Wall Street Puts Blame on Calabria for Blocking Mortgage Aid

Wall Street Heaps Blame on Calabria as Roadblock to Mortgage Aid

(Bloomberg) -- With the coronavirus crisis crushing the real-estate market, some on Wall Street are assailing a U.S. official who they blame for blocking a government bailout of mortgage lenders.

That man isn’t Treasury Secretary Steven Mnuchin or Federal Reserve Chairman Jerome Powell, who are leading Washington’s effort to rescue the economy. Rather, the target of ire is Federal Housing Finance Agency Director Mark Calabria, a libertarian economist whose job is regulating mortgage giants Fannie Mae and Freddie Mac.

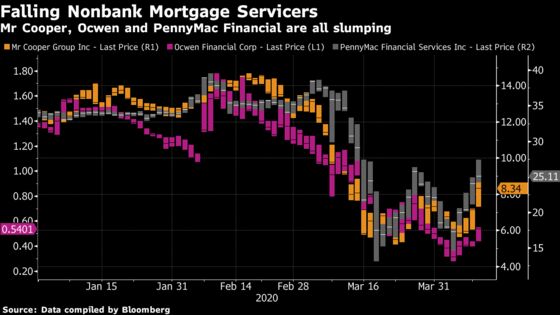

At issue is whether the U.S. should step in now to save nonbank mortgage servicers, firms including Quicken Loans, Freedom Mortgage and Mr Cooper Group Inc. that collect payments from borrowers and make sure investors in trillions of dollars of government-backed bonds get paid each month. With millions of homeowners predicted to start missing payments, the industry says it needs an immediate lifeline to head off servicer failures that could trigger nothing less than the collapse of the housing market.

Calabria argues that’s hyperbole. He’s refused to let government-controlled Fannie and Freddie provide support for servicers because he says there are more pressing uses of their limited capital to help bondholders and borrowers. His stance has made him a target of criticism for trade groups such as the Mortgage Bankers Association and some financial analysts.

“The president should fire Mark Calabria,” Chris Whalen, a New York-based bank analyst at Whalen Global Advisers, said in an interview. “He is taking a childish, naive approach right now that is bordering on negligence,” added Whalen, who says he’s been fielding phone calls from financial executives complaining about the FHFA leader.

Calabria counters that he’s not seen any data so far on borrower forbearance that indicates servicers need emergency government funds. For now, Treasury and Fed officials seem to agree because they’ve also declined to orchestrate a rescue.

“Nothing we are seeing as of today suggests that this is a systemic problem,” Calabria said in an interview. “What we are seeing suggests that for the next couple of months, this is sustainable.”

Calabria, who previously worked for Vice President Mike Pence, is a devoted small-government Republican with long-held opinions that Washington shouldn’t bail out every stumbling company or industry. A stark case in point: He’s repeatedly said that if it were up to him, Fannie and Freddie would have been allowed to fail during the 2008 financial crisis. The firms stand behind half of the nation’s $10 trillion residential mortgage market.

Personal Politics

Whalen and others who fault Calabria say he’s putting personal politics ahead of doing what’s necessary to get through the pandemic. A common gripe is that Calabria is obsessed with achieving a Trump administration goal of releasing Fannie and Freddie from the government’s grip, so he doesn’t want the companies to extend what little capital they have to prop up mortgage servicers.

Calabria disputes both points, saying his decisions aren’t being guided by his politics or mortgage-finance reform. Still, it seems inevitable that the virus will impact any plans the administration has to free Fannie and Freddie.

“Any steps that are taken now, there will be policy implications when we’re past this crisis,” said Chris Campbell, a former Treasury official under Mnuchin who is now at investment advisory firm Duff & Phelps. “It certainly complicates and limits options available for reform that many people in the administration believe is necessary.”

Industry Rebukes

To be sure, it’s not up to just Calabria whether mortgage servicers receive a bailout. That’s because the Fed and Treasury don’t need his sign-off to start a lending facility.

But Calabria’s outspokenness has made him the brunt of industry rebukes. The Washington-based Mortgage Bankers Association, which lobbies on behalf of nonbank servicers and other lenders, blasted him in a press release last week after he said he hadn’t yet seen forbearance requests that were so alarming as to warrant a Fed rescue.

