Partisan Bias Is Messing With Asset Prices

Partisan Bias Is Messing With Asset Prices

(Bloomberg) -- Politics seems to be seeping into everything these days, and new research suggests partisanship is even shaping asset prices.

Party bias alters financial analysts’ evaluation of corporate creditworthiness, based on a database created and analyzed by Elisabeth Kempf at the University of Chicago and Margarita Tsoutsoura at Cornell University. Analysts who aren’t in the president’s party are more likely to downgrade their ratings, an effect more pronounced in periods of high partisan conflict. The changed ratings are less accurate, but that doesn’t stop them from feeding through to asset prices.

(You’re reading Bloomberg’s weekly economic research roundup.)

“The stock market does not seem to correct analysts’ ideological bias,” the authors write in a National Bureau of Economic Research working paper. “Rating actions by partisan analysts have price effects, and can therefore distort firms’ financing and investment decisions.”

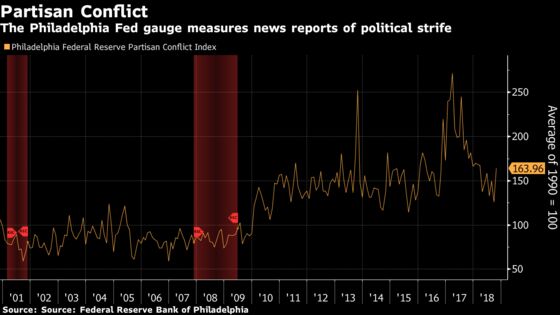

The authors compile a sample of 449 corporate credit analysts at Fitch Ratings, Moody’s Investors Service and S&P Global Ratings between 2000 and 2015, along with party affiliations. They compare analysts rating the same firm at the same point in time to arrive at their results, and use the Federal Reserve Bank of Philadelphia’s Partisan Conflict Index to show that the effect of bias is stronger when partisan divides are greater.

Other Research Worth a Read…

Socially Useless Jobs

Published on IZA

About 8 percent of workers think their jobs are socially useless, and another 17 percent doubt the usefulness of their work, according to a paper that uses data from a survey of 100,000 workers from 47 countries in 1989, 1997, 2005 and 2015. Poland, Japan and Israel lead the pack for workers who think they labor for little, while Mexicans are comparatively less likely to feel that way. Germany, Britain and the U.S. rank somewhere in the middle.

Simply Is Best: Enhancing Trust and Understanding of Central Banks Through Better Communications

Published on Bank Underground

Central bankers are trying hard to communicate more clearly, and the Bank of England is putting that push under a microscope. To test whether the bank’s new “layered” monetary policy release is reaching people, researchers asked 2,000 online participants to read one of four Inflation Report summaries: the specialist-targeting Monetary Policy Summary, the jargon-free and chart-heavy Visual Summary in the official release, an unofficial reduced text summary, and an unofficial “relatable” summary, which used real-life examples to explain ideas. They found that the visual summary boosted understanding, and those who read the “relatable” version learned the most.

Explaining Monetary Spillovers: The Matrix Reloaded

Published on the Bank for International Settlements

Federal Reserve and European Central Bank monetary policy moves spill over long-term interest rates thanks partly to exchange rate adjustments, this Bank for International Settlements paper finds, but “by far” the strongest determinant of interest rate spillover is financial openness. Countries with stronger financial links to the U.S. and euro area are more vulnerable to their rate changes. The fact that the long end of the yield curve is more responsive to big central bank moves suggests that while “countries retain policy rate independence, financial conditions are influenced by global yields,” the authors write.

To contact the reporter on this story: Jeanna Smialek in New York at jsmialek1@bloomberg.net

To contact the editors responsible for this story: Brendan Murray at brmurray@bloomberg.net, Jeff Kearns, Sarah McGregor

©2018 Bloomberg L.P.