Powell's Patience Fails to Calm Trump Despite Stock Surge

President Donald Trump blasted the central bank on Friday for “mistakenly’’ raising interest rates.

(Bloomberg) --

Federal Reserve Chairman Jerome Powell has a mounting distraction as he tries to engineer a rare soft landing of the economy and extend a nearly record-long U.S. expansion: The man who installed him in the job wants no landing at all.

President Donald Trump blasted the central bank on Friday for “mistakenly’’ raising interest rates and for a “ridiculously timed’’ reduction in its balance sheet. To hear the president tweet it, the economy would have expanded faster last year and the stock market would be higher if not for the Fed. Apparently he wasn’t happy enough with the strongest growth since 2005 and the S&P 500 Index’s best quarter in a decade.

Trump’s remarks stood out because the Fed has already done what he requested over the past year: stop raising rates. With budget deficits ballooning and fiscal stimulus difficult to engineer with a divided Congress, the White House is now turning the screws on the Fed to open the monetary spigot in time to boost the economy going into the 2020 presidential election year.

Soft-landing the economy -- reining in growth with just enough rate hikes to forestall overheating but not trigger a recession -- was never going to be easy. Ken Matheny, senior economist at IHS Markit’s Macroeconomic Advisers, likens it to a unicorn because it’s so illusive. The Fed arguably has accomplished it only once, in 1994-95, and then it was aided by a productivity surge that stretched the expansion into 2001.

Trump’s criticism “doesn’t make the Fed’s job any easier,’’ Deutsche Bank Securities chief economist Peter Hooper said. “If there is any sense that the Fed is kowtowing to pressure from the administration, that’s a problem’’ because it calls into question the central bank’s political independence.

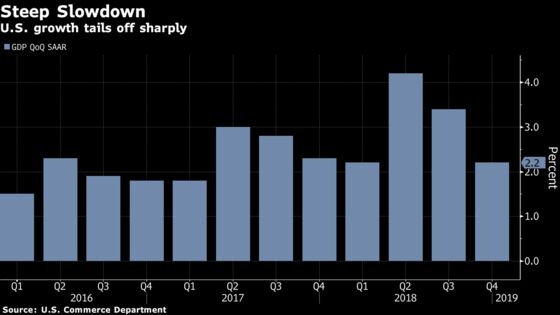

The Fed is vulnerable on two fronts. First, the economy is slowing sooner and more than the central bank expected, though Moody’s Analytics chief economist Mark Zandi said that’s partly because of Trump’s confrontational trade tactics. After downshifting to a 2.2 percent annualized pace in the fourth quarter from 3.4 percent in the third, growth is projected to have slowed further in the first quarter -- to 1.5 percent, according to economists’ forecasts compiled by Bloomberg. Activity was weighed down by the since-ended government shutdown and a wobbly global economy.

Secondly, inflation has failed to pick up as anticipated -- a development that Trump alluded to in his latest Twitter attack. The personal consumption expenditures price index, the Fed’s favorite inflation gauge, rose 1.4 percent in January from a year earlier and has not been sustainably above its 2 percent target since that objective was introduced in 2012.

In another potential pointer to a soft first quarter, U.S. retail sales unexpectedly eased in February on declines in grocery stores and building materials, which could potentially reflect cooler weather, though may also signal further headwinds for the economy.

The Fed has responded to lagging growth and inflation by abandoning plans to raise rates at all this year -- a surprise policy U-turn that sparked the first quarter’s stock-market surge. But the administration wants more.

Before Trump’s tweet on Friday, his senior economic adviser Larry Kudlow urged the Fed to reduce rates by a half percentage point. That followed a similar call from Stephen Moore, whom the president has said he will nominate to the Fed’s seven-member board. Those calls dovetail with financial-market expectations of a rate reduction.

The Fed is so far resisting the pressure. “It would be premature to contemplate a rate cut here,’’ St. Louis Fed President James Bullard, one of the most dovish officials, told reporters on Friday. “Most likely the economy will be stronger in the second quarter.’’

What Bloomberg’s Economists Say

“We think 1Q will mark the bottom for global growth this year. For the U.S., leaving aside the February jobs glitch, labor market remains tight. That will keep consumption -- the main engine of demand -- humming.”

-- Tom Orlik, chief economist

Click here for the full note.

Surprisingly quiescent inflation has enabled Trump officials to question the rationale behind the Fed’s soft-landing strategy. If inflation isn’t a problem, why slow growth down? That’s especially the case, they maintain, because the president’s tax cuts and deregulatory actions are boosting productivity and expanding the labor force, allowing the economy to grow faster without generating price pressures.

The Fed board’s two vice chairmen -- Richard Clarida and Randal Quarles, both of whom Trump appointed -- seem sympathetic to the argument that the economy has gotten a supply-side boost, though neither subscribe to anything like the administration’s claim of sustained 3 percent growth.

They also emphasize different parts of the economic equation. Clarida focuses on muted inflation and the need to ensure that expectations are anchored at the 2 percent target. Quarles zeros in on the potential for faster growth and the possibility that higher interest rates may be needed to keep the economy in equilibrium.

“Further increases in the policy rate may be necessary at some point, a stance I believe is consistent with my optimistic view of the economy’s growth potential and momentum,’’ Quarles said in a speech last week, while adding he was “very comfortable’’ with the Fed’s current patient stance in deciding its next move.

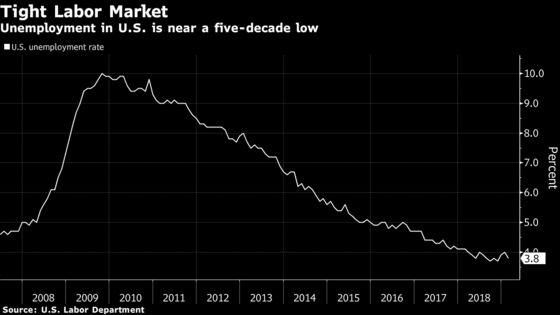

Fed and administration officials appear to agree that the economic fundamentals are solid. Consumers, whose spending accounts for more than two-thirds of gross domestic product. seem to be doing well, with wages rising thanks to a taut labor market and household wealth up due to surging share prices.

What’s worrying the Fed and the administration is weak foreign growth, especially in Europe.

Allianz SE chief economic adviser Mohamed El-Erian agrees Europe is a concern, but argues that won’t blow the U.S. expansion off course. “The only way you get a significant slowdown here is if you get a policy mistake,’’ said El-Erian, who is also a Bloomberg Opinion columnist.

But successfully engineering a soft landing and avoiding a recession are unlikely to satisfy Trump as he tries to take credit for a turbo-charged economy heading into the 2020 election.

Saying that he and the president “think a lot alike,’’ Fed nominee-to-be Moore told Bloomberg Television on March 22: “I really believe we could have 3 to 4 percent growth for another five or six years.”

--With assistance from Steve Matthews and Catarina Saraiva.

To contact the reporter on this story: Rich Miller in Washington at rmiller28@bloomberg.net

To contact the editors responsible for this story: Brendan Murray at brmurray@bloomberg.net, Scott Lanman

©2019 Bloomberg L.P.