Treasury Seeks to Quell Fears Crypto Tax Rules Are Overly Broad

Treasury Seeks to Quell Fears Crypto Tax Rules Are Overly Broad

(Bloomberg) -- The U.S. Treasury Department is set to clarify that only cryptocurrency companies it considers brokers will need to comply with proposed IRS reporting requirements, aiming to quell concerns over a provision in the bipartisan infrastructure bill passed by the Senate.

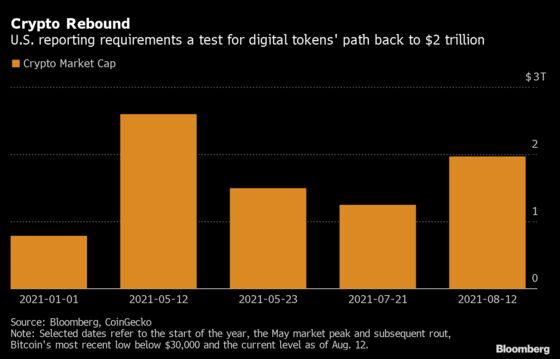

Other firms key to the nearly $2 trillion crypto market -- from developers and miners to hardware and software providers -- won’t have any new requirements, so long as they don’t also act as brokers, according to a Treasury official. The Treasury’s guidance won’t grant blanket exemptions based on how firms identify themselves and instead will focus on whether a firm’s activities qualify it as a broker under the tax code, the official said on condition of anonymity to discuss internal deliberations.

The guidance, which could be made public as soon as next week, is an attempt to address concerns in the cryptocurrency industry that the $550 billion infrastructure bill would require a host of companies with ties to digital assets to report data to the Internal Revenue Service that they don’t have. The tax provision, estimated to raise $28 billion over a decade, was included in the legislation as a way to help pay for new investments in roads and bridges.

The Treasury’s directive is crucial because lawmakers who want to revise the bill’s language in the House are unlikely to succeed, since altering the crypto section could open up the whole legislation to additional revisions. House Speaker Nancy Pelosi has said she’ll bring up the bill for a vote when President Joe Biden’s $3.5 trillion social spending and tax plan is also ready for consideration, which could be months from now.

The Senate-passed bill has caused significant heartburn in the cryptocurrency world, with participants saying Congress doesn’t understand the technology well enough to regulate it.

| Read more: |

|---|

|

Senator Rob Portman, the Ohio Republican who drafted that portion of the bill, said on the Senate floor after days of debate over the issue that he thinks the legislation is clear, but added that that miners, entities who validate transactions and software developers for digital wallets should not be subject to the new tax rules.

Crypto industry players and advocates objected to what they called overly vague language, worrying it could subject too many companies to burdensome reporting requirements. The proposed law would expand the definition of broker in the tax code to include anyone “regularly providing any service effectuating transfers of digital assets.”

A bipartisan group of senators sought to pass a last-minute amendment to more narrowly target the new rules, but it was ultimately blocked with procedural moves.

The Treasury official said some of the industry’s concerns were valid but that much of the lobbying was aimed at limiting the Treasury Department’s authority to collect legitimate tax information. The department isn’t looking to go after businesses who don’t have transaction data, the official said.

The Treasury guidance would give more clarity about how it would apply the definition of a broker to entities that transfer digital assets on behalf of another person. The number of companies ultimately affected by the new reporting rules will depend on how aggressively the IRS implements the Treasury guidance.

The effort is also part of a broader push by the Treasury Department to crack down on tax cheats. IRS Commissioner Chuck Rettig has said tax evasion through the use of virtual currency is a key contributor to the growing gap between what’s owed in taxes and what the IRS actually collects.

In addition, more regulation is likely coming for the cryptocurrency community with prominent lawmakers, including Senator Elizabeth Warren, and regulators like Securities and Exchange Commission Chairman Gary Gensler both eager to address the emerging technology.

Settling Down

Some of the industry’s worst fears over the Senate bill may prove overblown.

“I don’t think people will notice much. Did everything die in crypto in the U.S. when Coinbase began 1099s a few years ago?” William Quigley, the co-founder of stablecoin Tether and blockchain platform WAX, referring to when the largest cryptocurrency exchange began issuing IRS forms in 2017.

“Those worries, though, I think have started to settle down a bit,” he said. “I think the IRS is going to take note of what the intent was that was expressed by these senators.”

The new reporting rules, if signed into law, won’t go into effect until 2023, giving the government and cryptocurrency companies time to update their systems to send the data prescribed in the law. It also gives the industry time to ramp up lobbying efforts.

“The crypto community got a strong wakeup call that it needs to highlight the benefits rather than let Washington dictate top-down,” said James Creech, a tax attorney who specializes in crypto. “Once you get identified as the source of the tax gap, you also get identified as something that needs to be cracked down upon.”

©2021 Bloomberg L.P.