Plan for Emerging Markets Pits Wall Street Versus Washington

Plan to Save Emerging-Market Debt Pits Wall Street vs Washington

(Bloomberg) -- When Bill Rhodes says the debt crisis that’s erupted across the world’s emerging markets is the worst he’s ever seen, it must be bad.

Rhodes, 84, knows a thing or two about the topic. The former Citigroup Inc. executive is a veteran of the 1980s Brady Plan that re-set the clock for Latin America’s struggling economies by creating a new debt structure for developing nations that’s largely in place to this day.

“It’s going to be difficult,” Rhodes said in a Thursday interview. “You need to have some sort of coordination between the private and the public sectors.”

Three decades after U.S. Treasury Secretary Nicholas Brady stepped in to rescue emerging markets, the global pandemic is again challenging the world for a solution -- and this time, a raft of private bondholders must also be on board. More than 90 nations have already asked the International Monetary Fund for help amid the pandemic.

It’s clear that the task would be daunting. The $160 billion debt renegotiated during the Brady Plan pales next to the $730 billion that the Institute of International Finance says is due in hard-currency debt by emerging-market nations by the end of 2020.

And unlike 1989, when the loans were mostly held by banks and defaults had already happened, now it’s split between hundreds of creditors ranging from New York hedge funds to Middle Eastern sovereign wealth funds and Asian pension funds.

Academics and authorities are advocating for steps that would allow developing nations to pause bond payments through at least 2020, if not even longer, until the coronavirus fades and economies stabilize enough to analyze debt sustainability. That’s upsetting some creditors on Wall Street who depend on those funds to keep their portfolios afloat.

Group of 20 leaders and multilateral organizations are already working toward relief for nations to stay current on debt. The IMF and Paris Club asked the Washington-based IIF to coordinate a standstill, and the United Nations is calling for a new global debt body.

Private creditors are exploring ways to join initiatives to waive debt payments from poor countries, the IIF and Paris Club said on Thursday. They will work in the coming weeks on reference terms for voluntary private-sector participation in debt-relief efforts, the two bodies said in a statement.

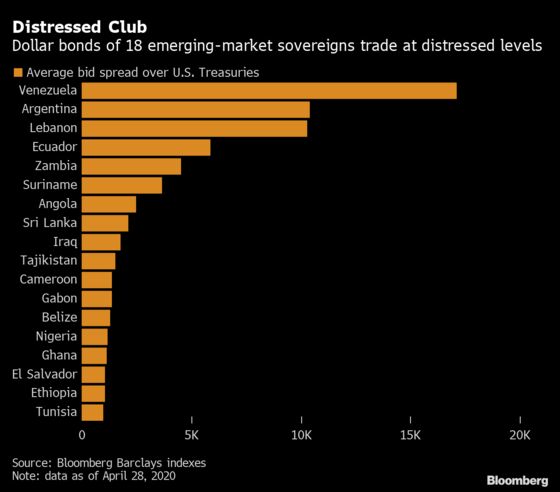

A solution can’t come soon enough. Dollar-denominated notes from 18 developing nations already trade at spreads of at least 1,000 basis points over U.S. Treasuries, the benchmark for distressed debt, data compiled by Bloomberg show. While the top three outliers -- Venezuela, Argentina and Lebanon -- were grappling with their own problems before the pandemic, others are approaching those levels amid currency sell-offs and record-shattering outflows.

Brazil, Mexico, Colombia, South Africa, India and Indonesia may be among the most vulnerable to a virus-related crisis, Anna Stupnytska, Fidelity International’s London-based head of global macro and investment strategy, said in a Bloomberg Television interview on Wednesday. She expects the coming months to be critical.

It isn’t just risky for governments. Moody’s Investors Service expects coronavirus-related disruptions and uncertainty to push emerging-market corporate defaults much higher in 2020.

Debt Relief

Forbearance on debt payments is the most popular idea to help emerging markets, although it would probably need to extend beyond 2020, according to Anna Gelpern, a law professor at Georgetown University who spent six years at the U.S. Treasury. A coordination group could offer standardized terms to all of a country’s creditors that automatically push out payments, she said.

Still, it will be no easy task to convince private creditors, especially those with large emerging-market exposure, to take a hit by deferring debt payments.

Zambia is asking restructuring houses for advice on how to handle its debt load, while Argentina has proposed a restructuring plan that includes a three-year payment moratorium.

“Countries that look to markets and are willing to engage market participants have found success in bridging the Covid financial shock,” said Hans Humes, chief executive officer of New York-based Greylock Capital Management, which has been involved in most emerging-market restructurings over the past quarter-century.

Bondholders already granted Ecuador a delay on coupon payments until August, which may save the government as much as $1.35 billion this year, as it deals with one of the region’s worst virus outbreaks and a sell-off in oil.

LISTEN: Bloomberg Intelligence’s Damian Sassower on funding stresses in EM

Even so, “the time and resource costs of pursuing market debt relief may outweigh the benefits,” Dylan Smith, a London-based economist at Goldman Sachs Group Inc., wrote in an April 17 note. Plus, “it is not clear that the fiduciary duties of large bondholders toward their investors would allow them to provide lenience to debtors, even if they privately support the initiative.”

Lee Buchheit, a four-decade veteran of the restructuring world, said forcing each nation to renegotiate on its own would only exacerbate the pain.

“Here we have a planet-wide phenomenon that is going to make a number of countries have to face unsustainable debt positions,” he said.

©2020 Bloomberg L.P.