U.K. Taxpayers Face £26 Billion Bill for Covid Loans, Panel Says

U.K. Taxpayers Face £26 Billion Bill for Covid Loans, Panel Says

(Bloomberg) -- U.K. taxpayers face a bill of as much as 26 billion pounds ($35 billion) to cover state-backed coronavirus loans that businesses are unable to repay or were fraudulently claimed, lawmakers warned.

Ministers prioritized speed of delivery “over all other aspects of value for money” when they rolled out a program of 100% guaranteed Bounce Back Loans to help small and medium-sized companies weather the pandemic, the House of Commons Public Accounts Committee said in a report published Wednesday.

“Rushing to get money out of the door after the fact didn’t allow for analysis of how many businesses needed this help, could benefit from it, or could repay it,” Meg Hillier, who chairs the cross-party panel, said in a statement. “Dropping the most basic checks was a huge issue that puts the taxpayer at risk to the tune of billions.”

The report marks the latest criticism of Chancellor of the Exchequer Rishi Sunak’s response to the resurgent pandemic. Opposition parties have already slammed him for being behind the curve after being forced into announcing major changes to Covid job support programs five times in six weeks. Sunak himself has acknowledged “deadweight costs” in some of his initiatives.

Even so, the U.K.’s economic measures have been held up by the International Monetary Fund as “one of the best examples of coordinated action we have seen globally.”

Criticism

The bounce back loans program was deployed in May in response to criticism that normally profitable small firms were struggling to access an existing 80% state-backed program because of caution by lenders.

The Department for Business, Energy and Industrial Strategy estimated in September that losses in the program through fraud and inability to repay would total between 35% and 60% of the amount lent.

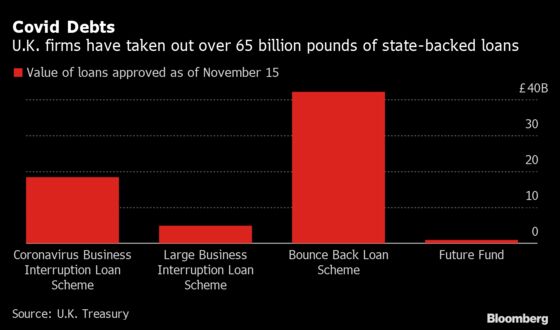

The most recent Treasury statistics show a total of 42.2 billion pounds has been lent under the program, suggesting losses would amount to at least 14.8 billion pounds and could stretch above 25 billion pounds.

The PAC attacked as “woefully under-developed” government plans for managing the risk to the taxpayer of non-repayment. It also said ministers lacked the data to be able to know how much of the losses would come through fraud, and how much through businesses that simply couldn’t repay the debt.

No Apology

The government said in a statement that it “won’t apologize” for targeting support at those who needed it “as quickly as possible,” and insisted steps are being taken to crack down on fraud.

The panel also:

- Commended the “impressive speed” at which the program was implemented, but said it “does not strike the right balance between supporting business and protecting the taxpayer”

- Said “no clear estimates” were made of the costs of not rolling it out so quickly

- Recommended that before embarking on future plans the Treasury “should be explicit on the level of losses it is likely to entail”

- Called on the Business Department to set out how it will attempt recovery and prosecution in instances where fraud has been committed

- Urged the Treasury to set out rules on loan recovery before the first repayments are due in May

©2020 Bloomberg L.P.