Putin vs. the Crown Prince: Ruble Gives Russia Edge in Price War

Oil Endurance Test Hinges on Ruble’s Edge Over Saudi Peg

(Bloomberg) -- If the oil face-off between President Vladimir Putin and Saudi Crown Prince Mohammed bin Salman turns on who has a stiffer fiscal backbone, it’s the ruble that could help carry Russia to the finish line.

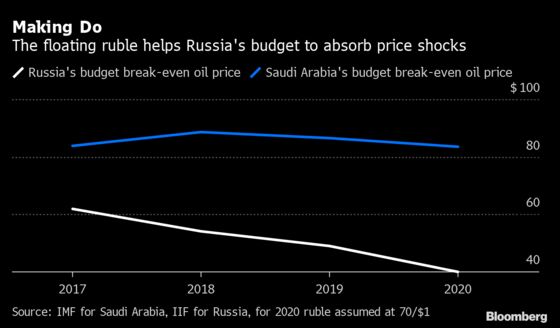

Saudi Arabia may boast the lowest extraction costs and more spare capacity, but it has little to counter Russia’s shock-absorber in its floating currency. An anchor of stability that’s been pegged for over three decades to the dollar, the riyal becomes more a straitjacket when oil prices go bust.

“A flexible exchange rate puts Russia at an advantage versus other commodity exporters at times of oil-price swings,” said Elina Ribakova, deputy chief economist at the Institute of International Finance. “Saudi Arabia has its hands tied.”

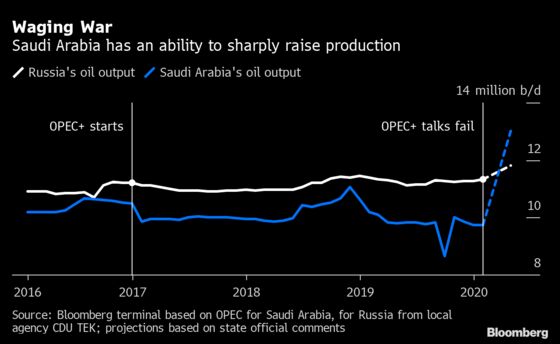

The disintegration of the production pact between OPEC and Russia last week jolted the oil market and turned the spotlight on the finances of commodity producers. Saudi Arabia escalated a price war with a move to flood the market with crude, taking advantage of its ability to drop prices and grab market share with higher production than Russia. But Russia’s top producer reciprocated with a plan to ramp up output too.

To the extent that fiscal challenges will dictate how long Saudi Arabia and Russia can endure a severe downturn in oil prices, especially with the coronavirus outbreak holding back demand, the clock will be ticking louder for the kingdom. Every day of ruble depreciation buys Moscow more time.

Russia gets 70 billion rubles ($969 million) in extra income for every 1 ruble decline against the dollar relative to the exchange rate used to calculate the budget, according to the Finance Ministry. The effect is similar for Russian oil producers, whose expenses are mostly in local currency whereas revenue is in dollars.

| What Our Economists Say... |

|---|

“Low oil prices will leave a smaller hole in the budget for Russia than for Saudi Arabia, and reserves are ample enough to fill it. But the buffers aren’t limitless, and the price shock will still be painful.” --Scott Johnson |

Russia’s exchange rate has retreated by about 5%, a drop of nearly 4 rubles, in the days since Saudi Arabia aggressively cut its selling prices and ramped up production in response to Putin’s refusal to curb output.

Although a weaker currency will boomerang by fanning inflation and sapping consumer purchasing power, Saudi Arabia’s policy of tethering the riyal will leave it cornered as it explores options for surviving the oil shock.

Read more: SAUDI INSIGHT: What Virus, Oil Mean for Growth, Deficit And Peg

Protecting the peg puts pressure on the kingdom’s foreign reserves, since it needs a dollar cover for every riyal in circulation and demand deposits. Adjusting for narrow money supply at the end of 2019, Saudi Arabia had just $343 billion of holdings at the central bank and foreign assets invested through sovereign wealth funds, according to Ziad Daoud of Bloomberg Economics.

When Saudi Arabia tapped reserves and turned to borrowing after the oil crash six years ago, Russia opted for frugality since 2017, stowing away windfall earnings it can now start spending. The Finance Ministry says it can cope with oil at as low as $25 a barrel for the next decade.

