Turkey Stealth Tightening Sets Back Clock on Rate Simplification

Turkey Stealth Tightening Sets Back Clock on Rate Simplification

(Bloomberg) --

The monetary-policy framework that confounded investors in Turkey for years is making a comeback.

Torn between market pressure to raise borrowing costs and President Recep Tayyip Erdogan’s persistent calls to lower them, Turkey’s central bank is trying to keep everyone happy by finding a backdoor to increasing the cost of money.

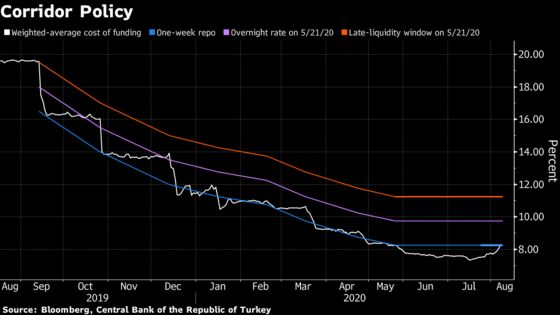

The vehicle it’s using is the interest-rate corridor. Rather than changing the main one-week repo at its monthly meetings, the central bank now tweaks the cost of funding on a daily basis, modifying the amount of liquidity available to lenders across its various interest rates.

To traders’ dismay, the regulator appears to have ditched a 2018 decision to focus on a single benchmark rate. The move was lauded at the time as a “simplification” of Turkey’s monetary regime, and a step toward making policy more predictable.

The pivot back began on Friday, when the central bank stopped funding the market using the benchmark repo, which it’s held at 8.25% since May. By Wednesday, it will have also eliminated a discount available to primary dealers, pushing the cost of marginal funding to 9.75%, the rate charged for using its so-called overnight window.

On Tuesday, the lira appeared to be benefiting from the prospect of tighter monetary conditions, swinging back from a loss to trade as much a 1% stronger against the dollar. It was set for the first increase in five days.

The advantage of running policy like this is that the central bank can effectively raise funding rates to as high as 11.25% -- the very top end of its corridor -- without making any changes at a monetary policy meeting. And more importantly, without evoking a political backlash.

The problem for investors is that this policy lacks transparency. What looks like tightening today can be reversed tomorrow with little notice or explanation. It’s also reminiscent of the approach in 2018, when it resisted raising benchmark rates for months.

That wasn’t enough to calm investors demanding higher rates to hold the nation’s assets, and the central bank was eventually forced into a large outright rate increase. By then, the lira had already tumbled to a record low in one of its sharpest depreciations on record.

©2020 Bloomberg L.P.