“The FHFA Director’s recent statements send a troubling message to borrowers, lenders, and the mortgage market,” MBA President Robert Broeksmit said in the April 7 statement. “Director Calabria should advocate for the creation of a liquidity facility at the Fed to ensure the stability of the housing finance market.”

Another trade group, the Structured Finance Association, said FHFA’s reluctance to step in has “perpetuated market uncertainty.”

“It would be disruptive and unfair for FHFA to expect private industry to bear the entire burden of government actions to protect American homeowners,” Michael Bright, the group’s president, said in an April 8 statement. “This is not 2008. This is not a bailout for an industry that has acted irresponsibly.”

Fed Watching

The Fed is “watching carefully the situation with the mortgage servicers,” Chairman Powell said Thursday during a webcast hosted by the Brookings Institution. Mnuchin told reporters Monday that Treasury is very aware of the issues confronting servicers and that it’s “going to make sure that the market functions properly.”

Calabria does acknowledge that the outlook for some servicers is grim. That’s because as part of the $2 trillion stimulus bill that Congress passed in March, lawmakers mandated that borrowers be allowed to delay payments on government-backed mortgages for as long as a year.

When homeowners go into forbearance, servicers must still advance payments to mortgage-bond investors. They will eventually be reimbursed by federal agencies or by Fannie and Freddie, but can face cash crunches while waiting. The issue could be especially acute for nonbank servicers, which don’t have deposits or other sources of liquidity that banks do.

The number of Fannie and Freddie loans in forbearance rose to 2.44% during the week ended April 5, up from 1.7% the previous week, according to the MBA. Roughly 3.7% of all mortgages are in forbearance.

A Quicken spokesman said the company neither needs government help nor is asking for it.

Taxpayer Rescue

Fannie and Freddie keep the mortgage market humming by buying loans from lenders and packaging them into securities that the companies guarantee. The housing collapse more than a decade ago prompted the government to take Fannie and Freddie over and eventually inject them with more than $187 billion of taxpayer funds. They’ve since returned to profitability.

Calabria has directed Fannie and Freddie to begin building up their capital buffers so they can endure losses, and thus survive as private companies. As a result, the companies have stopped sending their profits to the Treasury and instead started retaining earnings.

Fannie had $14.6 billion in capital at the end of 2019, while Freddie had $9.1 billion. Tapping those cushions wouldn’t alleviate all the problems facing servicers but it could help, according to industry analysts.

“Of course they need to step in now,” Jim Parrott, a former Obama administration official who is a consultant for mortgage companies, said of Fannie and Freddie. “If you’re not willing to allow the GSEs to step in when the private market flees and liquidly freezes, then why have government sponsored enterprises at all?”

Ginnie’s Lifeline

Ginnie Mae announced last month that it would advance payments to bondholders to help servicers that handle mortgages made through programs offered by the Federal Housing Administration and the Department of Veterans Affairs. Ginnie, which is part of the Department of Housing and Urban Development, guarantees loans that are popular with first-time homebuyers and lower-income borrowers.

A key reason the Fed and Treasury have held off on extending support to a wider group of servicers is that federal officials have discussed waiting to see how much Ginnie’s decision relieves mortgage-market stress, according to people familiar with the matter.

Former Fannie Chief Executive Officer Tim Mayopoulos said the cautious approach stems partly from the fact that nonbank lenders are so-called shadow banks that aren’t regulated by the Fed.

“There is a inherent reluctance on the part of regulators to extend their regulatory benefits to non-regulated institutions without all the other regulatory oversight that comes with that,” he said. “But I would be surprised if policy makers don’t eventually find some sensible solution to this because otherwise they are at risk of seeing all the other remarkable efforts they’ve made so far come to naught.”

Fighting Regulation

Another reason servicers aren’t beloved in Washington: The companies spent years lobbying against tougher oversight and stricter capital requirements.

The hesitancy to rescue the industry may foreshadow future fights. For example, private mortgage insurers could rack up losses and come under stress as the pandemic persists. That threatens to make them ineligible to insure Fannie and Freddie loans. If that happens, Calabria would face another tough decision over whether to step in.

“The question is whether and how much the government will use Fannie and Freddie to be a source of support,” Former Freddie CEO Don Layton said. “That’s going to continue to be the case as this goes on.”

©2020 Bloomberg L.P.