What’s Next for Banks as Draghi Steps Down?

What's Next for Banks as Draghi Steps Down?

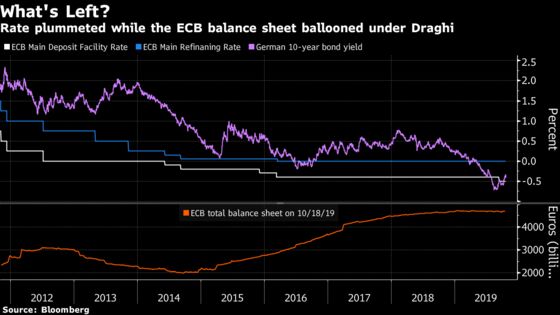

(Bloomberg) -- Arrivederci, President. Ending his eight-year tenure as head of the ECB, Mario Draghi could leave with the feeling of a job done: holding the euro-area together, whatever it takes. His accommodative policy pulled the old continent out of recession and helped create 11 million jobs. It also came at a cost for the central bank, with total assets doubling to about 4.7 trillion euros, while lenders’ margins have been hit by falling interest rates. The big question now is: what’s left in the ECB’s toolbox to fight the economic slowdown? But markets want to believe in a turnaround.

Draghi played a key role in preventing a meltdown in the banking sector during the sovereign debt crisis. The problem is that the industry never fully recovered in the following years, and the ultra-low rates have hurt them. Under Draghi’s term, euro-area lenders (SX7E) are down about 5%, while the Stoxx Europe 600 has gained nearly 70%. The broader European bank sector (SX7P) has done marginally better, up about 4% over the period.

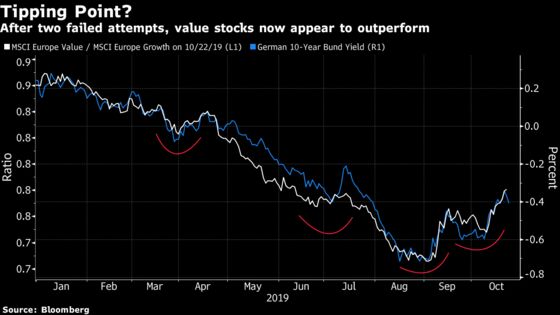

Ironically, the end of Draghi’s era coincides with the start of a turnaround -- albeit a tentative one at this point -- for bond yields and value stocks. Banks are the essence of the value trade as financials account for a third of the MSCI Europe Value index. Just this month, Credit Suisse, Morgan Stanley and Barclays strategists recommended being overweight on the sector. JPMorgan and Bank of America were already overweight European banks in September. All five brokers are bullish on value shares.

Some asset managers are also switching sides. Amundi Chief Investment Officer Pascal Blanque writes that value stocks are trading at all-time lows relative to growth, providing an attractive hunting ground.

In similar fashion, Claudia Panseri, co-head of cross-asset strategies at UBS Wealth Management, says the group went overweight financials recently because the valuation gap between consumer staples and banks was at a record high. Still, the strategist says this is tactical and driven by potentially improving macro data, in order to be less defensive or less exposed to bond proxies, and not a value trade.

“We don’t like the euro zone,” Panseri says, adding that the region is a value market driven by rates, inflation and economic expectations. The strategist sees lead indicators close to the bottom, but doesn’t expect bond yields to move up from here. That’s because the ECB will remain very accommodative, and inflation expectations will remain muted, so value or cyclical names shouldn’t “play out in the short-term,” she adds.

Indeed, in a world of crushed inflation, a ballooning ECB balance sheet and never-ending quantitative easing, investors are worried. The Fed was unable to stay out of some form of bond-buying for an extended period, and one key issue for Draghi’s successor, Christine Lagarde, will be to reconcile divergent views on stimulus.

Amundi’s Blanque says growing internal disagreements within the Fed and the ECB affect markets and will provide a new source of volatility, as it comes just when market expectations for central bank action is too high.

