Wall Street Frets Over a Revived CFPB Trump Left Toothless

Wall Street Frets Over a Revival of CFPB Left Toothless by Trump

(Bloomberg) -- The Trump administration has done its best to neuter the Consumer Financial Protection Bureau, giving large banks a reprieve from aggressive enforcement and new rules. With Joe Biden ascending to the White House, Wall Street is worried it will be quickly resurrected.

Thanks to a U.S. Supreme Court decision earlier this year, Biden will be able to fire Kathy Kraninger, the watchdog’s Republican director, even though her term isn’t complete -- a move likely to happen in the weeks after the inauguration. The banking industry has reason to fear that a new chief will return the agency to its days of meting out stiff sanctions on lenders and credit card companies.

“Banks should be prepared for more aggressive enforcement and an expansion of the CFPB’s authority through its rulemakings,” said Rachel Rodman, a former CFPB lawyer who now represents banks as a partner at Cadwalader, Wickersham & Taft LLP in Washington. She expects the agency to be “more likely to bring an enforcement action, pursue novel legal theories and more likely to demand higher penalties.”

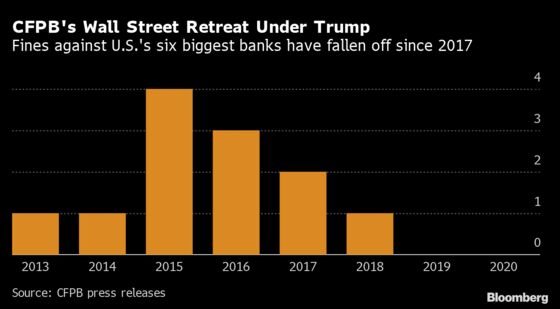

The regulator’s shift under President Donald Trump has been stunning. Since his appointees took over the CFPB in late 2017 it has imposed just a single fine on one of the nation’s six largest banks -- a $500 million penalty against scandal-ridden Wells Fargo & Co. for allegedly overcharging auto lending and mortgage customers. When Barack Obama’s director ran the CFPB, it routinely punished mega-banks.

Biden’s short-list of potential CFPB leaders, according to people familiar with the matter, includes Federal Trade Commission member Rohit Chopra and Representative Katie Porter, a California Democrat known for sparring with JPMorgan Chase & Co. Chief Executive Officer Jamie Dimon and other top bankers at tense congressional hearings. Both Chopra and Porter are supported by progressive Democrats and are acolytes of Senator Elizabeth Warren, who conceived of the CFPB and is determined to bring it out of its slumber.

A spokesman for the Biden transition didn’t respond to a request for comment.

Consequential Choice

The choice of who will run the CFPB is consequential since the watchdog was set up to avoid much of the political infighting that lobbyists often exploit to slow down policy changes and investigations. Unlike most federal agencies, the CFPB is run by a single director who not only controls the regulator’s agenda but also can set its budget without congressional approval.

That expansive power is what Democrats and consumer advocates are counting on to bring tough oversight to the financial industry, including mortgage lending, credit cards and bank overdraft charges. They also see the agency as playing a central role in the Biden administration’s efforts to tackle the nation’s economic troubles brought on by coronavirus: monitoring federal aid programs, helping to stem foreclosures and ensuring fair loan terms for small businesses on the verge of collapse.

“The CFPB has so many tools that it isn’t using right now,” said Linda Jun, senior policy counsel at Americans for Financial Reform, a non-profit coalition that includes consumer, investor and labor groups. “If you get the right leadership in place, there is a lot that can be turned around.”

Supporters say one immediate area for a revamp is the CFPB’s supervision and enforcement program, which has endured a staff exodus. Even the Wells Fargo settlement, its most prominent case in the Trump era, seemed a reaction to the president. It was wrapped up after he personally tweeted that the sanctions would be “severe.”

Mulvaney’s Pledge

The CFPB was created as part of the 2010 Dodd-Frank Act. Its job overseeing the parts of the financial industry that interact with regular people proved popular with many Americans. But the bureau also became one of the most politically contentious aspects of the financial crisis-era law.

The Trump administration was determined to end what it saw as years of Democratic over-regulation and activism at the CFPB. After former Congressman Mick Mulvaney became the first Republican to run the CFPB in November 2017, he declared: “The days of aggressively pushing the envelope are over.”

Through early November of this year, the CFPB had collected about $1.4 billion in fines and consumer redress since Kraninger took over as director in December 2018, according to a Bloomberg Law analysis of enforcement actions. Many of the cases involved small mortgage firms and payday lenders.

In the roughly six years that Obama’s CFPB chief Richard Cordray led the agency, the industry paid $12 billion in fines and consumer redress, with Wells Fargo, JPMorgan, Citigroup Inc. and Bank of America Corp. among banks that were penalized.

Big banks “frankly should be nervous,” said Rick Fischer, a senior partner at Morrison & Foerster in Washington who represents financial service firms on CFPB matters. “They recognize what life was like under Cordray and they recognize the size of his civil penalties.”

CFPB Spokeswoman Marisol Garibay said the bureau is “vigorously using enforcement to protect American consumers” and is on pace this year to bring the second-highest number of actions in its history. They include a $122 million settlement in August with TD Bank over improper overdraft charges, as well as cases involving debt collectors, mortgage servicers and student lending.

“These actions include settlements that have resulted in consumer redress, penalties and consumer debt forgiveness in the hundreds of millions of dollars spanning all of the markets policed by the bureau and involving institutions of all sizes,” Garibay said in an email.

Tough Confirmation

Democrats acknowledge that the partisanship enveloping the CFPB will likely make confirming a director difficult, especially if Republicans keep control of the Senate after next month’s runoff elections in Georgia. The focus on appointing a progressive leader will also heat up the battle.

Despite coming up with the idea for the agency and helping Obama set it up, Warren herself was unable to get enough support to win the CFPB director job in 2011. She instead returned to Massachusetts where she successfully ran for the Senate.

One solution to the potential logjam that the Biden transition team has been discussing, people familiar with the matter said, is to have the FTC’s Chopra run the agency on an acting basis. A federal law often used by Trump for temporarily filling vacancies of Senate-confirmed positions would allow Chopra to keep his current job and hold the CFPB post for about 300 days. Chopra worked with Warren to launch the bureau in 2010 and was then appointed an assistant director, overseeing the agency’s efforts on student lending.

Porter, who Warren taught at Harvard Law School, is also a serious candidate, the people said. However, there is some concern on Biden’s transition team as well as among congressional Democrats that her Orange County seat could be won by a Republican if she leaves Congress. Democrats have only a slim majority in the House.

Another possible candidate, the people said, is Patrice Ficklin, who works at the CFPB and helped launch its fair lending office. She would be the first African American to lead the agency.

Democrats’ Agenda

The incoming Biden administration is likely to overturn a number of the Trump-era policies that the CFPB enacted under Mulvaney and Kraninger, Democrats say. One early, and easy, change is expected to be the agency’s description of itself, which the Trump administration revised to prioritize ferreting out overly burdensome regulations.

Another, observers say, would be to bring back a rule that cracked down on payday lenders that was championed by Cordray. Under Trump, the agency scrapped guidelines that required lenders to verify that borrowers have the means to pay back the high-interest loans.

Wall Street is also expecting the regulator to review the controversial, though lucrative, practice of overdraft fees. The charges generate some $12 billion for U.S. banks.

©2020 Bloomberg L.P.