Politics Still Matters for European Equity Markets

Politics Still Matters for European Equity Markets

(Bloomberg) --

After fretting over trade tensions, central bank policies and Brexit in recent weeks, investors now have something else to worry about: the European elections and the potential rise of populist parties across the region.

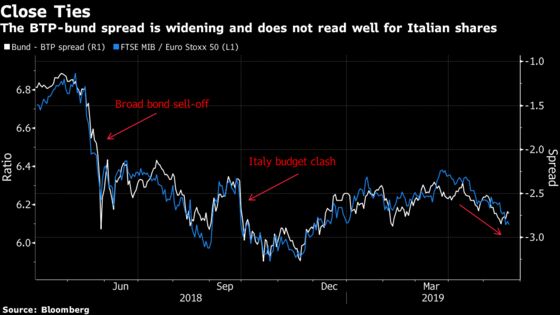

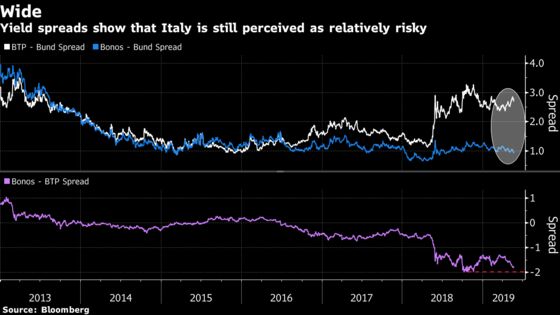

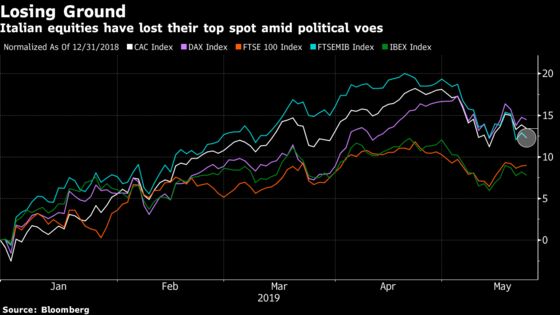

The results are particularly important in Italy, where the performance of the coalition parties could heavily influence budget talks with the EU. This spooked investors last year, triggering a sell-off in Italian bonds and equities.

“(Italian bonds) have started to discount a larger political and fiscal premium,” economists at Goldman Sachs write, adding that the deteriorating public finances, increasing fears of budget friction with the EU and potential credit rating downgrades are likely to weigh on Italian assets. Goldman has raised its short-term target for the BTP-Bund 10-year spread to 330bps and sees the FTSE MIB volatility as an attractive hedge for political risk.

The Italian government coalition is fragile, with the Five Star Movement and the League often at loggerheads on the economy, and now clashing on security measures. The antagonistic rhetoric from Italy’s leaders has recently reappeared in order to lure voters, with Deputy Premier Matteo Salvini ready to scrap “all limits” set by the EU. The results would also have consequences on how investors perceive the risk of Italy exiting the euro, which is currently fairly low, according to Barclays strategists.

For Jefferies strategists, however, a probable move toward more populist members of European Parliament following the election could put pressure on fiscal loosening and infrastructure spending, to the benefit of construction companies.

European voters have previously shown their capacity to surprise, and anything but stability and unity may not inspire the much-needed confidence to drive equity flows back to Europe.

Euro Stoxx 50 futures are trading down 0.7% ahead of the open.

- Watch the pound and U.K. stocks after speculation was rife that Prime Minister Theresa May could be pushed out of her job by Wednesday but she has remained steadfast even in the face of near certain defeat for her deal. Pound investors are bailing out of the currency as the uncertainty about who will be running the country.

- Watch copper-exposed miners, which may be active Thursday after the base metal’s price slid further on continued concerns about the U.S.-China trade dispute. LME copper sank further below the $6,000/ton mark. Watch pure-play copper names like Antofagasta, KAZ Minerals, KGHM and Aurubis, as well as diversified miners.

- Watch reaction to the Fed’s minutes after the central bank confirmed it intends to stay in wait-and-see mode for some time.

- Watch trade-sensitive stocks as China’s response is increasingly the focus as a full-blown trade war becomes the baseline assumption rather than just a risk. Goldman Sachs thinks the odds of a continued stalemate are high. The EU is also waiting to get into trade talks with the U.S., but isn’t sure the latter is ready for that yet. The trade war has, however, put the dollar back on its throne.

COMMENT:

- “Our five key inflation drivers for 2019 are aligning for higher inflation prints,” Citi strategists write in a note. “This could surprise markets as U.S. inflation pricing declined with the latest risk-off sentiment and Eurozone inflation pricing has fallen towards the lows seen in 2016.”

COMPANY NEWS AND M&A:

- Novartis Plans More Than 10 Launches by 2021

- France Pushes for Stronger Ties Between Renault, Nissan

- Bayer Roundup Talks to Be Led by Top Mediator Ken Feinberg (2)

- Fiat Chrysler CEO Boosts Brazil Wager in $4 Billion Comeback Bid

- Colas, Bouygues Win French Highway Contract Worth EU150M

- Activist ValueAct Urges Merlin Entertainments to Go Private

- Seadrill Ltd 1Q Adjusted Ebitda Beats Highest Est.

