What’s Next for Bitcoin?

After Crypto Booms, Busts and Crackdowns, What Next?: QuickTake

(Bloomberg) -- Last year, Bitcoin led a motley pack of so-called cryptocurrencies in one of the great booms in market history, soaring over 2,000 percent to its peak. Since then, it’s led an epic bust that rivals the dot-com era stock market collapse. But there are still plenty of true believers. And as the dust settles, investors and regulators find themselves still grappling with questions first raised when Bitcoin broke into public consciousness five years ago: What exactly is it? How do imitators like Ethereum, Ripple’s XRP and Bitcoin Cash work? Should I buy it? Where do cryptocurrencies fit into the future of money? Here’s a guide for those feeling at sea in these turbulent digital waters.

1. What’s been happening?

The total market value of all traded cryptocurrencies exploded late last year to peak at about $800 billion in January by one count. Four months later, though, the value of crypto-assets had plunged by about two-thirds, as regulators began to crack down and fear of big losses began to replace fear of missing out. By late June, Bitcoin had fallen by 70 percent -- close to the 78 percent fall of the Nasdaq Composite Index’s drop when the dot-com bubble burst -- while the worth of hundreds of other virtual coins fell close to zero. Even so, the total market value of traded cryptocurrencies still rested above $250 billion, many multiples of what it was a few years ago.

2. Is Bitcoin money?

In a way, yes, though it’s not necessarily a useful form of it. It’s possible to buy or sell some things with Bitcoin but very few people do. Extreme volatility is perhaps the biggest argument against treating cryptocurrencies as you would the dollar or the euro. The hallmark of a reliable currency is that it provides a stable store of value. You wouldn’t want to spend Bitcoin on groceries today if you thought its value might soar tomorrow, or take your salary in Bitcoin if you thought it might plunge.

3. So what is it?

Born out of the bitterness that followed the 2008 financial crisis, Bitcoin and its imitators aren’t bills or coins printed or policed by a government or bank. They’re electronic assets created and monitored by a community of users acting in a decentralized way, following protocols set down by the person or persons who dreamed them up. The “crypto” in the name refers to the encryption techniques used by so-called Bitcoin miners. And all the new currencies revolve around what’s seen as Bitcoin’s real innovation — blockchain, a publicly visible, largely anonymous online ledger that records the calculations miners perform to verify transactions without the need for a central authority.

4. Why are so many people down on Bitcoin?

You mean, why did legendary investor Warren Buffett call it "rat poison squared”? There’s a long list of reasons. Besides the massive price swings, Bitcoin and other cryptocurrencies have been connected with scams, money laundering, tax evasion, cyberthefts, exchange outages, excessive speculation and more. Risks like these may have been easier for regulators to overlook when Bitcoin and its peers sat on the far fringes of finance, but they are moving ever closer to the mainstream. The stakes are much higher now that mom-and-pop investors and Wall Street banks alike are piling in.

5. Is anyone overseeing this area of finance?

A wide range of regulators are trying to get a handle on cryptocurrencies. Turns out there’s little agreement about what they fundamentally are: currencies, commodities, securities or something entirely new. Thus you’ll see them called crypto-assets, digital tokens, coins or just “crypto.”

6. How are crypto-assets like commodities?

The vision behind Bitcoin laid out in a 2008 pseudonymous manifesto promised that no more than 21 million will ever be created. That means it’s sometimes compared with scarce commodities such as gold, whose value is determined solely by what people are willing to pay for it. Crypto-assets have become popular in places where hyperinflation erodes the buying power of the local currency (think Zimbabwe), or where sanctions block purchases

(think Venezuela and North Korea).

7. How are they like securities?

There’s an argument that some crypto-assets have the same characteristics as stocks, such as a share of ownership in a common endeavor and the expectation of making a profit from work done by a company. Much of the focus is on new coins or tokens offered by startups through so-called initial coin offerings, or ICOs. While they take different forms, ICOs let companies bypass the venture capital process by selling coins instead of shares. In some cases, the founders say coin buyers are prepaying to use a service that the company will build. In the U.S., the Securities and Exchange Commission has opened a broad probe into whether entities running ICOs are violating its rules by offering what are really securities, although a top SEC official said that neither Bitcoin nor Etherereum fell into that category. China has banned ICOs entirely. That didn’t stop them from raising more than $10.5 billion worldwide through the first half of 2018.

