ADVERTISEMENT

U.K. Bond Market Goes Into Vote Cautiously Relative to FX

U.K. Bond Market Goes Into Election Cautiously Relative to FX

12 Dec 2019, 12:36 PM IST

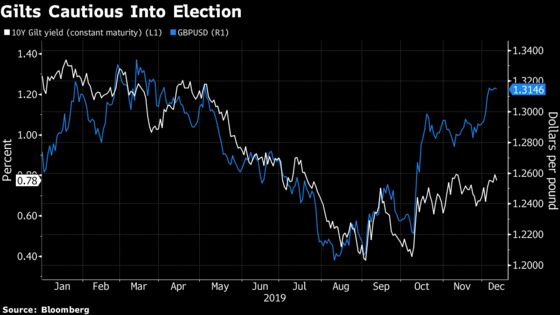

(Bloomberg) -- The bond market has lagged the recent optimism for a Conservative majority seen in the sharp move higher in the pound. Still, if Prime Minister Boris Johnson does indeed win on Thursday then a sell-off across the curve should only be mild.

The cautious approach of gilts into the election leaves the 10-year yield trading at the top of recent ranges. Volatility isn’t pricing a particularly pronounced move following the election, with the curve potentially shifting initially higher by around 10 basis points.

- Implied volatility on the 10-year swap rate is suggesting a potential range of around 25bps over the next three months, which doesn’t appear unreasonable relative to the Brexit premium and macro picture.

- Over the next year, implied volatility on the 10-year swap implies a 68% chance of yields trading between 0.65% and 1.30% versus current spot rate of 0.97%.

- The Sonia curve seems reasonably in-line with the potential weighted election outcomes, with BOE on hold in the case of a Conservative majority, and uncertainty over the Brexit transition period versus potential easing with a hung Parliament; January 2020 MPC-dated OIS prices 6bps of cuts and December 2020 12bps.

- Betting markets are pricing an outright Tory majority but the margin of error on polling models are large. Assuming a stable majority is achieved and the withdrawal agreement is signed off by Parliament, the outcome of the transition period remains unknown and poses risk of renewed downward pressure on GBP assets into the July 1 2020 transition period extension deadline.

- One of the main losers on the unwind of no-deal Brexit risk has been the front-end of the inflation markets. A Conservative majority should see further steepening of the RPI curve as the front-end has room to move toward realized prints, conditional on the pound remaining supported, while a hung Parliament likely will see some unwind.

- The Brexit effect decreases further out the inflation curve where the RPI reform will impact; the market appears reluctant to price the RPI to CPIH conversion and it remains uncertain.

- Selling GBP rate volatility has been a profitable trade this year, taking advantage of the Brexit-uncertainty premium and subsequent low realized volatility.

- As always around such event risks where forecasts -- which carry a high margin of error -- skew markets, assess payoff functions and be nimble around any extremes.

- Post-election option structures to consider include 1x2 payer spreads in the belly for a limited sell-off in 1H 2020 (which is short-volatility and initially long-duration) or conditional bull-steepeners if uncertainty prevails.

- NOTE: Tanvir Sandhu is a global fixed income and derivatives strategist who writes for Bloomberg. The observations he makes are his own and are not intended as investment advice.

To contact the reporter on this story: Tanvir Sandhu in London at tsandhu17@bloomberg.net

To contact the editors responsible for this story: Paul Dobson at pdobson2@bloomberg.net, William Shaw, Anil Varma

©2019 Bloomberg L.P.