Shelf

- China’s $10 trillion shadow bank crackdown has a long way to go.

- QuickTake explainers on how shadow banking is booming outside regulators’ grip, how China is getting serious about financial risks and China’s war on online loans.

- QuickTakes on WMPs and entrusted bonds.

To contact Bloomberg News staff for this story: Jun Luo in Shanghai at jluo6@bloomberg.net

To contact the editors responsible for this story: Marcus Wright at mwright115@bloomberg.net, Grant Clark

©2018 Bloomberg L.P.

With assistance from Editorial Board