U.S. Coal Giant That Pressed Trump for Bailout Faces Default

The largest closely held coal miner in America failed to make multiple payments to lenders this week.

(Bloomberg) -- Murray Energy Corp., the U.S. coal giant that had pressed the Trump administration for help averting bankruptcy, may be headed toward default.

The largest closely held coal miner in America failed to make multiple payments to lenders this week, the company said in a statement on Wednesday. Creditors have agreed not to take legal action until Oct. 14, buying Murray some time to figure out how to shore up its balance sheet, the St. Clairsville, Ohio-based firm said.

Murray Energy is struggling to stay afloat, along with the rest of America’s coal miners, as cheap natural gas and renewable energy resources cut into coal’s share of the U.S. power market. At least four companies including Cloud Peak Energy Inc. and Blackjewel LLC have gone bankrupt this year, laying bare the decline of a fuel that once accounted for more than half of all U.S. power generation. Today it’s less than 25%.

Prices for thermal coal -- the kind burned by power plants -- have slumped, which may have left Murray short on cash, said Lucas Pipes, a coal analyst with B Riley FBR Inc. “You can’t make payments out of thin air if the money isn’t in the bank,” he said.

The company idled some of its mines in West Virginia last month, citing “severely depressed coal markets.”

Murray’s potential default comes more than a year after the Trump administration’s efforts to subsidize struggling nuclear and coal-fired power plants -- particularly ones that Murray supplies -- failed, shot down by President Donald Trump’s own appointed energy regulators. Chief Executive Officer Bob Murray, an early Trump supporter and a big donor to his campaign, was instrumental in setting his energy agenda and has hosted multiple fundraisers for him.

The White House didn’t respond to a request for comment. The administration has considered other proposals to aid coal plants since, including one that would’ve had the Energy Department use its emergency authority to order grid operators to buy power from coal generators. But U.S. Energy Secretary Rick Perry said in June that there had been no movement on a plan.

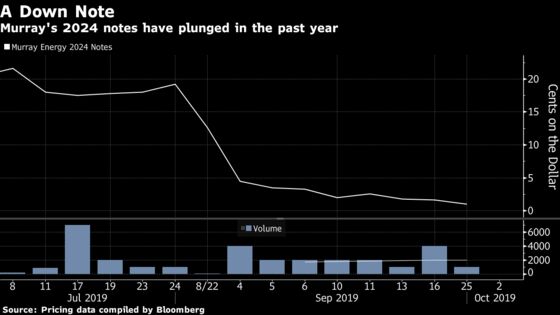

The company’s 2024 notes with about $500 million outstanding traded at 1 cent on the dollar last month, down from above 60 cents late last year, according to Trace price data.

On Tuesday, U.S. coal miner Foresight Energy LP failed to make its own interest payment, invoking a 30-day grace period to evaluate options. The shares slid 26% on the news to a record low. Murray and Foresight are inextricably linked: Murray bought a controlling stake in the St. Louis, Missouri-based company that hasn’t posted an annual profit since 2014.

While America’s biggest publicly traded coal miners, including Peabody Energy Corp., filed for bankruptcy in recent years, Murray chose to avoid that route. It has left the company at a potential disadvantage as it wrestles with how to manage its debt as opposed to investing money in its business, according to credit raters.

Secular Decline

Murray’s forbearance agreements are with lenders holding more than 50% of Murray’s loans under a credit and guaranty agreement and those holding more than half of loans under ABL and FILO credit facilities, according to the company’s statement.

Murray’s efforts to improve its liquidity will prove challenging as it runs up against a heavy debt load and an industry in secular decline, according to Moody’s Investors Service. U.S. power plants are turning away from coal and toward cleaner and cheaper alternatives and export markets are also under pressure, Moody’s said.

The company has tried to ease the strain before through deals with creditors, including a 2018 debt swap that gave holders 74 cents on the dollar and extended the due date by a year on some term loans. Moody’s labeled that agreement a default.

(Michael R. Bloomberg, the founder and majority stakeholder of Bloomberg LP, the parent company of Bloomberg News, has committed $500 million to launch Beyond Carbon, a campaign aimed at closing the remaining coal-powered plants in the U.S. by 2030 and slowing the construction of new gas plants.)

--With assistance from Jordan Fabian and Jennifer A. Dlouhy.

To contact the reporters on this story: Will Wade in New York at wwade4@bloomberg.net;Rick Green in New York at rgreen18@bloomberg.net

To contact the editors responsible for this story: Lynn Doan at ldoan6@bloomberg.net, Pratish Narayanan

©2019 Bloomberg L.P.