Economists are less sure about that, warning that Russia may use up nearly its entire wealth fund in about three years. If oil prices stabilize at lower levels, the government could face the choice of spending cuts or raising taxes.

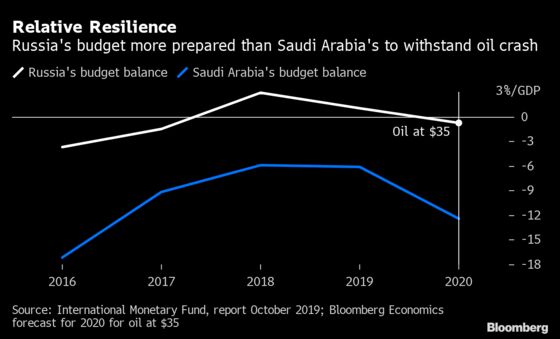

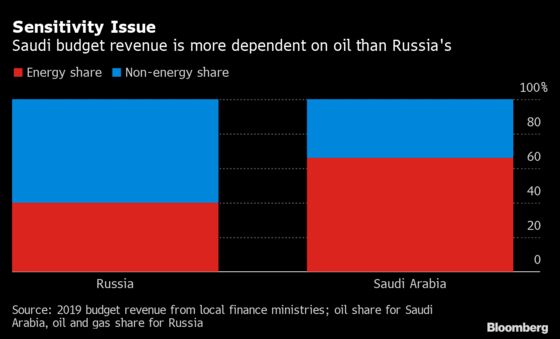

But by putting its fiscal house in order, Russia has added to its resilience, becoming less reliant on energy than Saudi Arabia’s budget. It’s a mismatch that might tip the scales in Russia’s favor in the longer run if the two can’t put aside their differences over how to manage oil prices.

The kingdom could run a wider budget deficit, absorbing the shock to its finances instead of accepting slower growth, according to Bloomberg Economics, which projects the fiscal shortfall may rise this year to $86 billion, or 11.1% of gross domestic product, if oil is at $40.

Saudi Arabia’s peg also means its current account will fare worse than Russia’s, since a weaker currency will allow Russia to adjust by making imports more expensive. That will leave the kingdom with the choice of running a much tighter fiscal policy or relying on borrowing or reserves to cover its external gap.

Should its budget shortfall run at $86 billion a year, Saudi Arabia has enough net foreign assets to finance its deficits for just four years, Bloomberg Economics estimates.

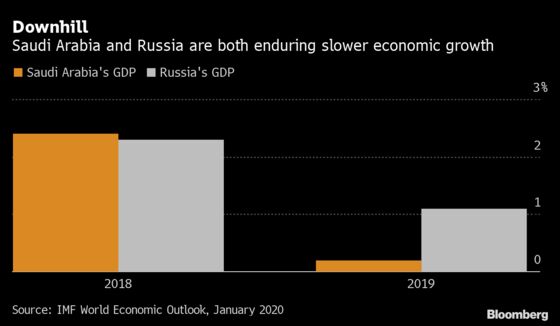

The oil showdown, however, isn’t just a budget math exercise for Saudi Arabia or Russia. Even before the recent market jolt, both already faced the prospect of sluggish economic growth after a disappointing run in recent years.

Higher oil production may offset the hit to their economies, but the damage to confidence and investment could be a drag in years ahead. It’s also a possible setback for Putin’s goal of unleashing fiscal stimulus after years of austerity, as spending plans come into question if oil doesn’t recover.

While the oil crisis is certain to sow economic anxiety for both Saudi Arabia and Russia, budget constraints will likely shorten the kingdom’s timeline.

“Saudi Arabia is trying to aggressively win market share but it cannot run this war for long,” said Christopher Dembik, global head of macroeconomic research at Saxo Bank. “At the end of the day, looking at the fiscal situation, Russia is clearly in better position.”

To contact the reporters on this story: Anya Andrianova in Moscow at aandrianova@bloomberg.net;Abeer Abu Omar in Dubai at aabuomar@bloomberg.net

To contact the editors responsible for this story: Gregory L. White at gwhite64@bloomberg.net, ;Lin Noueihed at lnoueihed@bloomberg.net, Paul Abelsky, Benjamin Harvey

©2020 Bloomberg L.P.