- BW Offshore First Quarter Ebitda Beats Highest Estimate

- Pfeiffer Vacuum 2Q Orders ‘Subdued’; FY Sales View Hits Midpoint

- Sandvik CEO Says He Won’t Remain at Co. for a Very Long Time: DI

- Newest Carige Plan May See Cap Raising Reduced to EU630m: Sole

- Dana Gas Gets Regulator Approval to Buy Back 10% of Shares

NOTES FROM THE SELL SIDE:

- Proximus now trades broadly in line with the sector following outperformance since Citi’s upgrade in September, leading the broker to now cut its rating to neutral.

- Berenberg initiated OMV at buy with EU60 PT, with co. seen exposed to most attractive free cash flow profile among the European integrated stocks.

- Inwit upside potential from the Vodafone deal is under-appreciated; Citi expects deal to be accretive and lead to an operation with a strong market position, upgrading stock to buy.

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 383.4 (50-DMA); 385.7 (76.4% Fibo)

- Support at 374.5 (61.8% Fibo); 369 (200-DMA)

- RSI: 44.9

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,410 (50-DMA); 3,516 (76.4% Fibo)

- Support at 3,309 (50% Fibo); 3,272 (200-DMA)

- RSI: 46

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- Anglo American Upgraded to Buy at SocGen

- Eutelsat upgraded to buy at HSBC; PT 19.50 Euros

- HSBC upgraded to buy at Goldman; PT 9.25 Pounds

- Heineken upgraded to add at AlphaValue

- Inwit upgraded to buy at Citi; PT Set to 9 Euros

- Opus upgraded to buy at Kepler Cheuvreux; PT 6.75 Kronor

- Rio Tinto Upgraded to Hold at SocGen

DOWNGRADES:

- Babcock downgraded to hold at Stifel; PT 4.85 Pounds

- dormakaba Cut to Reduce at Kepler Cheuvreux; PT 645 Francs

- Maha downgraded to neutral at SpareBank; PT 32 Kronor

- Proximus downgraded to neutral at Citi

- SAS downgraded to hold at HSBC; PT 16 Kronor

- SafeCharge downgraded to neutral at Macquarie; PT 4.36 Pounds

INITIATIONS:

- Nexi rated new buy at Goldman; PT 10.80 Euros

- Nexi rated new buy at HSBC; PT 10 Euros

- Nexi rated new neutral at Citi; PT 9.40 Euros

- Nexi rated new outperform at Mediobanca SpA; PT 10.50 Euros

- Nexi rated new overweight at Barclays; PT 10 Euros

- OMV rated new buy at Berenberg; PT 60 Euros

- Serica rated new buy at Jefferies; PT 1.85 Pounds

- Swedish Match reinstated overweight at Barclays; PT 530 Kronor

MARKETS:

- MSCI Asia Pacific down 0.1%, Nikkei 225 down 0.8%

- S&P 500 down 0.3%, Dow down 0.4%, Nasdaq down 0.4%

- Euro down 0.01% at $1.1149

- Dollar Index up 0.11% at 98.15

- Yen up 0.06% at 110.29

- Brent down 0.9% at $70.4/bbl, WTI down 0.9% to $60.9/bbl

- LME 3m Copper down 0.2% at $5913.5/MT

- Gold spot up 0.1% at $1274.3/oz

- US 10Yr yield down 1bps at 2.38%

MAIN MACRO DATA (all times CET):

- 8:45am: (FR) May Business Confidence, est. 105, prior 105

- 8:45am: (FR) May Manufacturing Confidence, est. 101, prior 101

- 8:45am: (FR) May Production Outlook Indicator, est. -2, prior -2

- 8:45am: (FR) May Own-Company Production Outlook, prior 9

- 9:15am: (FR) May Markit France Manufacturing PMI, est. 50, prior 50

- 9:15am: (FR) May Markit France Services PMI, est. 50.8, prior 50.5

- 9:15am: (FR) May Markit France Composite PMI, est. 50.3, prior 50.1

- 9:30am: (GE) May Markit/BME Germany Manufacturing PMI, est. 44.8, prior 44.4

- 9:30am: (GE) May Markit/BME Germany Composite PMI, est. 52, prior 52.2

- 9:30am: (GE) May Markit Germany Services PMI, est. 55.4, prior 55.7

- 10am: (EC) May Markit Eurozone Manufacturing PMI, est. 48.1, prior 47.9

- 10am: (EC) May Markit Eurozone Services PMI, est. 53, prior 52.8

- 10am: (EC) May Markit Eurozone Composite PMI, est. 51.7, prior 51.5

- 10am: (GE) May IFO Business Climate, est. 99.1, prior 99.2

- 10am: (GE) May IFO Expectations, est. 95, prior 95.2

- 10am: (GE) May IFO Current Assessment, est. 103.5, prior 103.3

To contact the reporter on this story: Michael Msika in London at mmsika4@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Jon Menon

©2019 Bloomberg L.P.