Why China’s Wild Stock Swings May Get Easier to Ride

Why China's Wild Stock Swings May Get Easier to Ride: QuickTake

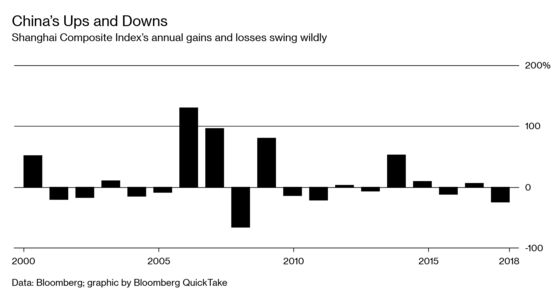

(Bloomberg) -- China’s $7.6 trillion stock market is the world’s second largest but is far from the most sophisticated. Global investors have long clamored for improvements in one area in particular: the ability to hedge their investments. As index compilers begin adding Chinese stocks to their gauges, meaning many fund managers must purchase them, investors are demanding tools that allow them to protect against declines in one of the most topsy-turvy markets, which started the year among the world’s worst-performing and by April was the best. It looks like China may heed the call.

1. What are investors demanding?

Derivatives products such as futures contracts, which are standard practice for many fund managers in major markets. Futures can be used to cushion a portfolio against sudden price movements or to follow a particular trading strategy. But Chinese authorities have kept tight control by, for example, making it difficult to trade derivatives or to short-sell shares, which refers to a practice where traders profit by selling borrowed shares and buying them back at a lower price.

2. Why is that a problem?

China’s market is among the most volatile, regularly swinging between out-sized losses and gains, in part because it is dominated by retail traders. Now that major index compilers are including Chinese equities in their gauges, institutional investors have little choice but to buy them, meaning their investments are at the mercy of those wild swings. After MSCI Inc. quadrupled the weighting of China’s equities in its emerging markets index this year, an executive at the firm said investors were reluctant to see further increases until more hedging tools were available.

3. What can international firms currently do?

Very little, compared to markets like the U.S. While foreigners have been given direct access to futures markets for iron ore and oil, equity derivatives remain insignificant. That’s because they were partly blamed for China’s epic stock market crash in 2015. In the same vein, short-selling is highly restricted. Investors instead use proxies such as Hong Kong-listed stocks, exchange-traded funds or structured products, which are usually harder to trade and more expensive than standard derivatives products. There is also a Singapore-listed futures contract for the FTSE China A50 Index, often Asia’s most-traded contract. The downside is this captures just a small slice of China’s market.

4. Is change afoot?

Highly likely. Chinese regulators have repeatedly spoken about loosening rules around hedging products in recent months. In April, an official at the securities regulator outlined plans to ease restrictions on domestic and international investors trading stock index futures, and voiced support for a plan by Hong Kong Exchanges & Clearing Ltd., or HKEX, to start futures contracts based on shares listed in China. HKEX is also discussing with its Chinese counterparts ways to make it easier to short Chinese equities via the stock-trading link between Hong Kong and mainland China.

5. What’s in it for China?

As much as $100 billion will likely flow into China’s stock market from abroad in 2019, according to Harvest Global Investments Ltd. analyst Yannan Chenye, as FTSE Russell and S&P Dow Jones Indices follow MSCI in including China-listed shares in their indexes. Investment from international fund managers helps China balance its capital account and reduces the market’s reliance on those unpredictable retail investors. Regulators have gotten the message from index providers and their investor base that those investments will only deepen if hedging tools are improved.

6. What about other asset classes?

The People’s Bank of China made clear in October that it’s looking at ways to encourage risk management in the bond market. HKEX has been talking to regulators in Hong Kong and China about providing fixed income hedging tools. Offshore-traded China treasury bond futures may start this year, Chief Executive Officer Charles Li said in February. Also on the docket are duration-hedging tools, forwards, repurchase agreements and cross-currency swaps linked to the U.S. dollar and Chinese yuan, according to Julien Martin, general manager of Bond Connect Co., a joint venture between exchanges in Hong Kong and China.

The Reference Shelf

- A QuickTake on China bringing in hedging tools in bond markets.

- Record bond failures breathe new life into CDS-like tools in China.

- MSCI boosts China stock weighting.

- A QuickTake on why indexes are a big deal for China, another on China’s inclusion in a global bond index and another on why China wants foreigners buying its bonds.

--With assistance from Kana Nishizawa and Lucille Liu.

To contact the reporter on this story: Benjamin Robertson in Hong Kong at brobertson29@bloomberg.net

To contact the editors responsible for this story: Sam Mamudi at smamudi@bloomberg.net, Grant Clark, Paul Geitner

©2019 Bloomberg L.P.