Brexit Isn’t Done Yet, But We May Get There: Taking Stock

Brexit Isn’t Done Yet, But We May Get There: Taking Stock

(Bloomberg) -- The job isn’t done yet. The British Parliament decided to extend what markets hate most: uncertainty. What’s next? Likely a delay, even if U.K. Prime Minister Boris Johnson’s vowed to leave by Oct. 31. Johnson will on Monday ask the House of Commons to support his deal a new “meaningful vote.” It’s going to be a long week, but judging by the contained reaction of the pound and the flat FTSE 100 futures this morning, the market is pricing some hope of a resolution in the coming days.

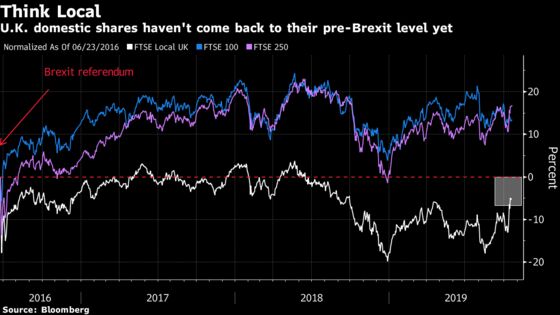

U.K. domestic-oriented stocks are first in line. They have surged over the past six sessions, and had been tipped to outperform if the deal would have been approved over the weekend. Looking at the chart below, they still have plenty of room on the upside before returning to their pre-Brexit referendum level. Morgan Stanley strategists write that a reduction in Brexit uncertainty should lead to a re-rating in U.K. stocks as the market becomes “investable again.” While U.K. mid-caps offer 10% upside, small caps offer an even better risk-reward as they trade at 10-year valuation lows relative to mid-caps, the strategists write.

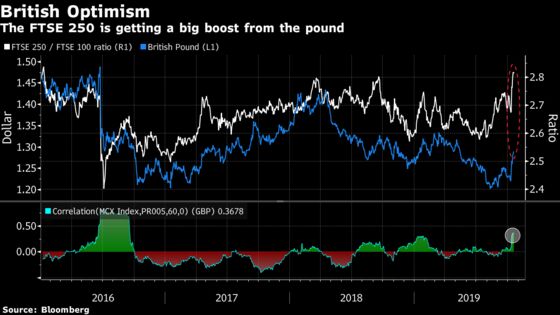

The FTSE 100 and 250 have performed closely in line over the past months, but the recent surge in the pound has boosted the mid-cap FTSE 250 while holding back the exporters-heavy FTSE 100. The former’s relative performance is at its highest correlation with the pound since September 2016.

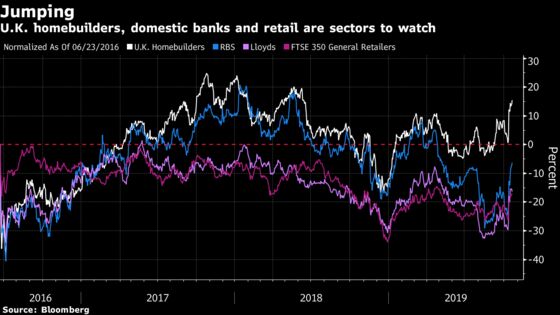

Digging deeper, domestic banks, housebuilders and retailers are key sectors to consider this week. Shares of U.K. high-street lenders have been among the hardest hit by Brexit uncertainty.

RBS, which Bloomberg Intelligence’s Jonathan Tyce calls the poster child for no-deal risk fears, as well as Lloyds, have rallied strongly in recent sessions but remain about 5% and 15% from their pre-Brexit referendum levels respectively.

British housebuilders have also been under pressure amid Brexit uncertainty and Morgan Stanley predicted last month that the group could gain 20% if a deal was reached, or drop 18% in a no-deal scenario. Those with big exposure to London, like Crest Nicholson and Taylor Wimpey, have been hit the hardest, still down 26% and 13% respectively since the referendum. HSBC analysts said earlier this month Taylor Wimpey is best placed to gain from a post-Brexit market bounce back.

