Bank of England Climate Tests Weigh Disorder in Stock Market

U.K. Insurers to Weigh Stock Market Disorder Caused by Climate

(Bloomberg) --

The Bank of England for the first time is asking British insurers to gauge how global warming might impact the value of the stocks and bonds they hold -- and its potential to upend financial markets.

The central bank, which regulates the U.K. financial services industry, included three scenarios related to climate change in a broader stress test of how robust the industry would be in times of strain. It’s asking for answers by Oct. 31.

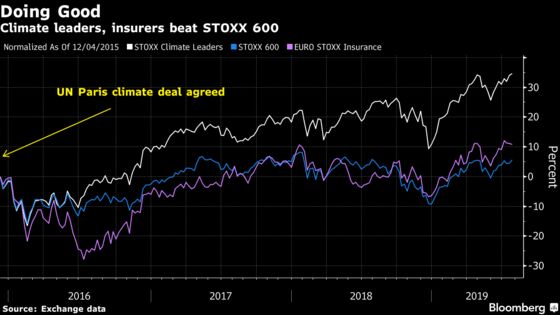

The exercise, which started in June, is part of a broader effort by BOE Governor Mark Carney to focus the attention of investors both on environmental issues and on how those are creating new risks for the financial system. After almost 200 nations backed the 2015 Paris Agreement on climate change agreeing limits on fossil fuel emissions, economies everywhere are adding regulations on pollution from coal and spurring investment in renewables such as wind and solar.

“What’s most interesting is the way the stress test will change the way the insurers will think about these particular sectors,” said Mark Lewis, global head of sustainability research at BNP Paribas SA’s asset management unit.

The three climate scenarios by the bank’s Prudential Regulation Authority are “exploratory” in nature. They “hypothetical narratives” are designed to “promote discussion on how business models and balance sheets may need to adapt, not about assessing current financial resilience,” it said in a guidelines document published on June 18.

- Under the most dramatic scenario, rapid global action to halt climate change results in a “disorderly transition.” It suggests “shock parameters” where the shares of oil companies plunge 42% in three years and coal users lose two-thirds of their value. Car makers would also suffer as traditional engines are scrapped in favor of electric vehicles.

- Another scenario envisions an orderly transition and warming in the atmosphere kept well below 2 degrees Celsius (3.6 degrees Fahrenheit) since pre-industrial levels. The economy would shift toward zero carbon emissions by 2050.

- A third outlook was for little tightening of environmental regulations, resulting in warming of 4 degrees by 2100 and more significant changes to the climate.

The assumptions set out by the PRA are “purposely non-exhaustive as the goal of this scenario analysis is investigatory in nature,” the regulator said. “The PRA recognizes that for different portfolios, the materiality of natural catastrophe perils and asset classes affected will differ.”

The exercise may prompt shareholders to see insurers as a more risky prospect, said David Lunsford, co-founder and head of development at Carbon Delta AG, which advises on climate risks and provided input to the PRA as it drew up its request.

“The interest of the PRA is to look at the most extreme scenarios,” he said. “While many people think insurers understand natural disasters enough to cope with climate change, the issue will “present many challenges. Some insurance companies might be more exposed than was expected before the tests.”

The scenarios chosen by the Bank of England are not necessarily expected outcomes. They reflect a “particularly abrupt change” and seem to take note of how markets work, Edwin Anderson, a partner at management consultant Oliver Wyman.

“Potential hits on short-term income could lead to large dips in equity value,” said Anderson, whose firm also fed into the PRA’s thinking. One of Anderson’s specialties is advising insurance regulators on risks within particularly complicated insurers.

Aviva Plc, an insurer, said it already has been assessing climate-related risks and promoting a better understanding of the issue within financial markets.

“Aviva recently published its Climate-Related Financial Disclosure which provides details of a Climate Value-at-Risk measure, relying on a range of climate warming scenarios, that we are developing to provide a holistic forward-looking view of climate-related transition and physical risks and opportunities to our business,” an official at the insurance company said in a statement.

Steven Findlay, head of prudential regulation at industry group the Association of British Insurers in London, welcomed the exercise.

“These are encouraging both firms and regulators alike to consider the climate change implications for insurers’ balance sheet, today and into the future, and how these should best be managed,” Findlay said. “We are looking forward to seeing the conclusions next year.”

Lewis at BNP said the scenarios might set off some deep thinking about how other investors will react to political developments on the environment in the months and years ahead.

“It becomes a sort of game-theory thing. Do you think Insurer X will sell? Do you think Insurer Y will sell?” Lewis said. “All of a sudden you are thinking I don’t want to be the last guy holding this stuff.”

The PRA doesn’t intend to disclose the results of the tests for individual insurers and it will publish a summary of the results in the first quarter of 2020.

“If a policymaker gives you a guideline as clear as this, it will change the way you think,” Lewis said. “Once you put something out there like this, the market starts to follow its own dynamic. This is a further example of the momentum increasing and accelerating and intensifying.”

--With assistance from Silla Brush and Will Hadfield.

To contact the reporters on this story: Mathew Carr in London at m.carr@bloomberg.net;Lisa Pham in London at lpham14@bloomberg.net

To contact the editors responsible for this story: Reed Landberg at landberg@bloomberg.net, Rob Verdonck

©2019 Bloomberg L.P.