Fed Seeks Economic Soft Landing, Rarely Seen in Wild: QuickTake

Fed Seeks Economic Soft Landing, Rarely Seen in Wild: QuickTake

(Bloomberg) -- U.S. unemployment is at rock-bottom levels. The stock market is near a record-high. Wages are finally rising and consumers are brimming with confidence. What could go wrong? Plenty, if the Federal Reserve missteps, as central banks often do in such heady times. The reason is that inflation, which has been unusually quiescent, could come surging back if the tight labor market overheats. The Fed hopes to avoid that by raising interest rates, but it could trigger a recession if it tightens credit too much. The ideal is what economists call a "soft landing." But getting this much-desired and often elusive condition can be more art than science.

1. What’s a soft landing?

In short, it describes the Fed’s main job these days: Slow the economy enough to prevent it from overheating, but not so much as to trigger a contraction in gross domestic product. Doing that takes a combination of smart policy-making and luck. Mark Zandi, chief economist of Moody’s Analytics Inc., likens it to “landing in the fog on an aircraft carrier that’s in the middle of choppy seas.”

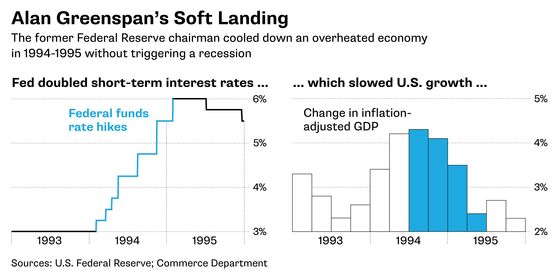

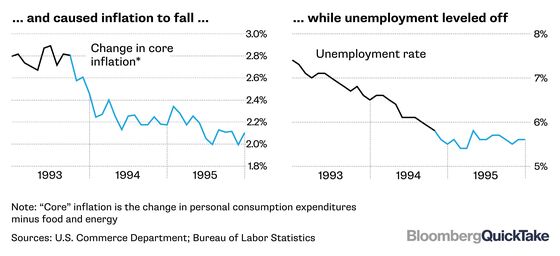

2. Has the Fed ever accomplished this?

Yes, but only once, in 1994 and 1995, under then-Chairman Alan Greenspan. The central bank back then doubled interest rates to 6 percent and succeeded in slowing economic growth without killing it off. The tighter credit did have adverse consequences, though. It led to huge losses for bond market investors and contributed to the 1994 bankruptcy of Orange County, California. Mexico was also compelled to seek a bailout from the U.S. and the International Monetary Fund.

3. Can the Fed do it again?

Theoretically, yes. But it’s even more difficult now than in 1994. That’s because unemployment back then was still elevated and the job market wasn’t as tight as it is now. May’s unemployment rate of 3.8 percent is already below what many economists say is its long-run sustainable rate. So achieving a soft landing today would mean not only slowing growth, it would also mean nudging up unemployment. The trouble, as outgoing New York Fed President William Dudley has noted, is that the economy historically “has always ended up in a full-blown recession” whenever joblessness has risen by more than 0.3 percentage point.

4. So why doesn’t the Fed just leave well enough alone?

Some economists favor this path, arguing that central bankers in the past have overreacted to inflation signs, depriving workers of the wage gains they’d make in a tight labor market. On the other hand, the Fed’s preferred inflation gauge hit its 2 percent target in March and April. While May figures for the Fed’s yardstick aren’t out yet, another inflation measure, the consumer price index, rose 2.8 percent from May 2017. That’s the fastest pace in more than six years, though the CPI historically runs about 0.5 percentage point higher than the Fed’s chosen metric. The worry is that, as companies find it increasingly difficult to find workers, they’ll bid up wages, which could lead to higher consumer prices as companies seek to protect profits. To short-circuit the wage-price spiral, the Fed would have to jack up interest rates to levels that could cause the economy to contract.

5. Is that the Fed’s only concern?

Some officials also worry that low interest rates risk pumping up asset prices to levels that will prove unsustainable. That’s what happened in the middle of the last decade when housing prices were bid up way too far -- with disastrous results. This time the concern focuses on stocks and bonds, especially risky corporate bonds. Indeed, Greenspan says that stocks and bonds are already in bubble territory. If he’s right and they do eventually burst, that could destroy trillions of dollars of wealth and tip the economy into a downturn.

6. So what’s the Fed’s strategy?

Gradually edge up interest rates to try to keep asset prices from rising too high and the unemployment rate from falling too low. Policy makers raised interest rates three times in 2017 and once in 2018, so far. They are roughly evenly split over whether to increase the benchmark rate two or three more times this year, including a widely-expected hike later on Wednesday. One big complication: President Donald Trump and Congress have stoked up the economy with tax cuts and higher spending just as Powell & Co. are trying to slow it down.

The Reference Shelf

- Bloomberg QuickTake explainer on why measuring inflation is such tricky business and one on the Fed unwinding its balance sheet.

- A 1995 research paper by economist Edward Yardeni says economic busts often are the result of central bank policy-engineering to correct failures in managing booms.

- Former Fed Chairman Alan Greenspan recounts his 2000 soft-landing miss in his book, "Age of Turbulence."

- The International Monetary Fund’s guide to how central banks tame inflation through inflation targeting.

--With assistance from Anne Cronin.

To contact the reporter on this story: Rich Miller in Washington at rmiller28@bloomberg.net

To contact the editors responsible for this story: Brendan Murray at brmurray@bloomberg.net, Alister Bull, Paula Dwyer

©2018 Bloomberg L.P.