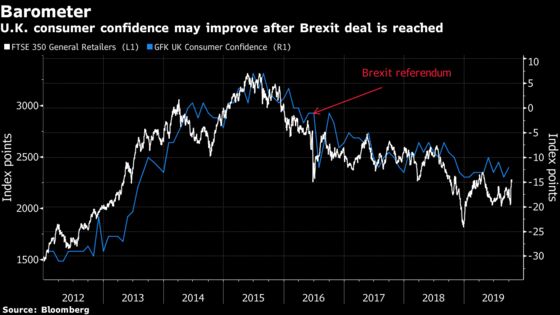

U.K. retailers too have suffered. The FTSE 350 General Retailers Index is still down about 17% since the referendum. Dispersing Brexit clouds may help improve consumer confidence, a strong barometer for the retail sector. Gains in the pound may help supermarkets in particular, such as Marks & Spencer, Sainsbury’s and Tesco.

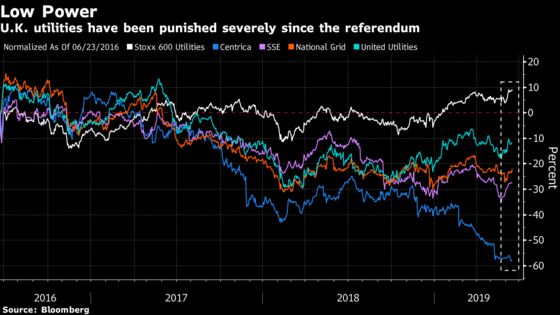

In the event of an U.K. general election, caution might be required for utilities and other stocks likely to be targeted by a potential Labour government. Jeremy Corbyn has vowed to nationalize swathes of Britain’s water and energy firms, along with the railways and postal group Royal Mail.

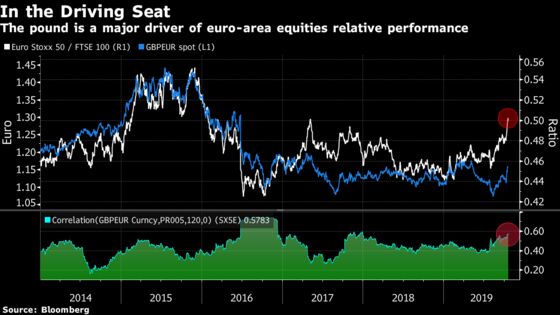

Outside of domestic-oriented U.K. shares, euro-area equities could also be a major beneficiary to a vote in favor of the deal this week. The soaring pound has been a key driver of the Euro Stoxx 50 outperformance, with correlation back near 2017 highs.

No matter what happens at the end, multinational groups listed on the FTSE 100 are set to track the pound, with the benchmark rallying if sterling drops and vice versa. FTSE 100 members derive more than 70% of their revenues from abroad. Diageo is one such stock to watch, with Jefferies analysts estimating that every 1% move in sterling against the dollar is worth about 0.5% of the beverage group’s EPS.

In the meantime, FTSE 100 futures are flat, Euro Stoxx 50 futures are up 0.1%, while S&P 500 contracts are up 0.2% ahead of the European open.

- Watch trade-sensitive equities after China’s top trade negotiator offered positive signals that talks between Washington and Beijing are progressing toward a partial trade deal.

- Watch German property owners after governing parties in Berlin struck a deal to freeze rents in the capital for five years. Watch Deutsche Wohnen, Berlin’s largest residential apartment owner, along with other German real estate names including Vonovia, TAG Immobilien, ADO Properties, Adler Real Estate, LEG Immobilien and Grand City Properties.

COMMENT:

- “We have been advocating a bullish equity stance, driven, among other factors, by the belief that the trade drag will ease and that one could see Brexit clarity as early as this month, with the risk of No-deal exit fading,” JPMorgan equity strategists write in a note. “We anticipate an inflection in PMI momentum and look for a continued bounce in bond yields. This is behind our recent reversal of preference for U.S. over Eurozone and the expectation that market leadership will broaden into cyclicals and Value style.”