It’s part of the reason why Draghi has been pushing for governments to provide the fiscal stimulus needed to fight the economic slowdown. But that’s a step euro-area leaders are reluctant to take while doubts emerge about the efficiency of such intervention. Stimulus wouldn’t be without risks for the bond market, either.

So what can we expect today? Not much, according to economists, as monetary policy has been locked for three years. Still, a cut in the economic forecast could be on the cards as the ECB’s macro outlook is “too optimistic,” says Deutsche Bank Chief Economist Mark Wall, in a view shared by Maud Minuit, head of fixed income at La Francaise Asset Management.

“It isn’t a big event,” says UBS’s Panseri. People know that there won’t be a new message and today’s PMIs will probably be a bigger factor for markets, she says. As per my taking stock yesterday, I wouldn’t disagree.

In the meantime, Euro Stoxx 50 futures and S&P 500 contracts are both little changed ahead of the European open.

- Watch the pound and U.K. stocks after U.K. Prime Minister Boris Johnson was left hanging by the European Union as Brussels debates how long of an extension to the Brexit process to grant Britain, with the French said to be pushing for a shorter deadline. Here’s how the process for agreeing on a delay actually works, and, with the U.K. seemingly heading toward a general election, here’s how that could unfold.

- Watch payment firms after PayPal surged in extended trading following an earnings beat. Watch the likes of Adyen, Wirecard and Worldline.

COMMENT:

- “Uncertainties abound and are accumulating: Brexit delays, trade tensions, recession chatter, impeachment escalation, oil-market disruptions, and geopolitical risks,” Citi strategist Catherine Mann writes in a note. “Although domestic resilience has been the bulwark countering slowing trade growth, pervasive and accumulating uncertainties weigh on confidence and business decision-making.”

NOTES FROM THE SELL SIDE:

- Dialog Semiconductor’s 3Q revenue and profit beat estimates and indicates better-than-expected smartphone demand, RBC (sector perform) writes in a note.

- Deutsche Telekom’s quality may “prevail over time,” but with nearer-term issues such as merger and integration of Sprintwith T-Mobile US, Citi cuts its rating on the German phone company to neutral.

- Europcar’s 3Q results were “very weak,” with Ebitda excluding mobility down 8% y/y, while co. reduced 2019 guidance by 16%-19%, Citi says in note.

COMPANY NEWS AND M&A:

- Daimler Cuts Trucks Guidance, Says Provisions May Not Suffice(2)

- Nokia Cuts Earnings Outlook and Pauses Dividend to Invest in 5G

- BASF Confirms Outlook as China-U.S. Trade War Weighs (1)

- AstraZeneca Third Quarter Core EPS Beats Estimates

- Schneider 3Q Rev. EU6.65B, Up 4.2%; Confirms FY Target

- RBS Third Quarter Pretax Oper Loss GBP8 Mln

- Atos 3Q Rev. Rises 1.8% to EU2.77B; Confirms 2019 Objectives

- STMicro 3Q Rev. Beats Est.; Sees FY Rev. at Mid-Point Abt $9.48b

- Hermes 3Q Sales Beat Estimates, Rising 15% Ex-Currency Shifts

- Dassault Systemes Raises Full-Year Non-IFRS EPS Target

- Air Liquide 3Q Sales Rise 3.5%; Expects FY Net Profit Growth

- Nordea Targets 60%-70% Dividend Payout Ratio From 2020

- DNB Third Quarter Net Income 2.0% Above Estimates

- Equinor Third Quarter Adjusted Net Beats Estimates

- Wacker Chemie Cuts FY Sales, Ebitda Guidance (1)

- Metro Fiscal Year Sales Rise 1.5%; Confirms Earnings Forecast

- Norwegian Air Bolsters Cash With Long-Awaited Jet-Lease Venture

- Salini CEO Sees Record Year With Over EU20B of Potential Orders

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 395.1 (July high); 397.9 (June 2018 high)