8. How are regulators clamping down?

Their approaches have run the gamut, from an exchange-licensing regime in Japan that was recently tightened to a largely hands-off system in Switzerland, though the anonymous and borderless nature of many digital coins makes them tough to control. China, once the world’s most active Bitcoin market, banned crypto-asset exchanges in 2017 and blocked access to overseas trading platforms. The crackdown came during government campaigns to stop money from leaving the country and to reduce financial risk. Most countries, notably the U.S., have not yet formulated a comprehensive regulatory strategy. But U.S. prosecutors are investigating whether traders have been manipulating the price of digital currencies.

9. How can I buy Bitcoin?

There are a bunch of ways, all with different risks. Individuals can buy crypto-assets directly from online exchanges that will trade them for regular currencies like the dollar, the euro or the yen. Most of the exchanges will offer to hold the asset for you in a digital “wallet,” although an alarming number of exchanges have been hacked. You can also hold the asset for yourself, in a digital wallet or in so-called cold storage: for instance, a thumb drive disconnected from the internet. Since December 2017, investors can place a wager on Bitcoin — betting it will either rise or fall — without having to own it directly, via futures contracts traded on two big U.S. exchanges.

10. What’s Wall Street’s approach?

Until recently, it mostly kept its distance. Now there’s lots of interest if not yet much action. Lenders including JPMorgan, Bank of America and Citigroup have barred customers from using their credit cards to buy cryptocurrencies to avoid the risk associated with these transactions. But Goldman Sachs Group Inc. planned to begin trading Bitcoin futures on behalf of customers. And everybody in finance is at least dabbling in blockchain, which is seen as an innovative way to handle transactions that could potentially upend a wide range of industries.

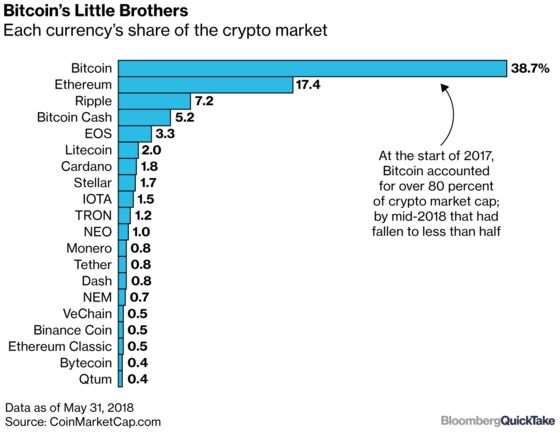

11. Why are there so many digital coins?

There are thousands of Bitcoin rivals, and it’s not clear how many of them are going to prove either legal or useful. Some were developed to overcome what their creators saw as flaws in Bitcoin, such as slow transaction times or high fees. Some of them were outright scams. Die-hard fans of newer currencies think they’ll eventually overtake their bigger cousin. The largest rival is Ethereum, which has a total market value half the size of Bitcoin. These so-called alt-coins are certainly getting more attention: By mid-2018 they accounted for more than half of all the money in crypto-assets, compared with less than a fifth at the start of 2017.

12. Who are the crypto true believers?

Here’s a short list of enthusiasts: Teenagers and hackers drawn by a disdain for authority and the libertarian aspirations behind Bitcoin’s creation. Technology geeks who believe they’re disrupting the marketplace and getting in early on the next chapter in the history of money. Financial firms and central banks that think something important will come out of all this even if Bitcoin withers. And there are also plenty of investors who aren’t true

believers but who hope to find one to sell their holdings to if crypto prices soar again.

The Reference Shelf

- QuickTake explainers on blockchain technology and crypto regulation.

- A QuickTake on Bitcoin’s wild price ride in late 2017.

- A Bloomberg View editorial on the value of blockchain technology.

- A Bloomberg News article on the history of crypto hacking, and a review of the many ways you can lose your Bitcoin.

- The Bank for International Settlement’s 2018 report on cryptocurrency.

- The original whitepaper outlining Bitcoin’s protocols.

- A Forbes article discussing the future of Bitcoin as a currency, as something used to buy Big Macs and other stuff.

To contact the reporters on this story: Sam Mamudi in Hong Kong at smamudi@bloomberg.net;Olga Kharif in Portland at okharif@bloomberg.net;Matthew Leising in Los Angeles at mleising@bloomberg.net

To contact the editors responsible for this story: Leah Harrison Singer at lharrison@bloomberg.net, John O'Neil

©2018 Bloomberg L.P.