Fannie Mae and Freddie Mac

Fannie Mae and Freddie Mac

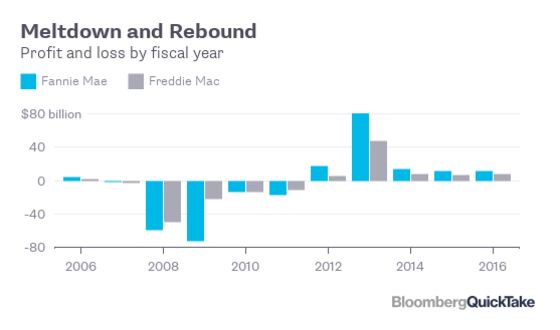

(Bloomberg) -- For decades, the mortgage giants Fannie Mae and Freddie Mac were the fat and happy foundation of the U.S. housing market. By buying and packaging home loans into bonds and absorbing much of their risk, they made it easier for homebuyers to get mortgages, and to get them on easier terms than are available in most countries. Created by the government and then spun off as shareholder-owned corporations, Fannie and Freddie churned out steady profits, as investors treated their debt as virtually risk-free. It was the best of both worlds — until the housing market melted down in 2008. The government's bailout of Fannie and Freddie has cost $191 billion. Since the agencies returned to profitability, they’ve repaid that amount and almost $100 billion more — and the housing market is more dependent on them than ever.

The Situation

President Donald Trump has pledged to free Fannie and Freddie from government control, and has a plan to do that without involving Congress, where a series of ideas for revamping the agencies have stalled. Responsibility for making that work lies with Treasury Secretary Steve Mnuchin and Mark Calabria, the head of the Federal Housing Finance Agency, which oversees Fannie and Freddie. Two of the biggest issues to be resolved are ensuring that they have enough capital to avoid needing another bailout during a downturn, and what kind of limited backstop the government would be willing to provide if that cushion wore thin. In 2019, Calabria and Mnuchin changed the terms of the old bailout to allow the companies to keep more of their profits, and Calabria has rewritten regulations about the size of their capital buffer. Democrats have reacted coolly to Trump’s plan. Mike Bloomberg, who’s running for the Democratic nomination to be Trump’s opponent in the November election, has put forward a very different approach: merging Fannie and Freddie to create one company officially backed by the government. (Bloomberg is the founder and majority owner of Bloomberg LP, the parent company of Bloomberg News.) Meanwhile, the companies also remain embroiled in a number of lawsuits filed by investors over the huge payments the agencies have made over the years to the government. As 2020 began, the Supreme Court was considering whether it would intervene in the wake of an appellate court victory for the investors.

The Background

Congress created the Federal National Mortgage Association in 1938 as a government agency with a mission of reviving the mortgage market after its collapse in the Great Depression. Traditionally, banks that made mortgages held on to them. By buying mortgages from lenders, Fannie Mae, as it became known, freed up money that the banks could use to make more loans. After World War II, that process helped fuel a housing boom and made 30-year fixed-rate mortgages the American norm — in most other countries mortgages have shorter terms or adjustable rates. In 1968, Congress converted Fannie into a for-profit, shareholder-owned company, in part to ease a debt burden fueled by spending on the Vietnam War. Freddie Mac, the Federal Home Loan Mortgage Corporation, was created as a federally-chartered corporation in 1970 to give Fannie Mae some competition. It was turned into a publicly traded company in 1989. The companies helped the market for mortgage-backed securities grow by guaranteeing the payments of bonds it sold — bonds that many investors treated as nearly as safe as those of the U.S. Treasury, because of what was seen as an implicit government guarantee. That meant the companies could borrow more cheaply than other lenders. The implicit promise was made explicit by the federal bailout, which came as the companies slid toward insolvency as the 2008 financial crisis moved toward its climax . Some conservative economists say their collapse was caused by Congressional requirements to back lending in poor areas. But most studies have pointed to their small capital reserves and decision to expand their investments in loans packaged by Wall Street during the housing boom, including subprime bonds. Fannie and Freddie now stand behind about half of new U.S. mortgages, compared with about a third in 2005.

The Argument

The disagreements that have blocked plans to reform Fannie and Freddie don’t always fall on partisan lines, but in general Republicans favor reducing the government’s guarantee and overall role in the housing mortgage industry, while many Democrats are concerned about measures that could make housing less affordable, especially for minority and lower-income borrowers. Within the industry, many bond investors, big banks and real estate agents worry about the economic damage that might be caused by changes that erode the safety of companies insuring $5 trillion of mortgage securities. All these factors have helped cement a status quo that few endorse but fewer have been willing to risk changing. Trump’s plan for an end run around Congress hinge on him winning re-election, as the immensely complicated task isn’t likely to be done by then, since it’s unlikely a Treasury Secretary appointed by a Democrat would share the same goals. The Trump plan has also been criticized as returning the agencies to the same ambiguous status — private corporations likely to be seen as having implicit government backing — that got them into trouble in the first place.

The Reference Shelf

- The takeover of Fannie and Freddie was addressed in the U.S. Financial Crisis Inquiry Report and a study by the Federal Reserve Bank of New York.

- The terms of the bailout agreement between the U.S. Treasury Department and Fannie Mae and Freddie Mac.

- A 2014 Bloomberg story about an attempt at legislation to wind down the companies. The legislation died later that year.

- A Bloomberg article about Fannie and Freddie shareholders’ battle for a share of the companies’ profits.

- A 2015 study by the Federal Reserve Bank of New York looks back at the 2008 bailout.

Joe Light contributed to the original version of this article.

To contact the editor responsible for this QuickTake: John O'Neil at joneil18@bloomberg.net

©2020 Bloomberg L.P.