- Support at 384.3 (50-DMA); 379 (200-DMA); 365.5 (50% Fibo)

- RSI: 61

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,636 (February 2018 high); 3,687 (January 2018 high)

- Support at 3,519 (76.4% Fibo); 3,482 (50-DMA); 3,403 (61.8% Fibo)

- RSI: 62.4

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- ABB raised to buy at SEB Equities; PT 23.60 Swiss francs

- Kungsleden raised to buy at Handelsbanken; PT 95 kronor

- Secure Income raised to buy at Panmure Gordon; PT 470 pence

- Whitbread raised to market perform at Bernstein; PT 4,000 pence

DOWNGRADES:

- Big Yellow Group cut to hold at Panmure Gordon; PT 1,171 pence

- Bonava cut to hold at ABG; PT 110 kronor

- Bonava cut to hold at Handelsbanken; PT 108 kronor

- Brunel cut to hold at ABN Amro Bank

- Deutsche Telekom cut to neutral at Citi

- Ingenico Group cut to hold at HSBC; PT 95 euros

- Remy Cointreau cut to equal-weight at Morgan Stanley

- Ringkjobing Landbobank cut to sell at ABG; PT 445 kroner

- Segro cut to hold at Panmure Gordon; PT 875 pence

- Technotrans cut to hold at Bankhaus Lampe

- Telia cut to underweight at JPMorgan; PT 38 kronor

- Unite Group cut to hold at Panmure Gordon; PT 1,210 pence

INITIATIONS:

- Prosegur Cash rated new buy at Mirabaud Securities

- Swedish Match reinstated buy at ABG; PT 510 kronor

MARKETS:

- MSCI Asia Pacific down 0.1%, Nikkei 225 up 0.6%

- S&P 500 up 0.3%, Dow up 0.2%, Nasdaq up 0.2%

- Euro up 0.03% at $1.1133

- Dollar Index down 0.03% at 97.46

- Yen up 0.07% at 108.61

- Brent down 0.5% at $60.9/bbl, WTI down 0.8% to $55.6/bbl

- LME 3m Copper down 0.2% at $5870.5/MT

- Gold spot up 0.1% at $1492.9/oz

- US 10Yr yield down 1bps at 1.75%

ECONOMIC DATA (All times CET):

- 9am: (SP) 3Q Unemployment Rate, est. 13.75%, prior 14.02%

- 9:15am: (FR) Oct. Markit France Manufacturing PMI, est. 50.2, prior 50.1

- 9:15am: (FR) Oct. Markit France Services PMI, est. 51.6, prior 51.1

- 9:15am: (FR) Oct. Markit France Composite PMI, est. 51, prior 50.8

- 9:30am: (GE) Oct. Markit/BME Germany Manufacturing PMI, est. 42, prior 41.7

- 9:30am: (GE) Oct. Markit Germany Services PMI, est. 52, prior 51.4

- 9:30am: (GE) Oct. Markit/BME Germany Composite PMI, est. 48.8, prior 48.5

- 10am: (EC) Oct. Markit Eurozone Manufacturing PMI, est. 46, prior 45.7

- 10am: (EC) Oct. Markit Eurozone Services PMI, est. 51.9, prior 51.6

- 10am: (EC) Oct. Markit Eurozone Composite PMI, est. 50.3, prior 50.1

- 10:30am: (UK) Sept. UK Finance Loans for Housing, est. 42,350, prior 42,576

- 1:45pm: (EC) Oct. ECB Main Refinancing Rate, est. 0.0%, prior 0.0%

- 1:45pm: (EC) Oct. ECB Marginal Lending Facility, est. 0.25%, prior 0.25%

- 1:45pm: (EC) Oct. ECB Deposit Facility Rate, est. -0.5%, prior -0.5%

--With assistance from Ksenia Galouchko, Jan-Patrick Barnert and Macarena Munoz.

To contact the reporter on this story: Michael Msika in London at mmsika4@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Jon Menon

©2019 Bloomberg L.P.