NOTES FROM THE SELL SIDE:

- Sandvik is raised to buy from neutral at Citi after its 3Q earnings beat on Oct. 18. Citi says it’s stayed on sidelines, instead seeing Volvo as resilience top-pick. But broker now adds Sandvik to its “value-resilience camp”. Separately, SEB also raises Sandvik to buy.

COMPANY NEWS AND M&A:

- SAP Confirms 2019, Mid-Term Ambitions After 3Q Profit Increases

- Wirecard Commissions KPMG to Carry Out Independent Audit (1)

- Shell to Sell Egypt Assets in Western Desert to Focus on Gas

- Advent Nears Guarantees on Cobham Deal: Telegraph (Oct. 20)

- Telenor Grameenphone 3Q Revenue NOK3.84B vs NOK3.34B Year Ago

- Bawag to Start EU400 Million Buyback Offer for 11% of Stock (1)

- Sartorius Stedim Ups Sales View, Buys Parts of Danaher Life (2)

- Roche’s Tecentriq-Avastin Combo Shows Overall Survival Increase

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 395.1 (July high); 397.9 (June 2018 high)

- Support at 382.8 (50-DMA); 378.5 (200-DMA); 365.5 (50% Fibo)

- RSI: 57.2

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,636 (February 2018 high); 3,687 (January 2018 high)

- Support at 3,519 (76.4% Fibo); 3,466 (50-DMA); 3,403 (61.8% Fibo)

- RSI: 59.3

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- EDP raised to overweight at JPMorgan; PT 4 euros

- Getinge raised to hold at SEB Equities; PT 143 kronor

- Norma raised to outperform at MainFirst; PT 40 euros

- Pearson raised to hold at Deutsche Bank; PT 600 pence

- Sandvik raised to buy at Citi

- Sandvik raised to buy at SEB Equities; PT 190 kronor

- Yara raised to buy at Handelsbanken; PT 410 kroner

DOWNGRADES:

- Assa Abloy Cut to Sell at Pareto Securities; PT 220 kronor

- Bobst cut to underperform at MainFirst; PT 48 Swiss francs

- Danone cut to sector perform at RBC; PT 72 euros

- Deutsche Boerse cut to reduce at Oddo BHF; PT 130 euros

- Groupe Open cut to hold at Portzamparc; PT 12.10 euros

- ICADE cut to neutral at Invest Securities SA; PT 83.50 euros

- Julius Baer cut to neutral at Citi

- Kiadis Pharma cut to hold at Jefferies; PT 2.50 euros

- Kiadis Pharma cut to sell at KBC Securities; PT 3.50 euros

- Premier Oil cut to outperform at RBC; PT 125 pence

- Schaeffler cut to neutral at Oddo BHF; PT 8 euros

- Wirecard cut to neutral at MainFirst; PT 150 euros

- Yara cut to hold at Arctic Securities; PT 400 kroner

- Yara cut to sector underperform at Scotiabank; PT 320 kroner

INITIATIONS:

- HelloFresh Rated New Reduce at Kepler Cheuvreux

MARKETS:

- MSCI Asia Pacific down 0.3%, Nikkei 225 up 0.3%

- S&P 500 down 0.4%, Dow down 0.9%, Nasdaq down 0.8%

- Euro down 0.08% at $1.1158

- Dollar Index up 0.07% at 97.35

- Yen down 0.02% at 108.47

- Brent down 0.3% at $59.2/bbl, WTI down 0.2% to $53.7/bbl

- LME 3m Copper up 0.2% at $5820.5/MT

- Gold spot up 0.2% at $1492.4/oz

- US 10Yr yield little changed at 1.75%

ECONOMIC DATA (All times CET):

- 11am: (EC) 2018 Govt Debt/GDP Ratio, prior 85.1%

--With assistance from Kit Rees, Joe Easton and Erin Roman.

To contact the reporter on this story: Michael Msika in London at mmsika4@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Namitha Jagadeesh

©2019 Bloomberg L.P.